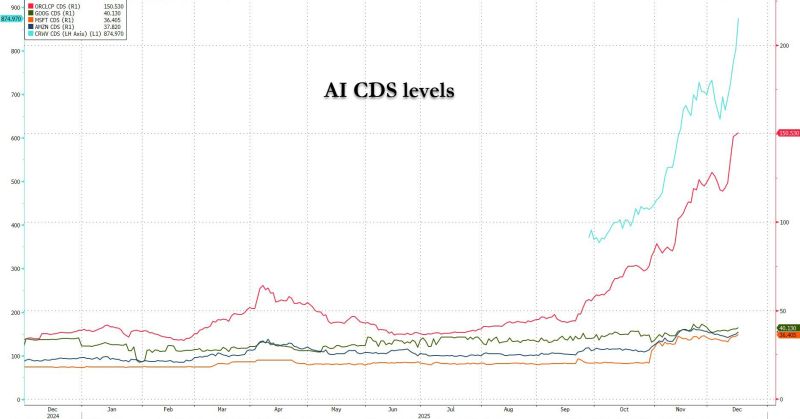

AI CDS levels update

Coreweave in blue Oracle in red Source: www.zerohedge.com

Everyone is talking about Oracle CDS, but Coreweave $CRWC CDS is the real gem...

Source: RBC, Bloomberg

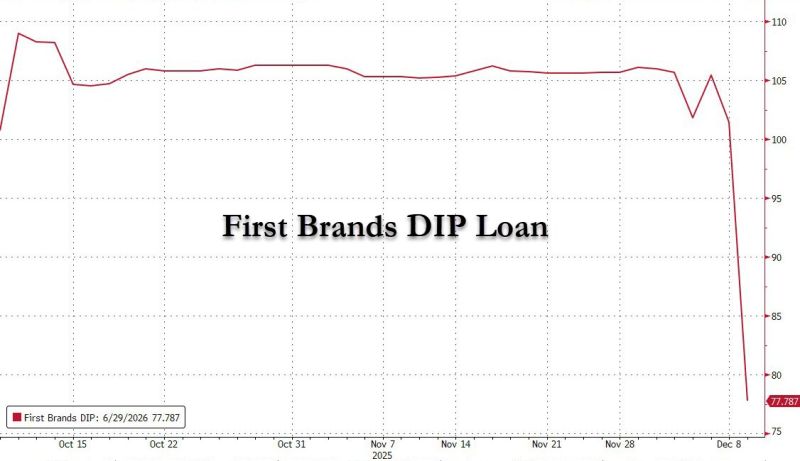

It looks like those who did zero homework on the First Brands term loans did exactly zero homework on the First Brands DIP loans.

A DIP (Debtor in Possession) loan is a form of financing that is provided to companies facing financial distress and who are in need of bankruptcy relief. In other words, the main purpose of DIP financing is to help fund an organization out of bankruptcy. Source: www.zerohedge.com, Bloomberg

Oracle 5Y CDS graph looks exciting $ORCL until you run the math and realize that it is only pricing in 1.93% probability of default per year.

And a 9% 5 year cumulative probability of default... Historically, ORCL CDS traded around 20–40 bps, so 117 bps represents a material repricing of risk, but not a distressed profile. Source: Special Situations 🌐 Research Newsletter (Jay) @SpecialSitsNews

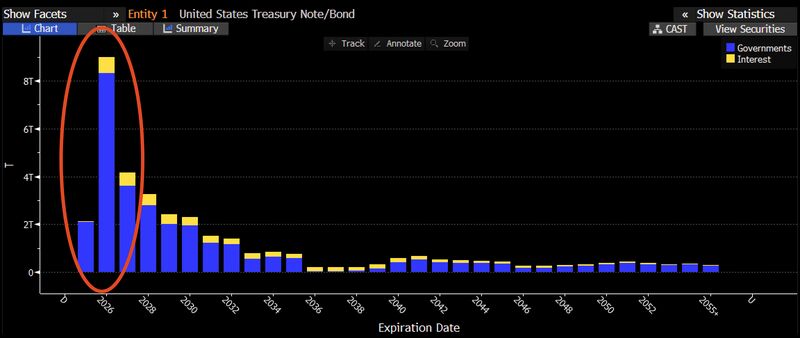

Interesting comment by James Lavish on X:

"With 10 Year UST yields continuing to rise on the eve of another Fed rate cut, it begs the question: Why is the Treasury pushing so hard for more cuts if the market is saying that it will only be inflationary in the long term? Answer: Because so much of US government debt is now short term T-Bills, with every 25bp cut, annual interest expense drops by ~25 billion. Cut rates low enough, and it could slash interest expense in half within the next two years". Source: James Lavish

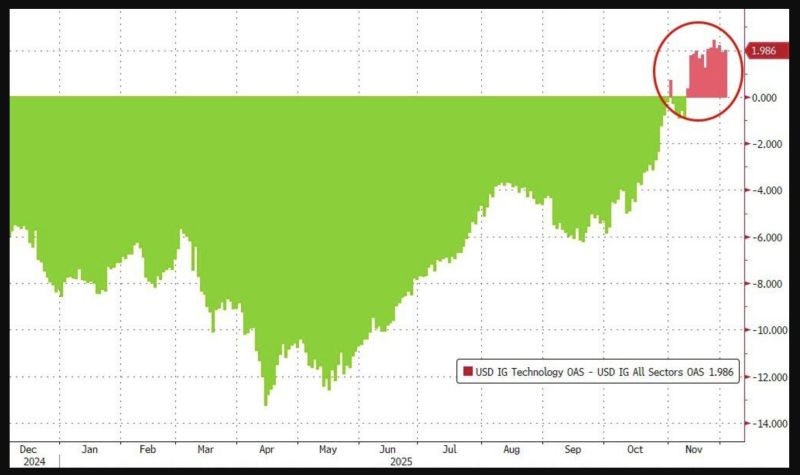

Overall Tech credit Spreads continue to trade wide to the overall IG credit market...

Source: zerohedge

Japan 10 year - US 10 year: the big crocodile jaw

Japan might have to use yield curve control again to save its bond market Source chart: The Market Ear

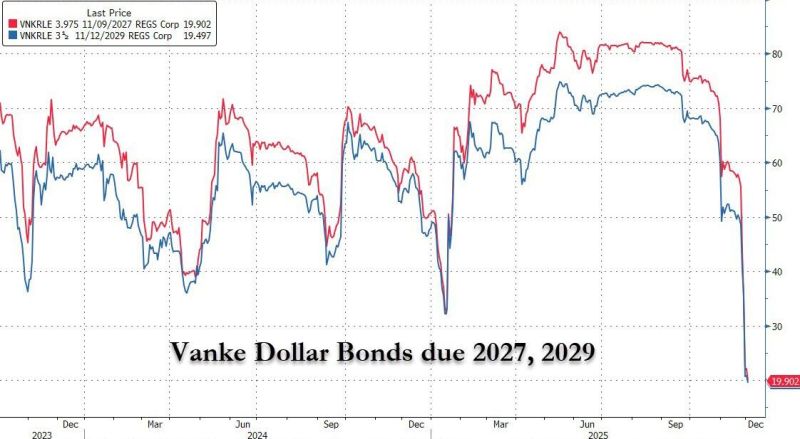

🔥 China’s Latest Property Shock: Vanke Just Broke the Last Illusion 🔥

Vanke, once viewed as China’s “safe” developer after Evergrande, just stunned markets. It’s asking for a 1-year delay on a ¥2B bond with zero upfront payment and even the interest pushed back a year. Creditors expected support. Instead, they got nothing. 📉 The fallout: ➡️ Bond crashed from near par to ¥27 ➡️USD notes collapsed to 20 cents ➡️Analysts warn this “shatters investor confidence” Vanke is now pledging core assets, being rejected for emergency loans, and facing warnings that its commitments are “unsustainable.” This isn’t one company’s problem — it’s the latest sign that China’s 5-year property downturn has no bottom. Home prices continue to fall, sales data is going missing, and global banks see years of decline ahead. And with China’s middle class holding most of its wealth in property, a deeper slump could be devastating. The crisis is no longer at the fringes. If Vanke is wobbling, the entire foundation is shaking. Source: zerohedge