Aramco just revealed the hidden cost of avoiding Hormuz

Saudi Aramco has built an alternative route that bypasses both the Strait of Hormuz and the Red Sea. Oil moves from Yanbu to Ain Sokhna, through the SUMED pipeline, exits via Sidi Kerir, and then sails around the Cape of Good Hope to reach Asia. The catch? That "safer" route now costs about $5 per barrel more once freight, insurance, and pipeline fees are included. On a typical cargo, that's roughly $10 million in additional costs. The impact is now so significant that Aramco is developing a separate pricing formula for these shipments because its standard Asia Official Selling Price (OSP) no longer reflects the true economics. The key takeaway: The market has been treating alternative routes as a free solution. They never were. Those costs are now becoming visible, and they're another reason why the true cost of oil is moving higher, even when headline crude prices don't fully reflect it. Source: Jack Prandelli on X

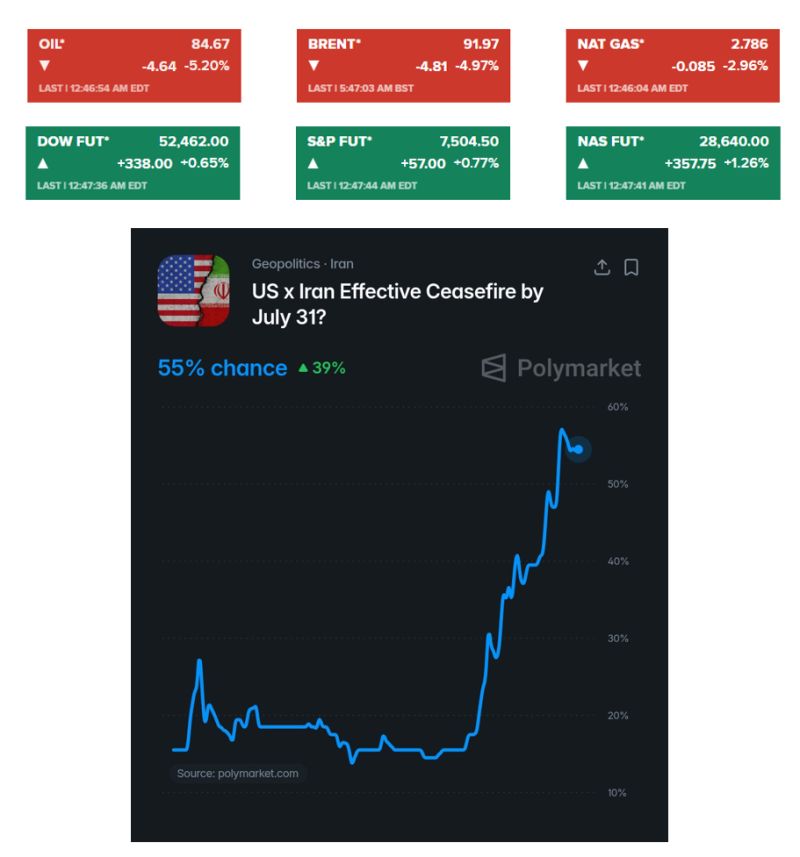

Oil slides 5% and US stocks indices futures jump as Iran reportedly signals halt to attacks if U.S. pause holds.

Iran has indicated it will stop carrying out attacks as long as the U.S. also refrains from striking, Reuters reported. There is now a 55% chance that the United States 🇺🇸 and Iran 🇮🇷 will sign a ceasefire this month, according to Polymarket traders Source: Evan, CNBC

Brent crude has returned to $100 a barrel after Houthi militants attacked two Saudi tankers in the Red Sea

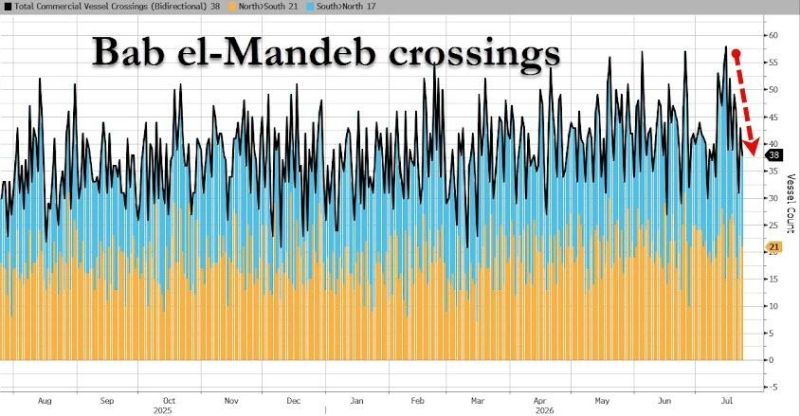

The attacks have widened the Middle East conflict and increased the risk of further oil supply disruptions. Shipping was already under pressure in the Strait of Hormuz because of renewed tensions between the US and Iran. The Bab el-Mandeb Strait had become an important alternative route, but more vessels are now avoiding it. Oil markets are also facing attacks on the Caspian Pipeline Consortium terminal, which handles most of Kazakhstan’s crude exports. With global inventories already reduced by months of conflict, the risk of a supply squeeze is rising. According to Saxo Bank, oil flows now face two major bottlenecks. This has pushed up the risk premium in crude prices and renewed inflation concerns. Source: zerohedge

President Trump told Axios on Thursday that he's seriously considering restarting major combat operations in Iran

Including strikes that would be bigger than the ones carried out during Operation Epic Fury. In a brief interview, Trump acknowledged that such a decision would have consequences and stressed he hasn't made a determination yet. Trump didn't give a deadline for his decision. Two other U.S. officials confirmed no call has been made and no new orders have been given to the military. The current escalation has caused oil prices to eclipse $100 per barrel. A return to all-out war is highly unpopular in the U.S. "I am considering a massive attack. Bigger than ever before. I am close to making a decision. We are all set for it," the president said. Trump said Israel "would join in two minutes if I ask them to," but added that "we don't need anybody" to launch a new operation against Iran. He also said there would be "consequences" for Israel joining the strikes, hinting at Iranian retaliation against Israel. Source: Axios

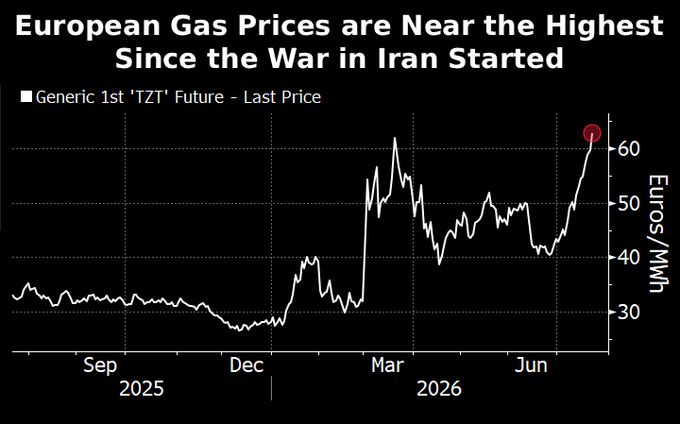

European gas futures are back near their highest level since the Iran war started

The reason: Europe is losing the LNG bidding war. Imports down 35% y/y over the last month; China's up 8%. TTF is back near its post-Iran-war high — not because Europe wants more gas, but because it has to pay up to get any. The cargoes aren't disappearing, they're just sailing east. US exporters are indifferent to which. Source: Jack Prandelli on X, Bloomberg

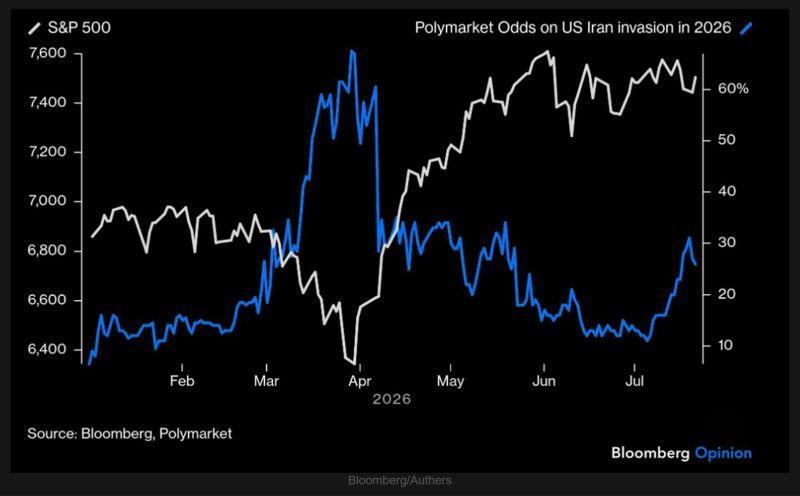

Prediction markets sharply lowered the perceived odds of a ground invasion, helping fuel a strong rally in the S&P 500.

Following conciliatory remarks from Iran and President Trump's announcement of a bombing pause earlier this year, investors concluded that neither side had the appetite for a prolonged ground conflict. Those odds have started to climb again, however, even as equities remain relatively resilient. Source: TME, Bloomberg/Authers

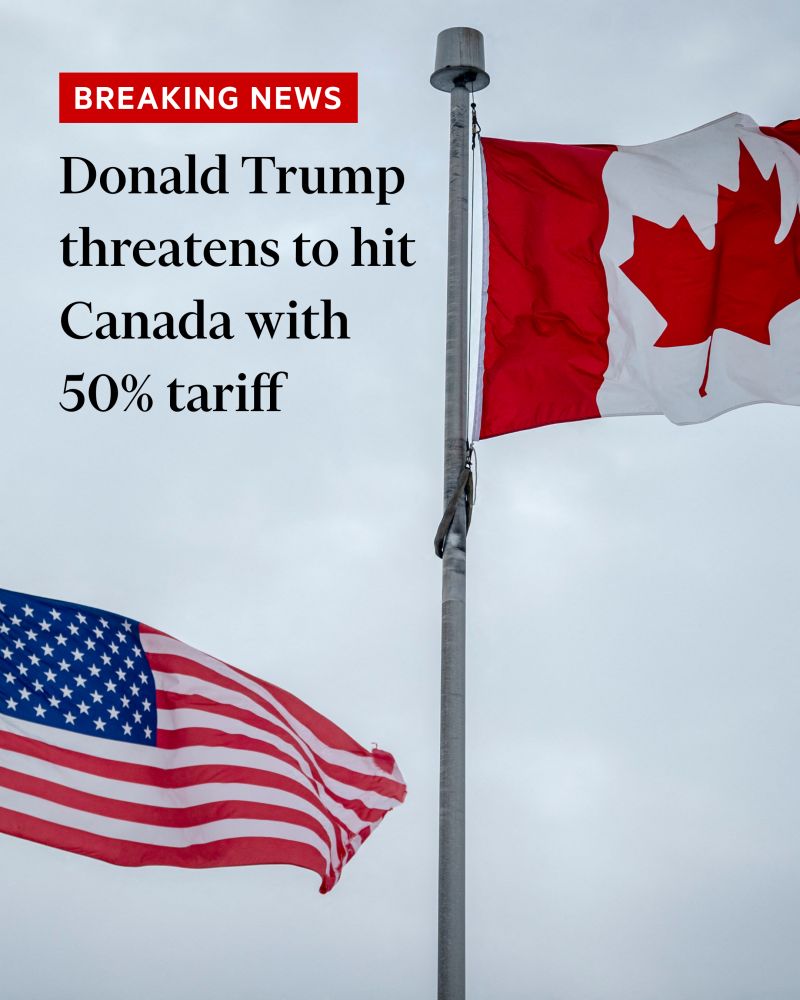

The US has said it will hit Canada with tariffs of 50 per cent on a wide range of goods in a move that threatens to reignite Donald Trump’s trade war

Senior Trump administration officials accused Canada of engaging in unfair trade practices, saying its provinces had halted the purchase of US alcohol, slapped tariffs on US cars and discriminated against American cheese. “At the outset of the president’s trade policy, which he implemented earlier last year, there were only two countries that retaliated against the United States: the People’s Republic of China and Canada,” said a senior administration official. Trump’s move on Monday risks re-inflaming a global trade skirmish that had eased after the US Supreme Court earlier this year knocked down the president’s global emergency tariffs. Canada is the US’s second-biggest trading partner, with trade between the two amounting to $716bn last year. Source. FT

Iraq just signed 48 DEALS with US companies, including with USA oil giants to bypass the Strait of Hormuz via a new pipeline

Total deals are worth over $60 BILLION, per Reuters. Chevron, ExxonMobil, Shell and more are also involved They also involved other industries, including healthcare, communications and infrastructure. It’s not clear when the oil deals will be able to create viable alternatives to the Strait of Hormuz, through which about a fifth of the world’s oil flows. Goldman Sachs estimates that pipelines in just one country take at least two and a half years to build, and these pipelines would travel through two or more nations. Iran has sought to close the Strait repeatedly since the U.S.-Iran war began Feb. 28, causing sharp gyrations in oil and gas prices. Alternatives routes for oil will weaken Iran's main bargaining power. Will China be the big loser here? Source: AP, Al Jazeera