Oil Reserves Are Still Dominated by the Giants

Proved reserves show where long-term oil power still sits Saudi Aramco remains in a league of its own with around 260 billion boe Source: Jack Prandelli on X

Brent Crude Oil crashes 10% as US and Iran halt strikes.

President Trump said the “perimeters of a deal” had been reached with Iran to reopen the Strait of Hormuz after speaking with Saudi Crown Prince Mohammed bin Salman (MbS). According to Saudi Arabia’s state news agency, both leaders emphasized dialogue, de-escalation, and pursuing a truce to prevent a wider regional conflict. Axios reported that MbS urged Trump to avoid large-scale strikes on Iran, warning of possible retaliation against Israeli and Gulf energy infrastructure. Saudi officials also sought clarity on U.S. military plans. As a key U.S. ally, Saudi Arabia has historically shaped Washington’s Iran policy and appears to have influenced efforts to delay or limit further escalation. Source: zerohedge

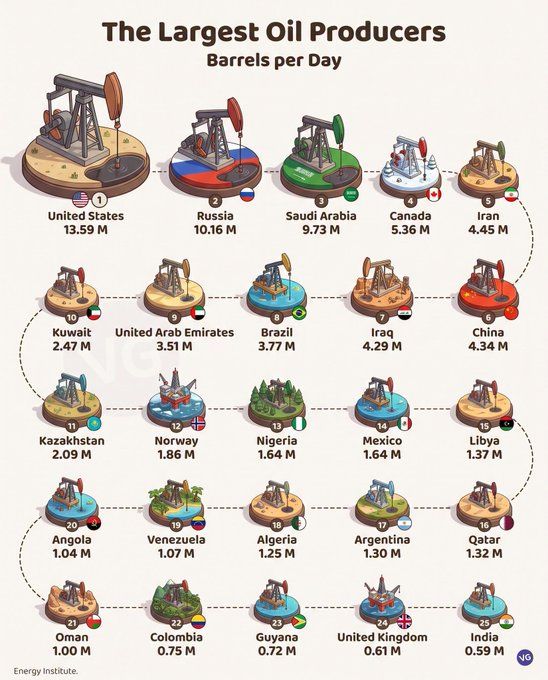

US produces 13.59 million barrels a day.

That is more than Russia and Saudi Arabia , at 10.16 million and 9.73 million. It is nearly triple Iran's 4.45 million. America is not just the largest oil producer on earth, it is exporting record volumes of that supply overseas. Source: Jack Prandelli on X

Aramco just revealed the hidden cost of avoiding Hormuz

Saudi Aramco has built an alternative route that bypasses both the Strait of Hormuz and the Red Sea. Oil moves from Yanbu to Ain Sokhna, through the SUMED pipeline, exits via Sidi Kerir, and then sails around the Cape of Good Hope to reach Asia. The catch? That "safer" route now costs about $5 per barrel more once freight, insurance, and pipeline fees are included. On a typical cargo, that's roughly $10 million in additional costs. The impact is now so significant that Aramco is developing a separate pricing formula for these shipments because its standard Asia Official Selling Price (OSP) no longer reflects the true economics. The key takeaway: The market has been treating alternative routes as a free solution. They never were. Those costs are now becoming visible, and they're another reason why the true cost of oil is moving higher, even when headline crude prices don't fully reflect it. Source: Jack Prandelli on X

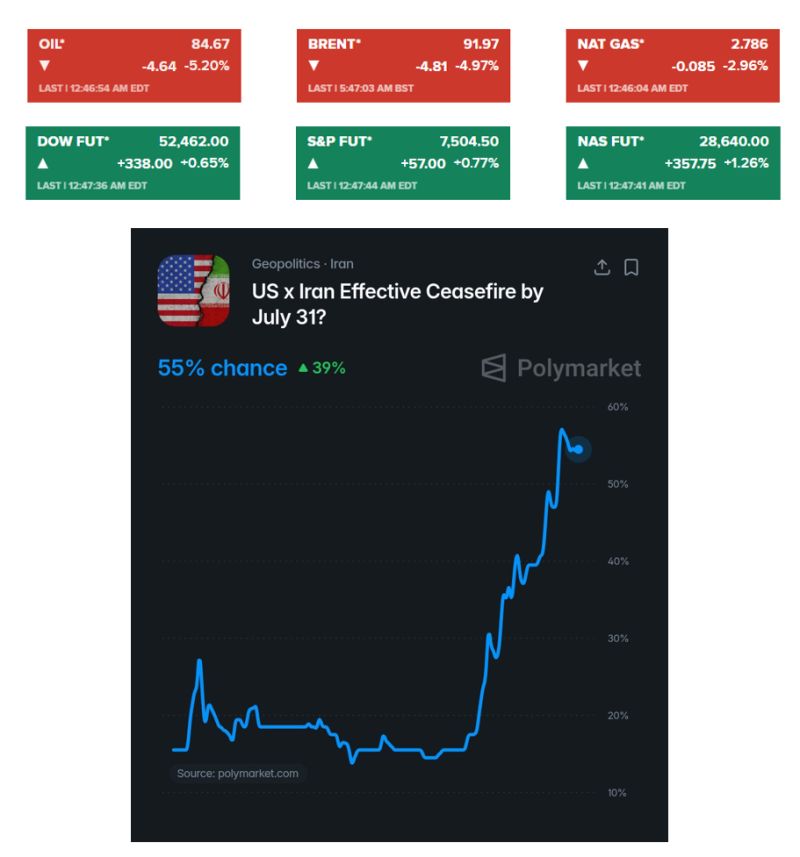

Oil slides 5% and US stocks indices futures jump as Iran reportedly signals halt to attacks if U.S. pause holds.

Iran has indicated it will stop carrying out attacks as long as the U.S. also refrains from striking, Reuters reported. There is now a 55% chance that the United States 🇺🇸 and Iran 🇮🇷 will sign a ceasefire this month, according to Polymarket traders Source: Evan, CNBC

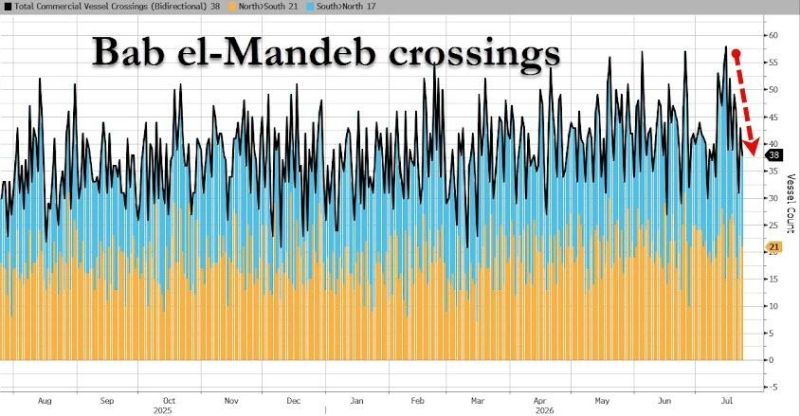

Brent crude has returned to $100 a barrel after Houthi militants attacked two Saudi tankers in the Red Sea

The attacks have widened the Middle East conflict and increased the risk of further oil supply disruptions. Shipping was already under pressure in the Strait of Hormuz because of renewed tensions between the US and Iran. The Bab el-Mandeb Strait had become an important alternative route, but more vessels are now avoiding it. Oil markets are also facing attacks on the Caspian Pipeline Consortium terminal, which handles most of Kazakhstan’s crude exports. With global inventories already reduced by months of conflict, the risk of a supply squeeze is rising. According to Saxo Bank, oil flows now face two major bottlenecks. This has pushed up the risk premium in crude prices and renewed inflation concerns. Source: zerohedge

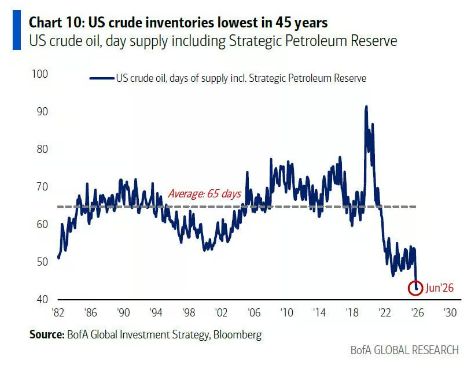

Crude Oil only has 43 days of supply left in the U.S., the lowest inventory in 45 years 🚨 🚨

Source: Barchart, BofA

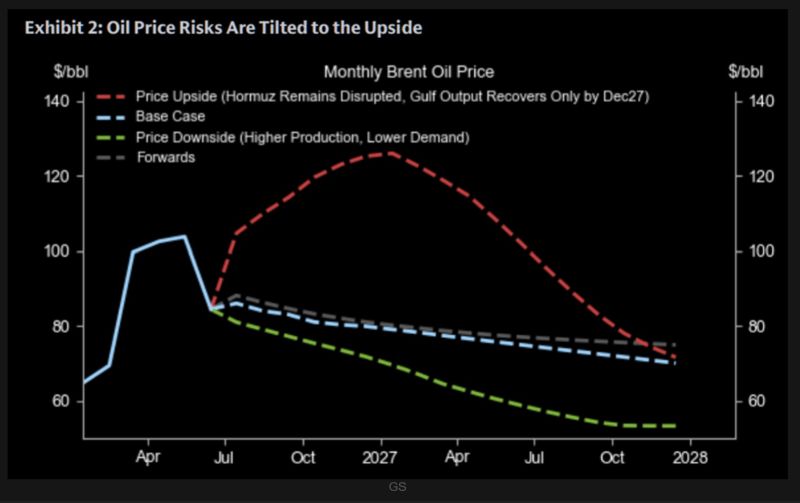

Goldman Sachs models a scenario where the Strait of Hormuz remains disrupted through late 2027.

Under these conditions, they project Brent crude could spike above $120/bbl by Q4 2026, before settling at an average of ~$100/bbl throughout 2027. This contrasts sharply with Goldman's $80 base case, suggesting current prices still assign relatively low odds to a prolonged physical supply disruption Source: GS, TME