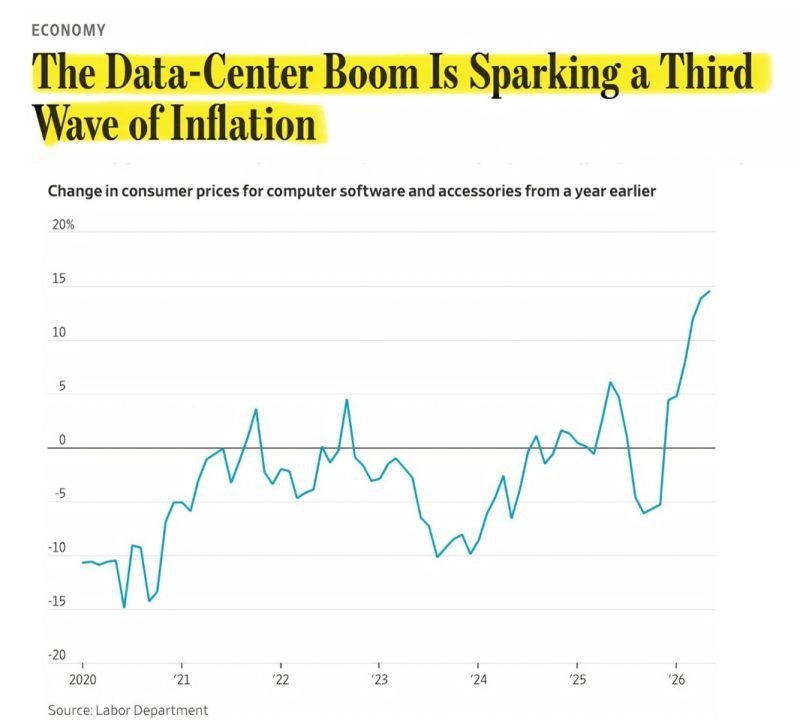

AI MAY BE TRIGGERING THE THIRD WAVE OF INFLATION.

Even Tim Cook recently said the current cost pressures are unlike anything he's seen in more than 40 years in the business. The first inflation wave came from supply chain disruptions. The second was driven by tariffs and energy prices. But this third wave could be different. Tariffs can be negotiated. Oil prices eventually fall as supply catches up. AI infrastructure spending doesn't work that way. This isn't a temporary supply shock. It's a massive demand shock that's still in its early stages. The five largest hyperscalers are expected to spend roughly $741 billion on AI infrastructure this year—up about 75% from last year. Much of that investment hasn't even translated into physical deployments yet. That means today's price pressures may be the beginning, not the peak. Here's why. AI requires enormous amounts of high-bandwidth memory and advanced chips. Those same components are also used in smartphones, laptops, gaming consoles, automobiles, and countless other electronics. As AI companies absorb a growing share of the available supply, they aren't just increasing the cost of AI—they're putting upward pressure on prices across the broader electronics market. We're already seeing signs of that. Apple and Microsoft recently raised prices on products including MacBooks, iPads, and Xbox consoles while pointing to higher component costs and memory constraints. Nintendo and Sony had already announced similar price increases weeks earlier. This isn't one company passing through higher costs. It's an entire hardware industry repricing around the same supply bottleneck. The Federal Reserve's long-term assumption is that AI will eventually offset these inflationary pressures through productivity gains. That may ultimately prove true. But several analysts, including UBS, argue those productivity benefits could take years to fully materialize, while the cost increases are happening today. That leaves the Fed facing a difficult balancing act: keeping interest rates elevated through a period where the technology expected to reduce inflation over the long run may be contributing to higher prices in the short run. If that's the case, this inflation cycle may prove more complex than the tariff- and energy-driven shocks policymakers have dealt with so far. Source: Bull Theory on X

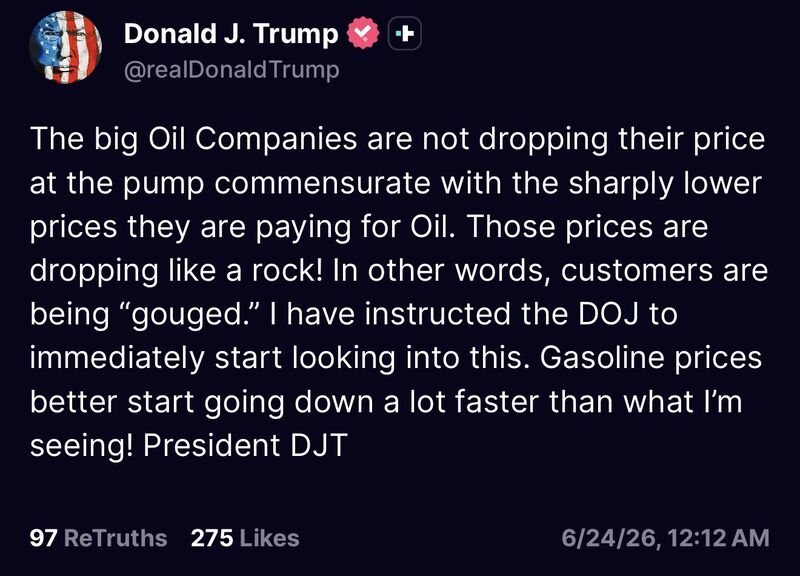

President Trump says he has instructed the DOJ to begin looking into “big Oil Companies” who “are not dropping their price at the pump”

“Customers are being ‘gouged’” he added Source: Trend Spider

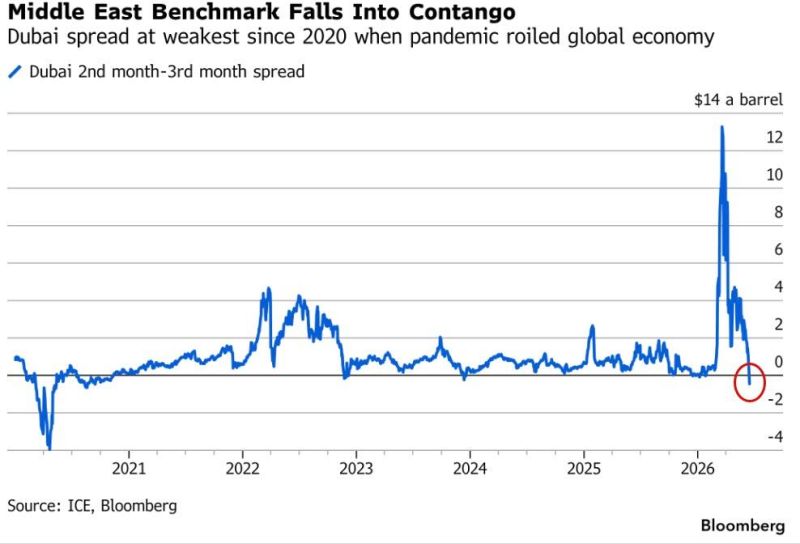

Bloomberg's Michael Ball notes that material flows through Hormuz creates a different problem for crude,

Especially in Asia, as too much supply hits a region that has already adapted to fewer Middle East barrels. Asian refiners replaced disrupted Middle East barrels with US crude and other alternatives, cut some processing runs when prices rose and are now facing a sudden wave of Persian Gulf supply. This has led Middle Eastern crude curves to flip into bearish contango, showing the market is pricing a near-term glut rather than shortage. Source: Bloomberg, zerohedge

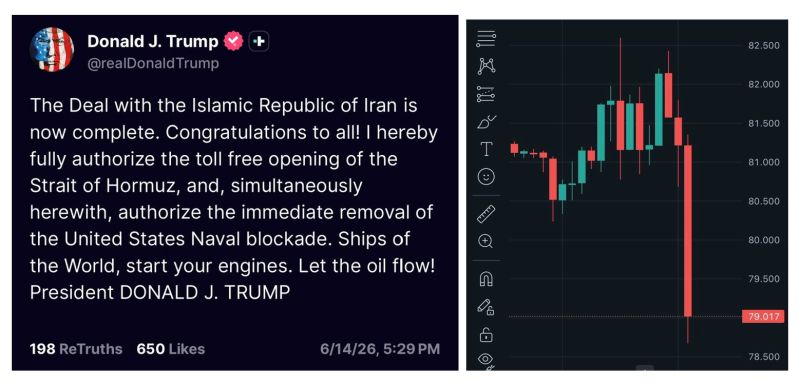

Trump: "The deal is complete (...) Let the oil flow!" Crude oil $WTI is plummeting on Hyperliquid in pre-market open!

After 107 days of war, the US and Iran have now officially reached a peace deal, with the signing set for June 19th in Switzerland.

Oil falls. Yields rise. Something has shifted

Oil down 15% in three weeks. The two-year yield up 15bps last week to 4.15% - its highest since early 2025. For the first time in months, US macro is back in the driving seat. Source: Jonny Matthews | SuperMacro

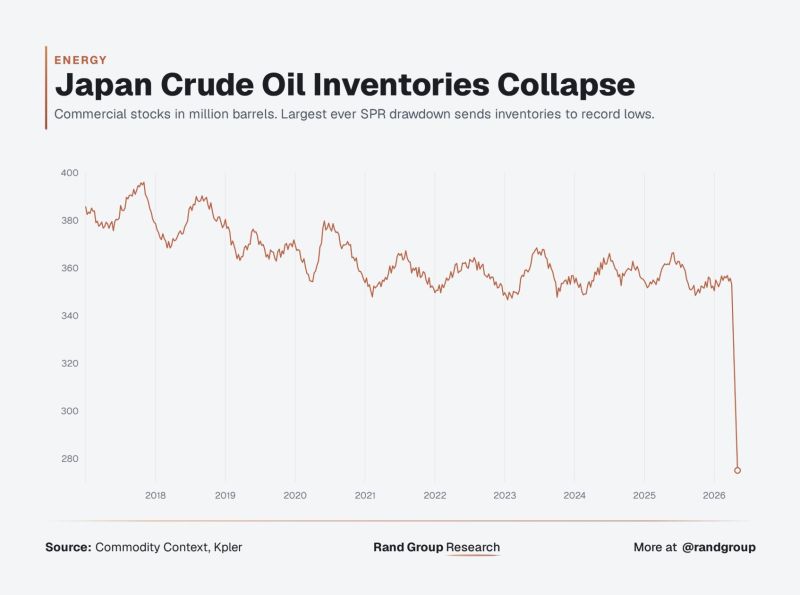

Japan's Crude Oil reserve was built in 1980.

Took 45 years to fill. Took 8 weeks to drain. Source: Rand Group

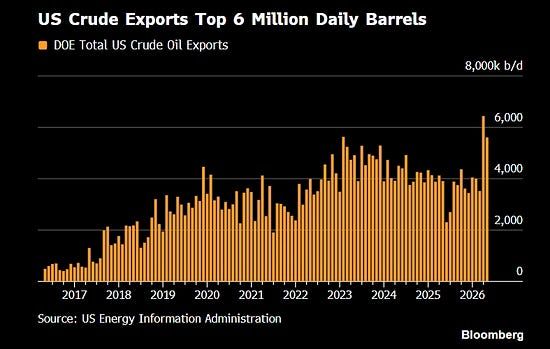

The US is exporting its SPR releases.

Source: Lukas Ekwueme

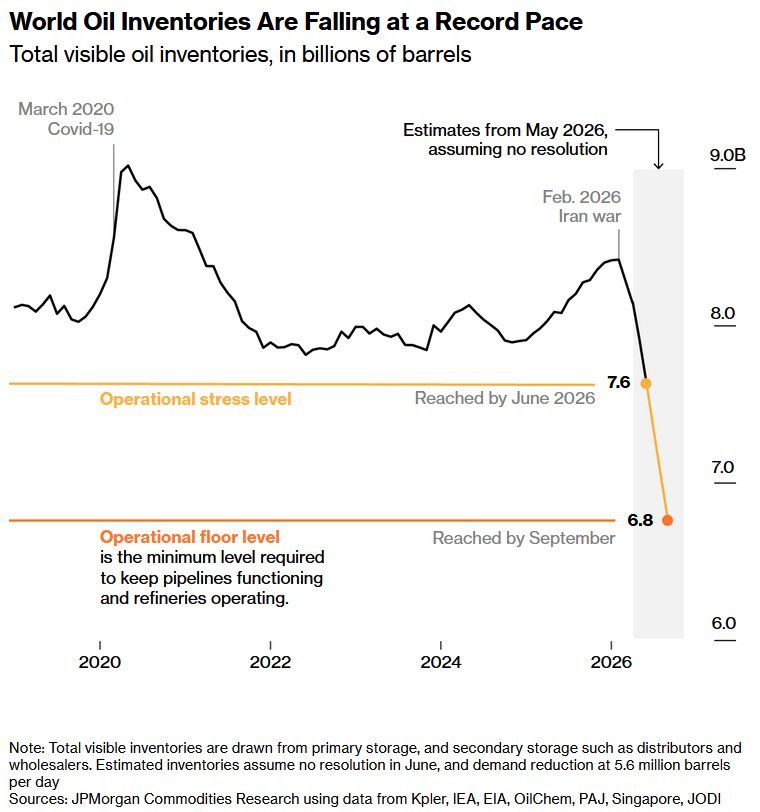

Global oil inventories have fallen to 7.6 billion barrels since the Iran war began

Source: Stocks World