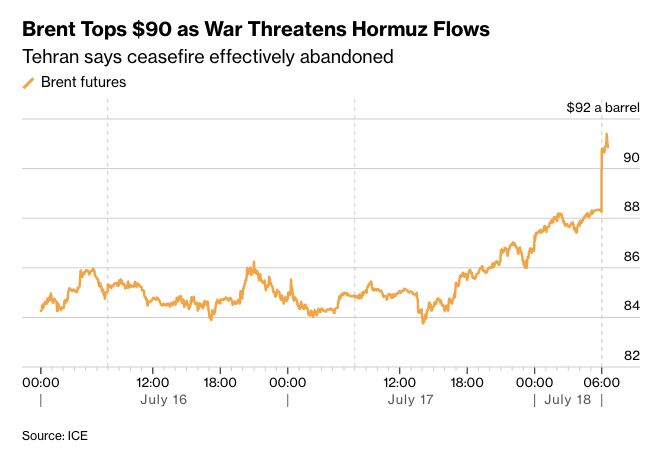

BRENT CRUDE OIL JUST JUMPED BACK OVER $90 PER BARREL

Source: Evan @StockMKTNewz Bloomberg

Hedge Funds going long oil at the fastest pace in a decade

Source: Barchart

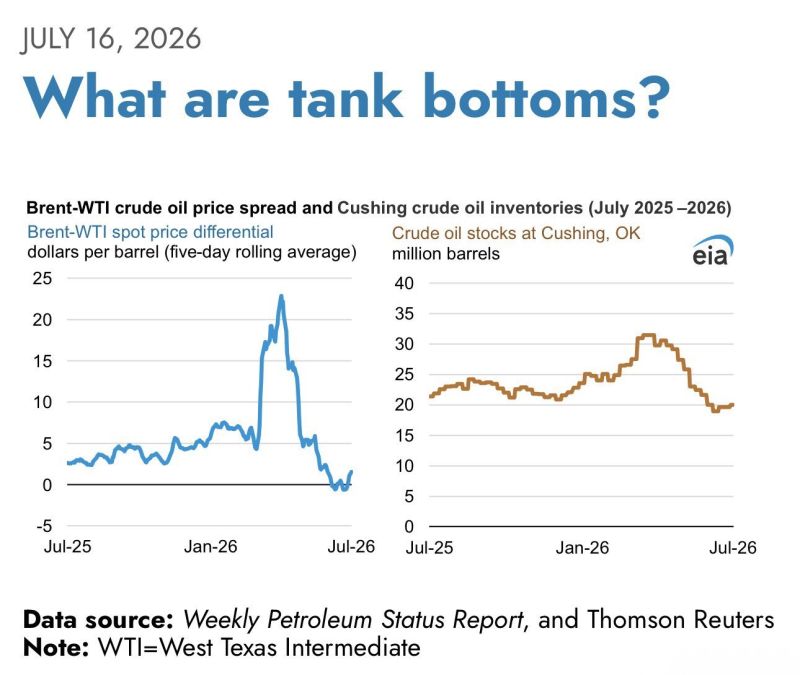

The EIA just published a warning today that reported Cushing inventory may overstate how many barrels are actually usable as stocks approach tank bottom levels.

This is the exact mechanism from the storage schematic covered in the below post. The suction line near the bottom of a tank means the last portion of reported inventory was never really accessible. If Cushing tightens further, the headline barrel count will look higher than what the market can actually draw on. Watch operationally accessible barrels. Source: Jack Prandelli on X

Strait of Hormuz 🇮🇷 oil crossings (in white) have not recovered, yet oil prices (in blue) are near the levels they were pre-war.

Source: Gordon Johnson

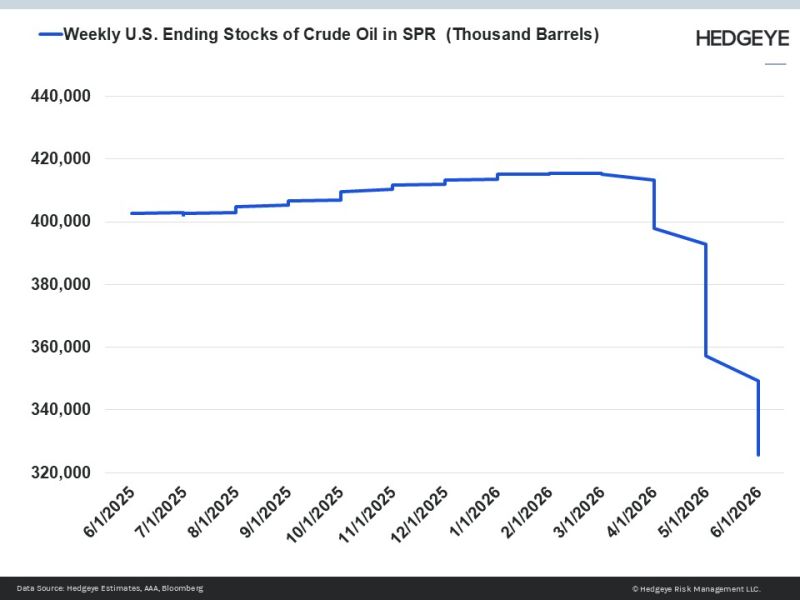

U.S. Strategic Petroleum Reserve (SPR) stocks fall to 43-year low

Source: Hedgeye

Saudi Arabia cut the price of its main crude grade for Asian customers, effective August, amid weakening demand and easing tensions.

It's the largest reduction in over two decades. The sharp price cut comes as pressure grows on the world's largest crude exporter, as softer demand in Asia coincides with improving supply conditions following the easing of geopolitical tensions in the Middle East.Source: The Times Of India

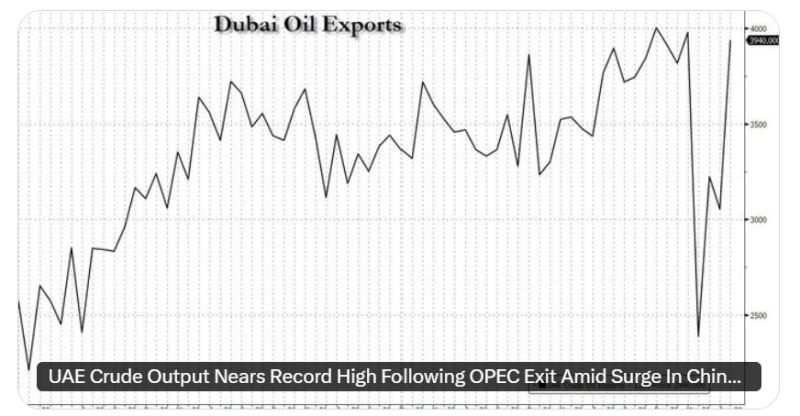

UAE Crude Output Nears Record High Following OPEC Exit Amid Surge In Chinese Buying

Source: zerohedge

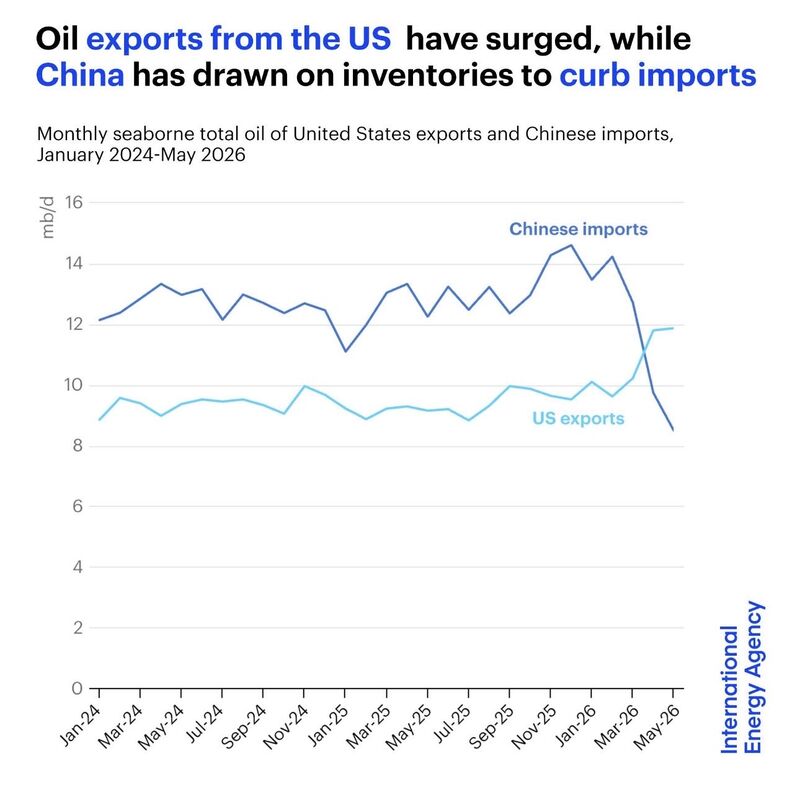

One chart may have just revealed a major shift in the global energy order.

For the first time in history, U.S. oil exports have surpassed China's crude oil imports. At first glance, it looks like just two lines crossing on a chart. In reality, it could mark a profound structural change. For two years, China's crude imports hovered around 12–14 million barrels per day. Then they suddenly plunged to roughly 8.5 million. At the same time, U.S. oil exports, long stuck around 9–10 million barrels per day, surged above 12 million. Why? China didn't stop buying oil because demand disappeared. It stopped because supply became constrained. • Nearly 38% of China's crude imports depended on the Strait of Hormuz. • Gulf producers faced major disruptions. • Russia was already exporting at full capacity. • U.S. light sweet crude isn't an ideal substitute for many Chinese refineries. With few alternatives, China began drawing down strategic inventories instead of importing. That collapse in imports isn't necessarily a sign of weaker demand. It may be evidence of a country relying on its emergency reserves to navigate one of the biggest supply shocks in years. Meanwhile, U.S. exporters stepped in to replace part of the missing Gulf supply. Sometimes, the most important geopolitical shifts don't make the front page. They simply appear when two lines cross on a chart. Source. Jack Prandelli on X, IEA