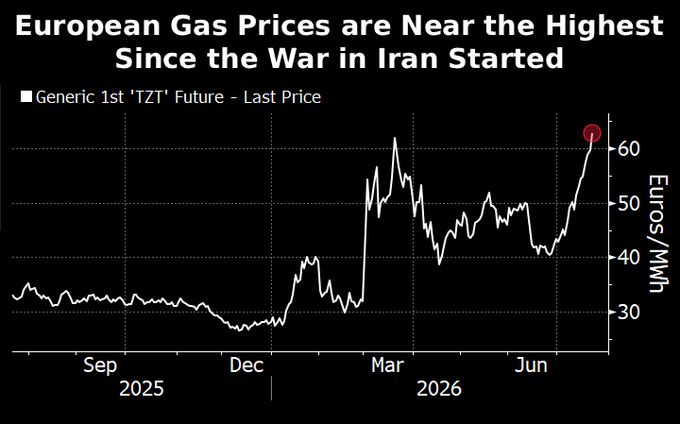

European gas futures are back near their highest level since the Iran war started

The reason: Europe is losing the LNG bidding war. Imports down 35% y/y over the last month; China's up 8%. TTF is back near its post-Iran-war high — not because Europe wants more gas, but because it has to pay up to get any. The cargoes aren't disappearing, they're just sailing east. US exporters are indifferent to which. Source: Jack Prandelli on X, Bloomberg

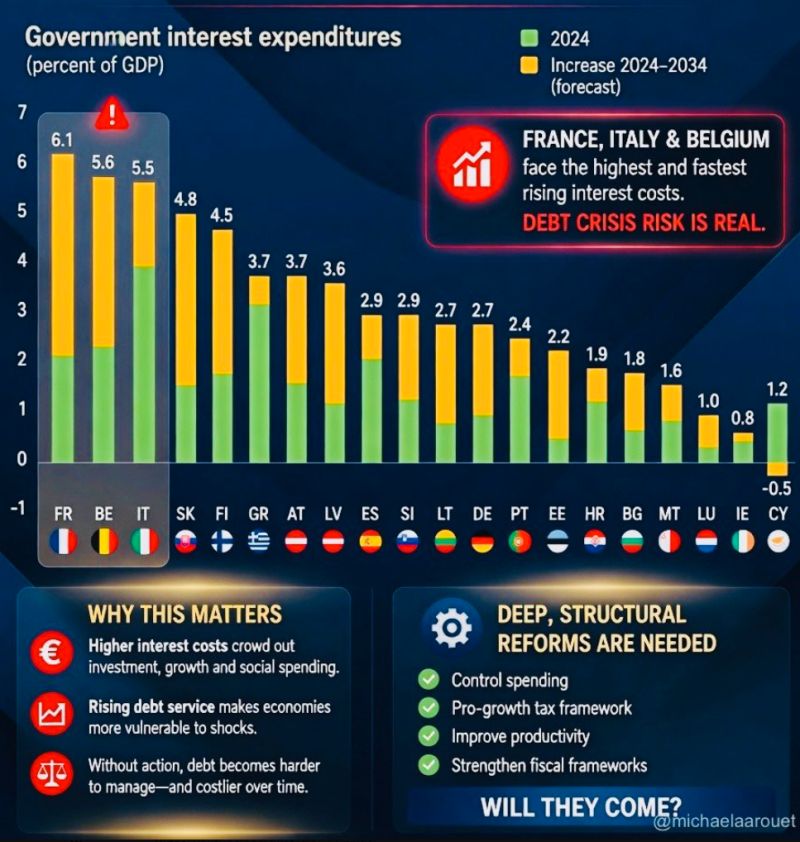

Are France, Italy & Belgium heading into a debt crisis ???

Government interest expenditures (as a & of GDP) is forecasted to explode in the coming years. There are only two options left for them: 1. They cut spending and implement business friendly pro-growth policies 2. They will face a debt crisis. The first Euro crisis was about hundreds of billions, the next one will be about trillions Which one will it be? Source: Michel A.Arouet

BREAKING: President Trump just ordered to immediately halt all trade with Spain.

Trump made the remarks during a NATO meeting while standing next to NATO Secretary General Mark Rutte. Trump's core complaint is that Spain refuses to pay its NATO defense spending commitments. While Germany, France, the UK, and Italy have all been contributing, Spain has openly resisted meeting the 2% GDP defense spending target that NATO members are required to hit. Trump said he tested NATO members during the Iran conflict to see which ones would show up and support the US. Spain did not. "Spain is a terrible partner in NATO. They don't participate, they don't pay." "Cut off all trade with Spain immediately. Don't even talk to them. Including visits." Spain is one of the US's significant trading partners in Europe. The US exports roughly $16 billion worth of goods to Spain annually. Trump is threatening to end that entirely over NATO non compliance. "They make so much money with us and we are going to see that they make a lot less." Source: Bull Theory @BullTheoryio

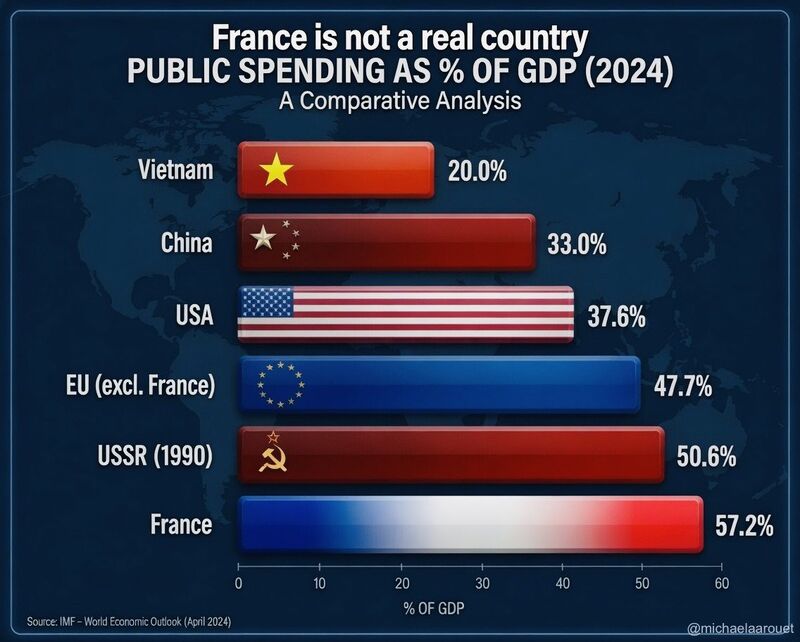

France has higher public spending as % of GDP than the Soviet Union, and now they seriously demand new taxes at the EU level to finance their absurd public spending?

Germans were just told that they need to work much longer before retiring, why should the French retire so early? Source: Michel A.Arouet

As expected, the ECB hiked rates by 25 basis points the first increase since 2023.

The ECB lifted its main refinancing rate to 2.40% and its deposit facility rate to 2.25%, citing inflation pressures following an Iran conflict-driven energy shock that pushed eurozone inflation to 3.2%. The surprise move comes as the eurozone economy shows signs of weakness, with GDP contracting 0.2% in Q1. Policymakers said the hike is aimed at preventing higher energy prices from becoming embedded in broader inflation. While this may draw criticism from some given the current growth context, the Bank actually has little choice. Unlike the Fed’s dual mandate of inflation and employment, the ECB has a single mandate: price stability. Note a big jump in the ECB's 26/27 inflation forecasts, offset by a drop in GDP forecasts HICP 2026: 3.0%, from 2.6% in March HICP 2027: 2.3%, from 2.0% HICP 2028: 2.1%, from 2.0% GDP 2026: 0.8%, from 0.9% GDP 2027: 1.2%, from 1.3% GDP 2028: 1.5%, from 1.4%

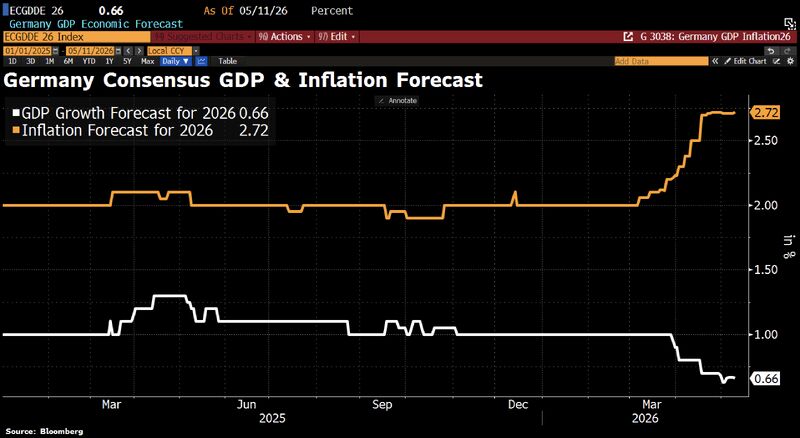

Germany appears to be heading towards stagflation.

Consensus GDP forecasts for 2026 have been revised down from more than 1% to just 0.66%, while inflation forecasts have climbed above 2.7%. Against this backdrop, the ECB is now expected to raise interest rates twice – at least, that is what markets are pricing in. Source: HolgerZ, Bloomberg

In Germany, deeply negative energy prices due to solar glut are forcing a rethink of the energy transition

Economy Minister called to end subsidies for excess renewable electricity after costs ran into the tens of millions last weekend alone. Source: Bloomberg, HolgerZ

🔴America's valuation premium over Europe is historically WIDE:

The S&P 500 trades at a forward price-to-earnings (P/E) ratio of ~21 times, while the Stoxx Europe 600 trades at ~14 times. This brings the valuation gap up to ~7 points, the widest since at least the 2008 Financial Crisis. This comes as the Middle East war exposed Europe's structural vulnerability to energy shocks, turning what looked like attractive valuations into a value trap. At the same time, the US benefited from its relative energy independence and surging tech sector. Source: FT, Factset, Global Markets Investor