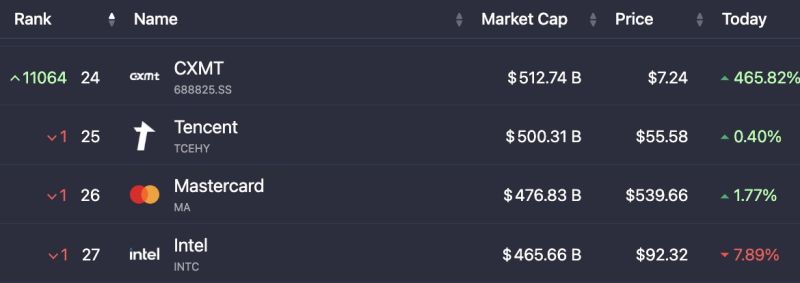

CXMT is the largest Chinese maker of memory chips. Its shares surged +472% in its trading debut.

CXMT opened at ¥49.50 vs its IPO price of ¥8.66. The company raised ¥57.92 billion ($8.6B) in Asia's largest IPO of 2026. CXMT's market value surged to about ¥3.3 trillion ($487B), up from $85.5 billion at its IPO valuation. CXMT is now larger than Intel $INTC and is reportedly now the largest Chinese public company, overtaking ICBC. Based on sales figures for the fourth quarter of 2025, CXMT held a 7.67% share of the global DRAM market in 2025, according to its IPO prospectus. DRAM chips are used in electronic devices ranging from smartphones to servers. The global DRAM market is dominated by Samsung Electronics, SK Hynix, and Micron Technology. The listing comes at a time when CXMT has seen increased attention, following reports earlier this month that Apple has begun testing the Chinese chipmaker’s DRAM for devices sold in China. CXMT swung to an operating profit of 35.43 billion yuan in the first quarter from a loss of 2.83 billion yuan a year earlier, as it saw continued growth in global computing power demand and capacity allocation by major manufacturers. Morningstar said in a note Friday that as AI is increasingly becoming an issue of national security for China, CXMT will likely be a key beneficiary. The research firm added that while CXMT’s technology still lags global memory leaders, domestic internet giants spearheading AI development will likely drive robust adoption of its chips as Beijing pushes for semiconductor self-sufficiency. CXMT, founded in 2016 by Chairman Zhu Yiming, plans to boost its technological capabilities and core competitiveness, primarily memory wafer mass production and R&D projects, by employing the IPO proceeds, according to a Google translation of the information in the prospectus. Source: Bull Theory, Evan on X, CNBC

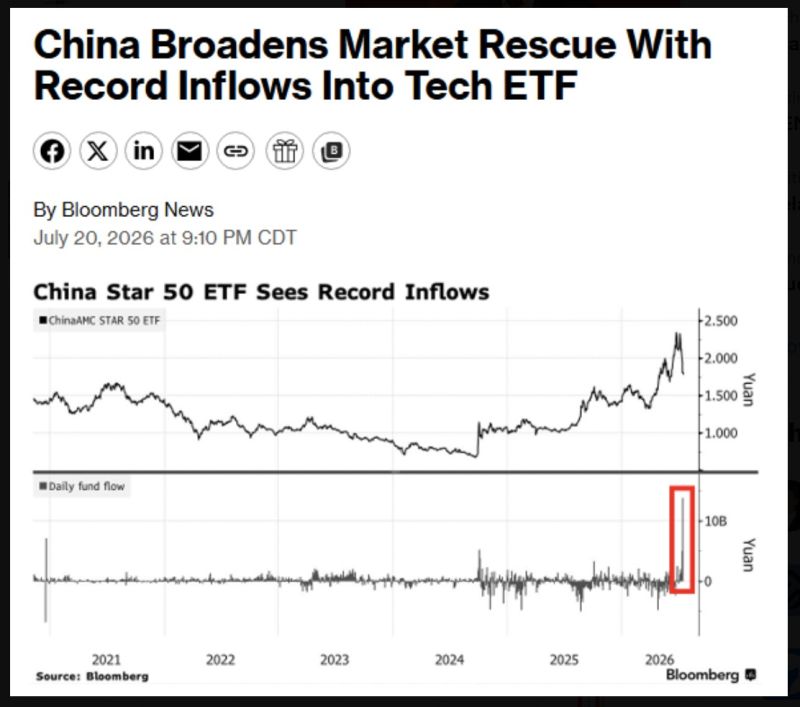

China's government just pumped 13.8 Billion Yuan ($2 Billion USD) into their largest ETF tracking semiconductor stocks, the fund's largest inflow in history

Bloomberg, Barchart

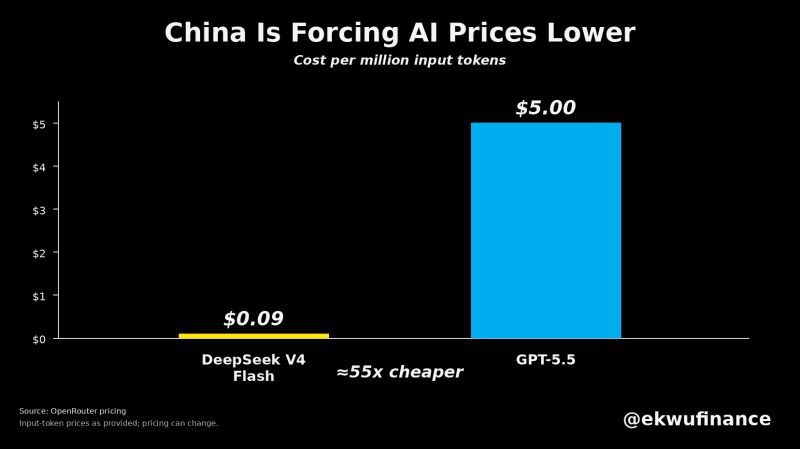

China is forcing AI prices lower

DeepSeek V4 Flash costs $0.09 per million input tokens. GPT-5.5 and Claude Opus 4.8 cost around $5. That's ~55× cheaper. Source: Lukas Ekwueme

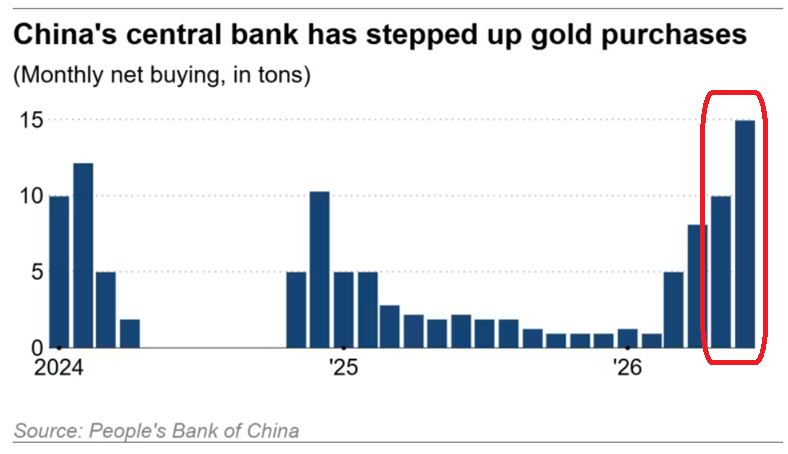

China's gold purchases are ACCELERATING:

China's central bank acquired +15 tonnes of gold in June, the largest monthly purchase in at least 2.5 years. This also marks the 20th consecutive monthly addition. Year-to-date, the country has increased its gold reserves by a total of +40 tonnes. This lifts China's total gold reserves to a record 2,346 tonnes, or 9% of its total FX reserves, near an all-time high. China is extremely bullish on gold. Source: Global Markets Investor

In case you missed it... China's factory inflation hits a near 4-year high.

China's Producer Price Index (PPI) rose 4.1% YoY in June, the highest reading since July 2022 and the 4th consecutive monthly increase. Consumer inflation slowed to 1.0% from 1.2% in May, highlighting weak domestic demand even as manufacturers face rising input costs. Higher energy prices during the Iran conflict were the main reason producer prices increased. Source: Bull Theory, FT

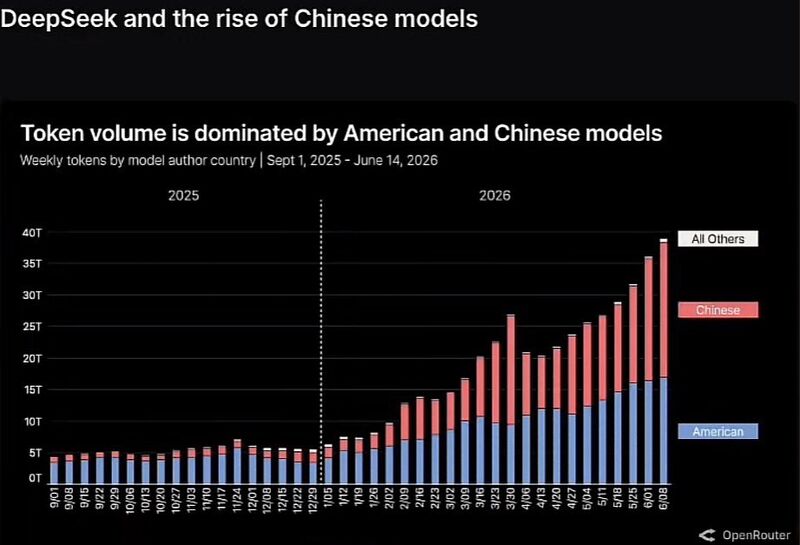

In 2025 American AI dominated with 90% market share.

Today Deep Seek and other AI open source Chinese AI has overtaken the US and now control about 52% of the market. Why? Because Chinese AI is much cheaper. Source: QE Infinity

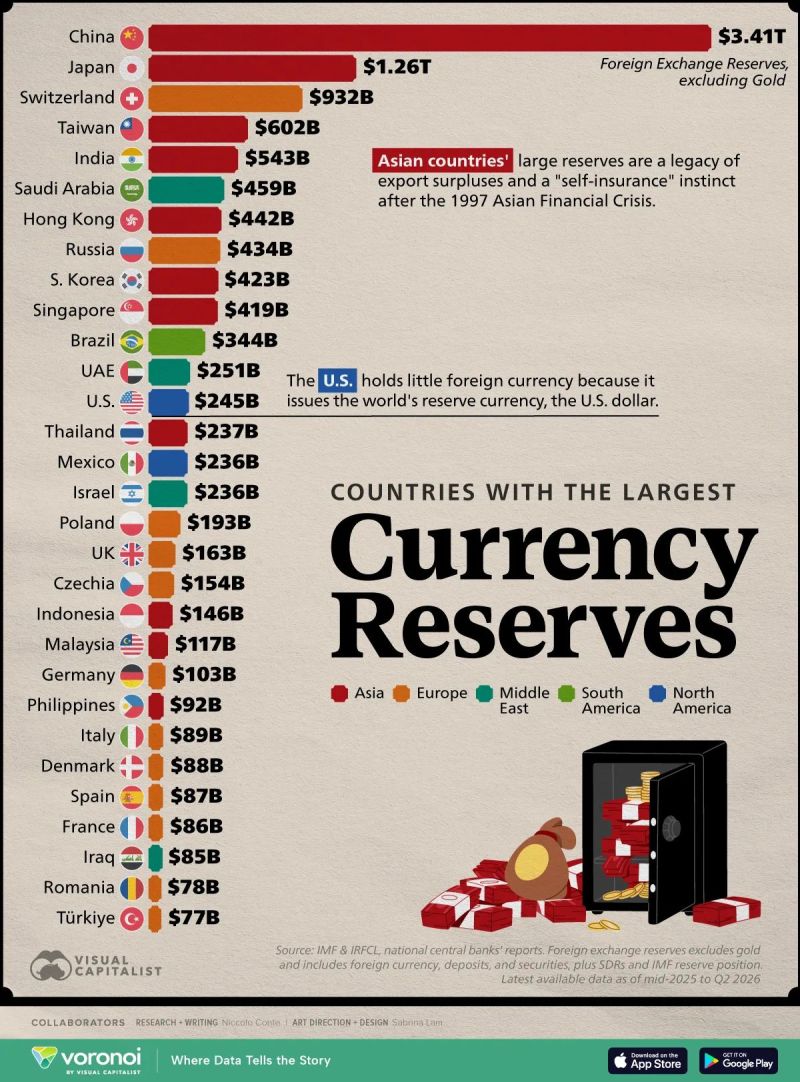

Ranked: Countries with the Largest Currency Reserves

China holds over $3.4 trillion in foreign exchange reserves, nearly 3x more than Japan. Seven of the world’s 10 largest reserve holders are in Asia, reflecting decades of export-led growth. Despite being the world’s largest economy, the U.S. ranks only 13th because the dollar is the world’s primary reserve currency. Source: James Wong, Visual Capitalist

🚨 The AI race is entering a new phase.

Not because demand is slowing. Because costs are becoming impossible to ignore. Here are the numbers: 📈 Chinese AI models now process ~18.5 trillion tokens per week on OpenRouter. 🇺🇸 US models? Around 6 trillion. That's a 3x gap. Why? • Lower energy costs. • More efficient models. • Aggressive pricing that's reshaping the competitive landscape. Meanwhile, something interesting is happening inside large enterprises. Companies including Amazon, Walmart, Cisco, Uber, and Meta are reportedly introducing internal limits on AI usage as spending exceeds expectations. One striking example: A software company saw its AI bill jump 7x overnight after moving from a flat-rate subscription to usage-based pricing. Suddenly, the true cost of AI became visible. And this is only the beginning. 📊 Goldman Sachs estimates AI agents could increase token consumption by 24x by 2030. That creates a fundamental challenge: AI demand may keep exploding... while AI budgets become increasingly constrained. The next competitive advantage won't just be building the smartest models. It will be building the most cost-efficient ones. The AI story is evolving: ➡️ From "Who has the biggest model?" ➡️ To "Who delivers the lowest cost per useful output?" The winners of the next AI wave may not be those with the most compute... ...but those who make intelligence affordable at scale. Do you think AI spending is finally reaching a reality check, or is this just a temporary pause before the next investment wave? Source: FT, Global Markets Investors