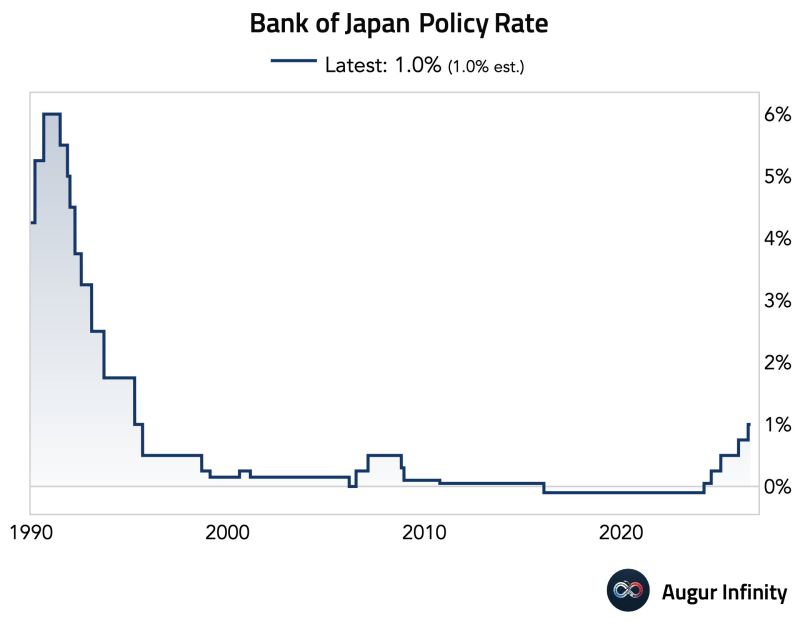

Bank of Japan ) keeps rates unchanged at 1% However, it warned that core inflation was likely to exceed its 2% target from September.

The move comes as Japan reportedly conducted an intervention to strengthen the yen on Thursday night. • The Bank of Japan kept its policy rate unchanged at 1% in an 8-1 vote on Friday, in line with market expectations, after raising rates to their highest level since 1995 last month. • Board member Naoki Takata dissented, calling for an immediate 25-basis-point hike, citing upside inflation risks and changing global financial conditions. • The BOJ said it will continue to raise rates if economic activity, inflation and financial conditions evolve as expected, adding that underlying inflation is now close to its 2% target. • In its latest outlook, the central bank lowered its FY2026 core CPI forecast to 2.5% from 2.8% and raised its FY2026 GDP growth forecast to 0.6% from 0.5%. FY2027 GDP growth forecast is raised to 0.8% from 0.7% 🏦BoJ Says: Significant downside risks to economy activity & significant upside risks to prices have decreased. In its outlook, the BOJ said that core inflation was likely to accelerate to a level “clearly above” 2% from the second half of its 2026 fiscal year, which runs from September to March. It cited wage increases being passed along into selling prices, the rise in crude oil prices and the recent depreciation of the yen. Inflation should then come down toward 2% as crude oil prices decline, it said. Japan’s core inflation for July came in at 1.6%, and has been below 2% for most of 2026. The decision comes as Tokyo reportedly conducted an intervention on Thursday night, in conjunction with U.S. authorities executing a “rate check,” a move usually seen as a precursor to intervention. Peter Schiff: "The BoJ’s decision to hold rates at 1%, with only the possibility of a quarter-point hike by year-end, ensures a weaker yen, rising inflation, and higher long-term interest rates, ultimately forcing the BoJ to hike much more in the future, with even more adverse consequences". Source: Augur Infinity

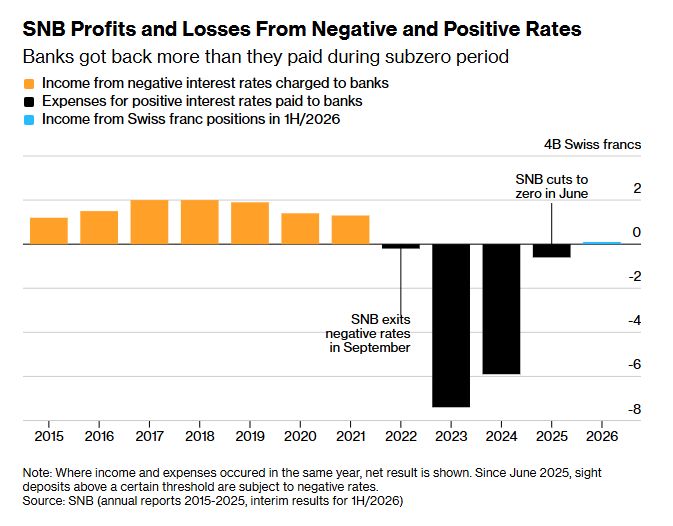

The Swiss National Bank reported a solid six-month profit, as gains from the global stock-market rally and a weaker franc offset the drop in value of its gold holdings.

The SNB earned 25.2 billion francs ($31.2 billion) from January through June, it said in a statement on Friday. That brings a year-end payout to the Swiss government back into focus after the first quarter resulted in a small loss. Source: Bloomberg

The Dow Jones Industrial Average closed 1,153.18 points lower, or 2.19%, for its worst decline since April 2025

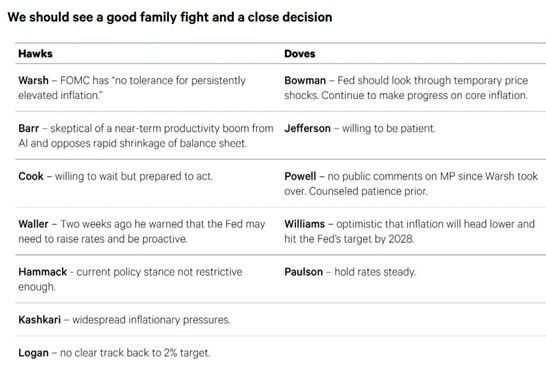

Stocks tumbled for a myriad of reasons Wednesday, but mostly because the bond market signaled the Federal Reserve could be falling behind on the inflation fight as the central bank chose to keep interest rates unchanged. The S&P 500 slid 1.52%. The Nasdaq Composite fell 1.74% to 24,442.94, ending the session more than 10% off its all-time high. The Fed kept to the sidelines in its latest rate decision, and the bond market responded with the 10-year Treasury yield jumping 7 basis points to above 4.67%. The 30-year Treasury yield soared 10 basis points to above 5.2%, hitting its highest level since 2007. Three officials wanted a hike, but the Fed still stood pat on rates. And Fed Chairman Kevin Warsh’s tough talk failed to convince the bond market.

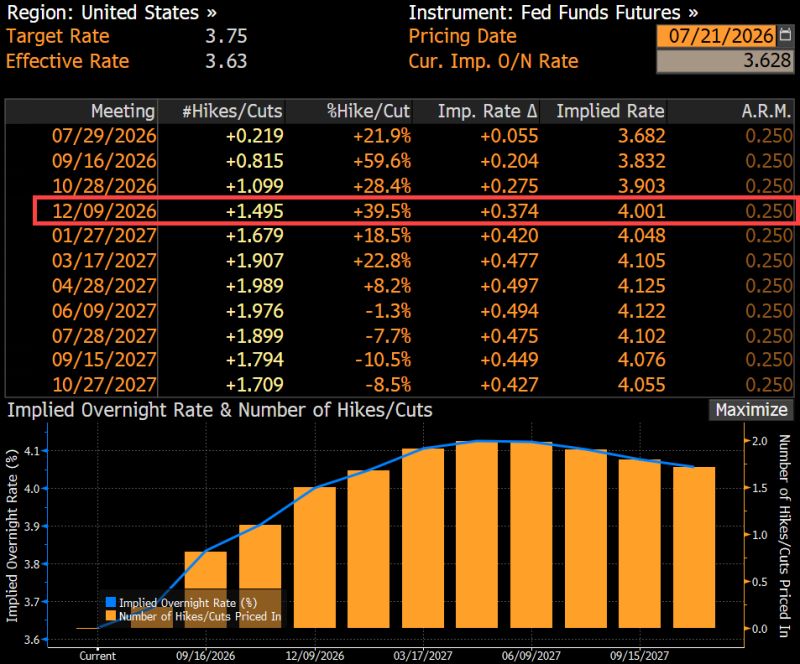

NDR's latest assessment suggests the market may be underestimating the risk of a near-term Fed rate hike.

Their view is that several Fed governors remain concerned about inflation and are reluctant to ease policy too soon, fearing it could undermine the Fed's inflation-fighting credibility. In other words, preserving credibility may take priority over delivering the rate cuts markets are expecting. Source: NDR

The futures market is now pricing 1.5 Fed rate hikes by year-end

Source: Hedgeye, Bloomberg

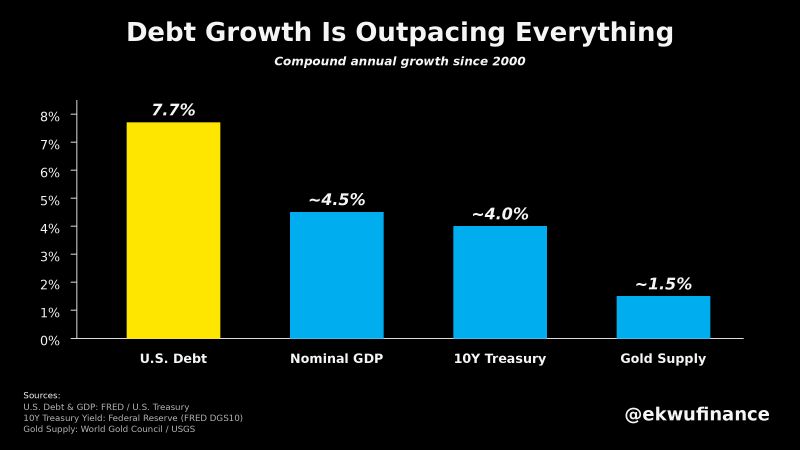

U.S. debt has been growing much faster than the economy for over two decades

Since 2000, U.S. debt has compounded at 7.7% annually, far outpacing nominal GDP (~4.5%) and the 10-year Treasury yield (~4%). Meanwhile, gold supply has expanded by only about 1.5% per year. For central banks, the contrast is striking: one asset becomes increasingly abundant as debt issuance accelerates, while the other remains structurally scarce. That helps explain why many central banks have been steadily increasing their gold holdings in recent years. Source: Lukas Ekwueme @ekwufinance

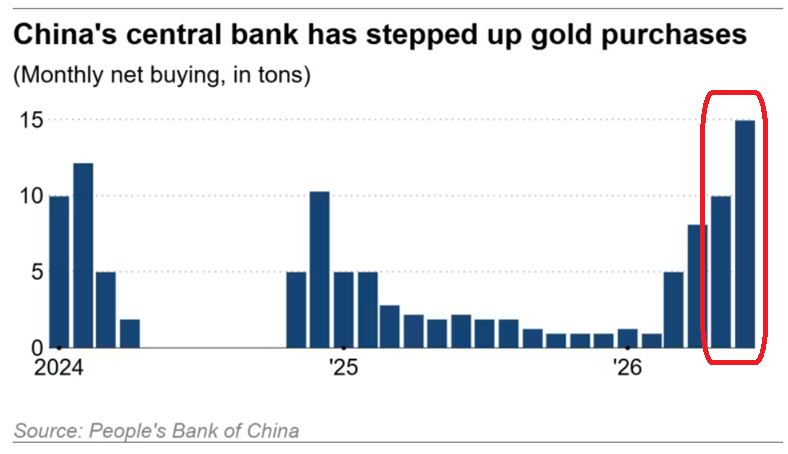

China's gold purchases are ACCELERATING:

China's central bank acquired +15 tonnes of gold in June, the largest monthly purchase in at least 2.5 years. This also marks the 20th consecutive monthly addition. Year-to-date, the country has increased its gold reserves by a total of +40 tonnes. This lifts China's total gold reserves to a record 2,346 tonnes, or 9% of its total FX reserves, near an all-time high. China is extremely bullish on gold. Source: Global Markets Investor

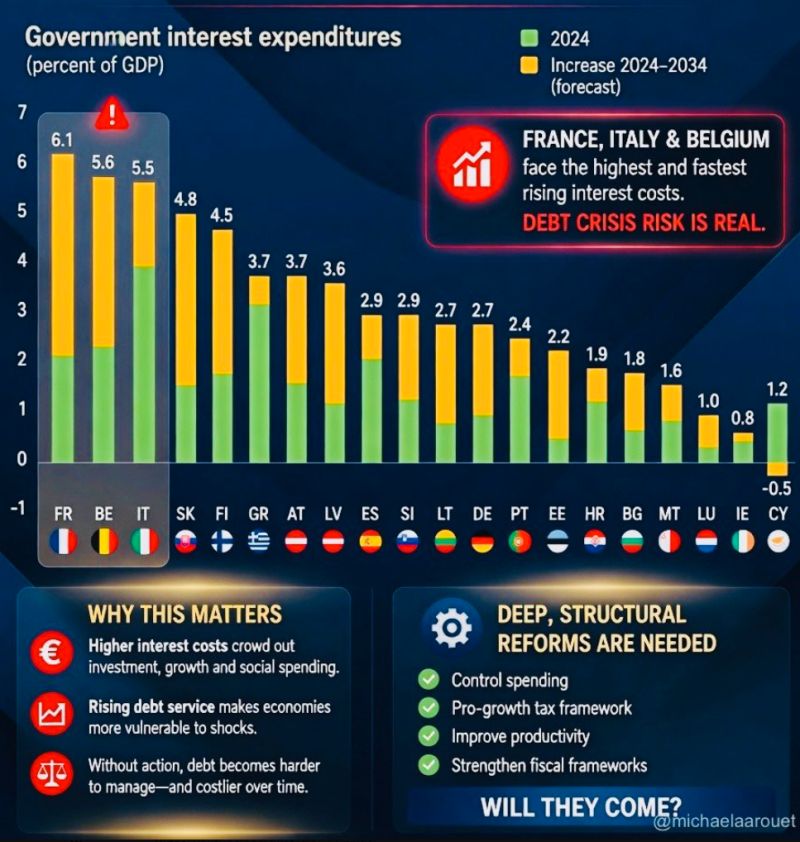

Are France, Italy & Belgium heading into a debt crisis ???

Government interest expenditures (as a & of GDP) is forecasted to explode in the coming years. There are only two options left for them: 1. They cut spending and implement business friendly pro-growth policies 2. They will face a debt crisis. The first Euro crisis was about hundreds of billions, the next one will be about trillions Which one will it be? Source: Michel A.Arouet