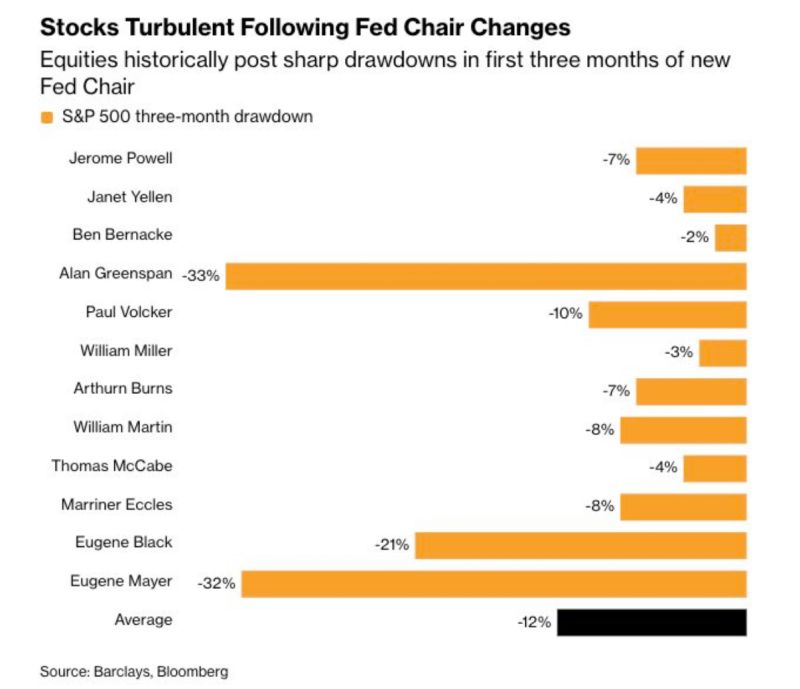

Today is officially Kevin Warsh's first day as the Fed chair.

Since 1930, the US stocks benchmark has seen an average 12% drawdown in the first 3 months after a new Fed chair has been elected. Source: Bloomberg, Barclays

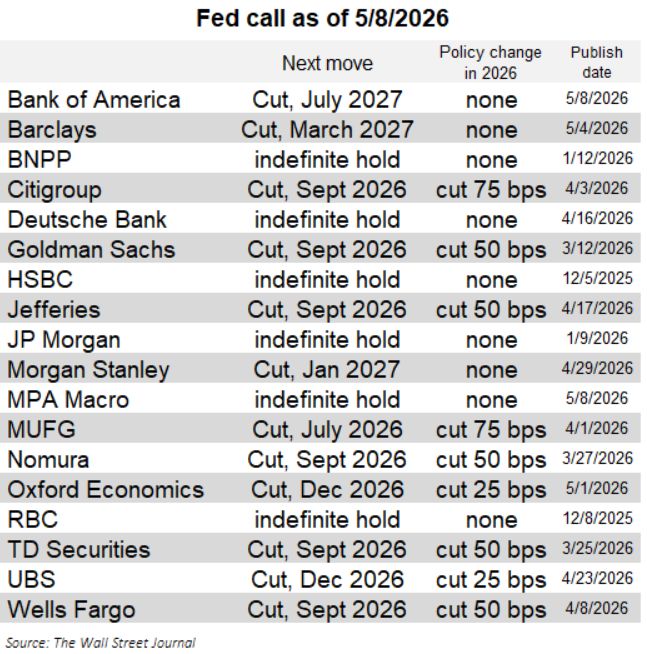

Fed IRP (Interest Rate Probabilities) is telling us ~¾ of a hike is priced in for Dec2026.

August of 2024 the market was expecting 10 cuts… Source: Bloomberg, RBC

More sell-side firms and Fed watchers are removing/delaying cuts from their outlook, including a couple forecasters after the April NFP.

Half now see no cuts this year (and risks are clearly tilted to this group continuing to grow given inertial nature of these forecasts). Source: Nick Timiraos

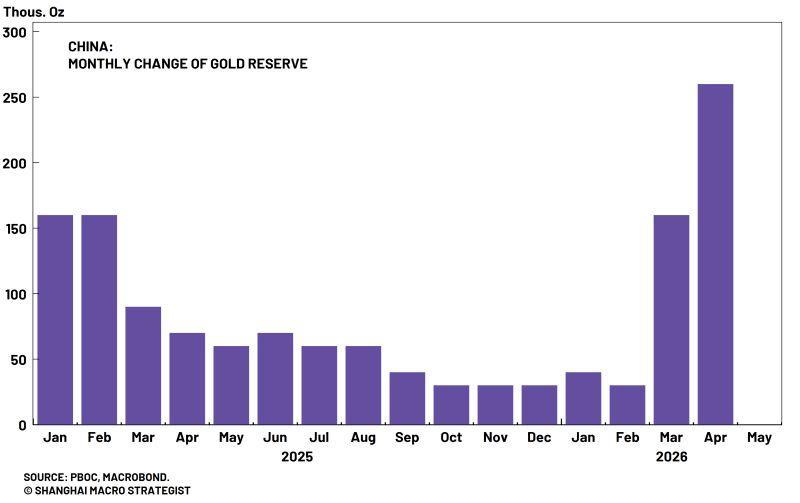

The Chinese central bank remains the most unwavering “buy-the-dip” force in gold.

Source: Shanghai Macro Strategist

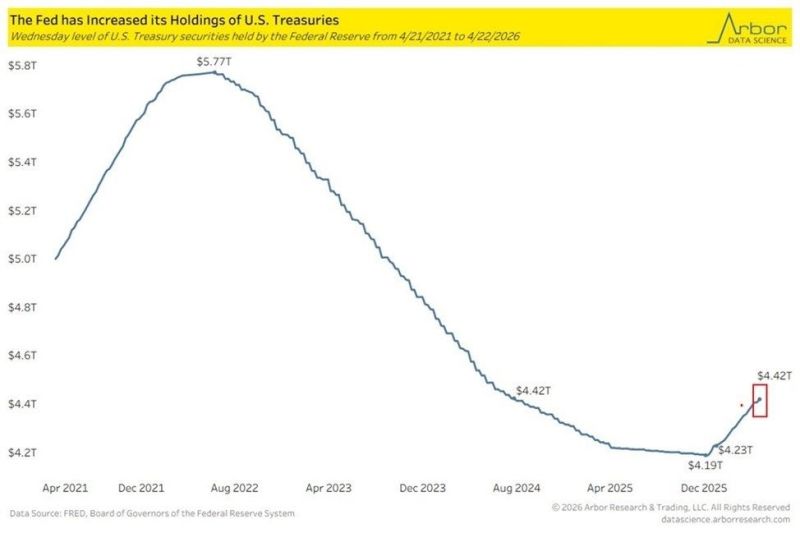

The Fed is steadily loading up on U.S. Treasuries at a pace not seen since 2008

$237 billion in purchases since December 2025. Total holdings now sit at $4.4 trillion, the highest since July 2024. More striking: Treasuries now make up 65.9% of the Fed's total assets, the highest share since March 2008. That's a central bank stepping in to hold up a bond market under pressure from record fiscal spending. The question is how long it can keep doing it before the balance sheet becomes the story. Source: Bloomberg, Arbor Data Science

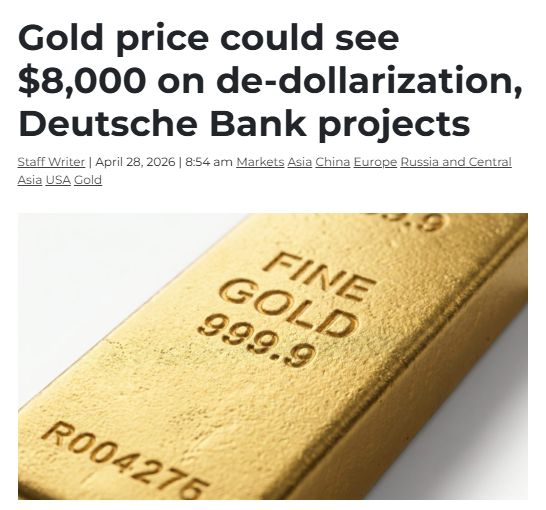

The German investment bank said it sees a scenario where central banks continue to increase their gold holdings as a financial safety net to protect themselves from Western sanctions.

These central banks have added over 225 million ounces to their reserves since the 2008 financial crisis, while their holdings of US dollars have fallen from a peak of over 60% in the early 2000s to about 40% today. Gold’s share of global central bank reserves could reach 40%, up from 30% currently, the bank predicts. At that allocation, Deutsche Bank ran a simulation that projects gold prices to hit $8,000 an ounce within five years, a near 80% rise on current levels. Source: Wall Street Mav

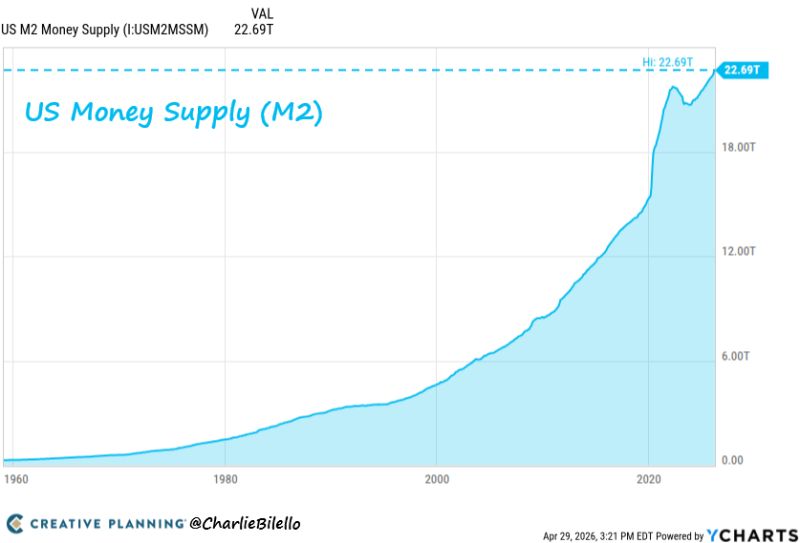

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years. Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control. The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money. Source: Charlie Bilello

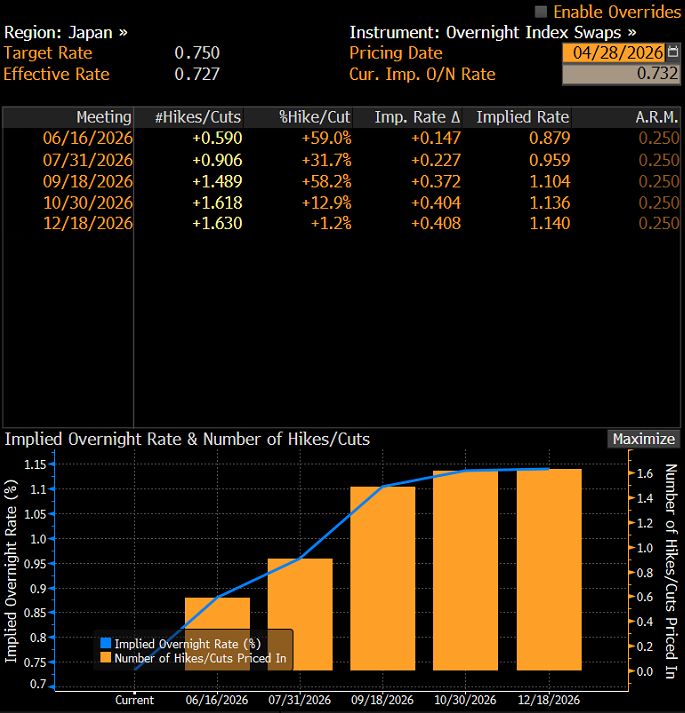

Hawkish Hold from the BOJ Amid Rising Inflation Risks

The Bank of Japan kept its policy rate unchanged at 0.75% in a split 6–3 decision, with three members pushing for a hike to 1% as Middle East tensions raise upside inflation risks. The bank sharply revised its 2026 core CPI forecast to 2.8% (from 1.9%) while cutting growth expectations to 0.5% (from 1%). Markets are now pricing in 15bps of tightening by June, the yen is strengthening toward 159, and the Nikkei 225 is down around 1%, as higher oil prices threaten profits and household incomes. Source: Joumanna Nasr Bercetche (@JoumannaTV)