🚨 Very interesting note by Eric Balchunas: Has the US stock market become "too important to fail"?

More than 55% of Americans now own stocks, the highest participation rate in the world. With new retirement programs bringing millions more investors into the market, Wall Street is becoming deeply intertwined with household wealth, retirement security, and even politics. The implication is profound: future policymakers may face overwhelming pressure to prevent prolonged bear markets. Some believe that, in the next major crisis, the Federal Reserve could even follow Japan and China by purchasing equity ETFs to stabilize markets. Whether or not that happens, one thing is clear: the growing financialization of the US economy is reshaping how investors think about downside risk—and may help explain why markets continue to recover so quickly after every sell-off. Source: Eric Balchunas, Bloomberg

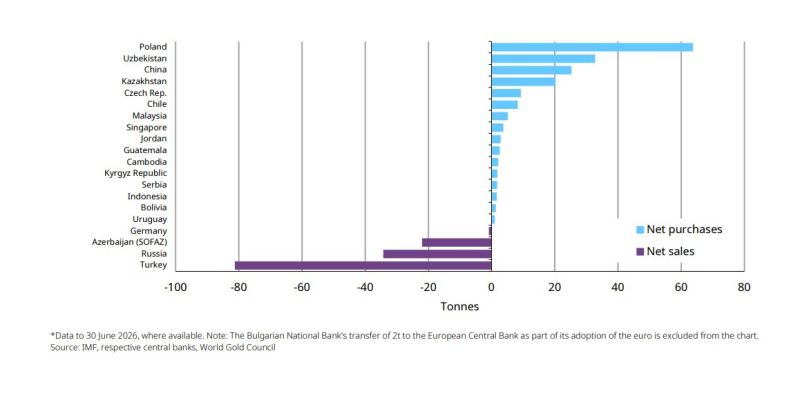

Central banks just doubled their gold buying in a single month.

The World Gold Council reported net central bank gold purchases of 41 tonnes in May, more than double April's 19 tonnes. Poland was the biggest buyer, adding 18 tonnes in May, bringing its 2026 total to 64 tonnes. Its reserves now stand at 614 tonnes. China added 10 tonnes, its biggest monthly purchase since December 2024 and its 20th straight month of buying. Total Chinese reserves now sit at 2,331 tonnes. Turkey was the only major seller, offloading 3 tonnes in May, extending its 2026 net sales to 81 tonnes as it draws on reserves to defend the lira. The 2026 Central Bank Gold Reserves Survey shows 89% of central banks expect global gold reserves to increase over the next 12 months. A record 45% plan to increase their own holdings. Gold gained +2% last week after four straight weekly declines but remains -25.4% below its peak. Source: Bull Theory

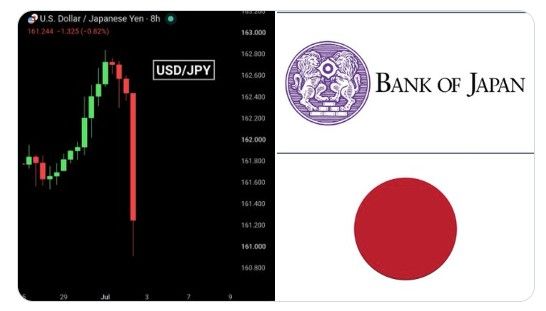

🚨 THE BANK OF JAPAN MAY HAVE STEPPED INTO THE FX MARKET AGAIN.

USD/JPY surged to a fresh 40-year high of 162.84 before plunging to 160.90 within hours. A 1.2% intraday reversal in one of the world's most liquid currency pairs is highly unusual. It mirrors what happened in April and May, when Japanese authorities spent roughly $72–73 billion selling U.S. dollars and buying yen to slow the currency's collapse. The pattern looks strikingly familiar: • New multi-decade high. • Sudden, aggressive reversal. • Speculation of official intervention. There has been no official confirmation yet. But the speed and magnitude of the move are exactly what markets expect when Tokyo steps in. Even after the sharp rebound, the yen remains close to its weakest level in four decades, keeping pressure on policymakers as imported inflation rises and global markets watch for their next move. Source: Bull Theory

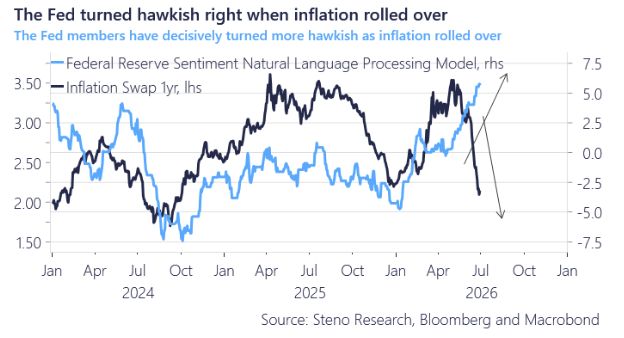

The reason for the strong USD in one chart.

The Fed turned hawkish, when inflation rolled over. Source: Andreas Steno Larsen @AndreasSteno

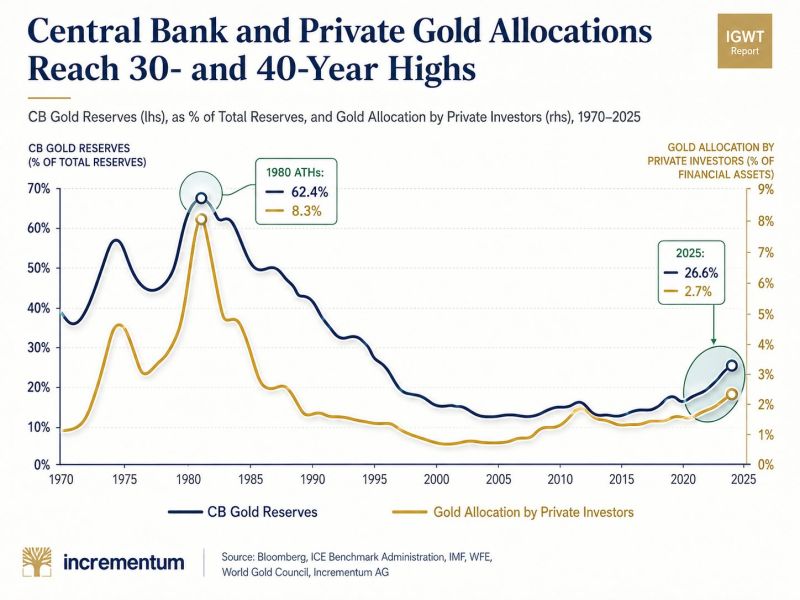

Gold allocations are at multi-decade highs, and they're still tiny.

Private investors hold just 2.7% of financial assets in gold. In 1980 it was 8.3%. Central banks sit at 26.6% versus 62.4% back then. Source: Incrementum AG, Jack Prandelli on X

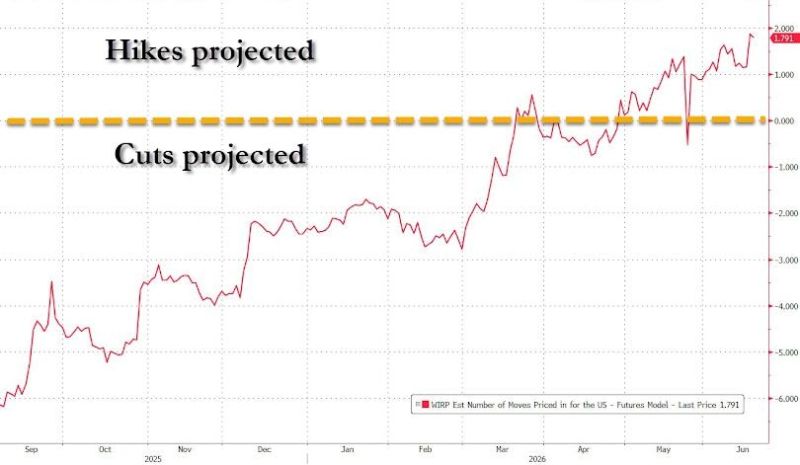

What a turnaround for Fed rates expectations (as implied by Futures). From projecting 6 cuts in September to 2 hikes now

Note that it didn't prevent equities to surge... Source: zerohedge, Bloomberg

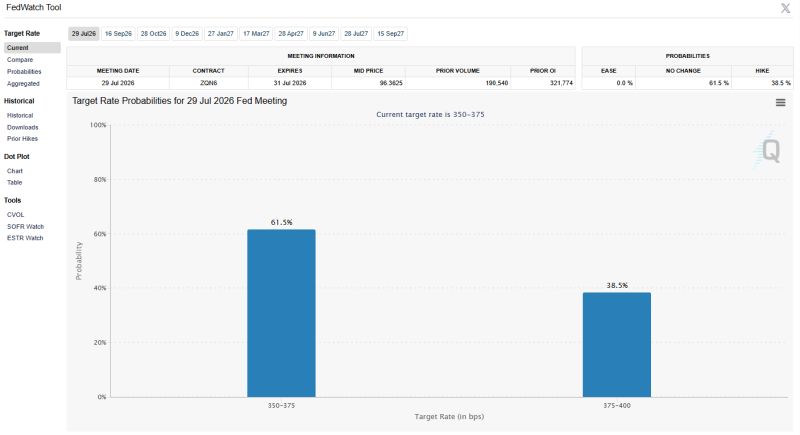

There is now a 38% chance of a rate hike at the July FOMC and a 0% chance of a rate cut

Source: Barchart

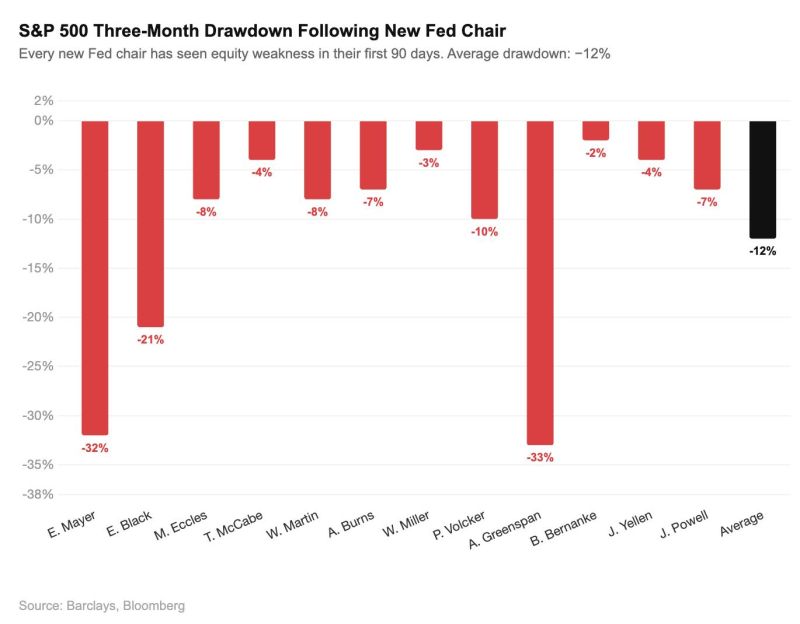

The S&P 500 has fallen under every single new Fed chair in their first 90 days.

Kevin Warsh chairs his first FOMC meeting today. The historical data goes back nearly a century across 12 Fed chairs. The average drawdown in the first three months of a new Fed chair is -12%. The worst was Alan Greenspan at -33%. The best was Ben Bernanke at -2%. Jerome Powell's first 90 days saw a -7% drawdown. Janet Yellen's saw -4%. Not one single new Fed chair has avoided a drawdown in their first three months. Warsh's 90-day clock starts today. Source: Bull Theory