Big shift in Fed dot plots with the median member now forecasting 1 rate HIKE this year when previously they were forecasting 1 rate CUT. (Clone)

The stock market may not like it but this is the right move if the Fed wants to regain any credibility as an inflation fighter. Source: Charlie Bilello @charliebilello

Kevin Warsh just chaired his first FOMC meeting. The Fed held rates at 3.5–3.75% (unanimous). No surprise there. The surprise was everything around it.

𝗙𝗼𝗿𝘄𝗮𝗿𝗱 𝗴𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝗶𝘀 𝗴𝗼𝗻𝗲. Under Powell, the Fed told markets what was coming. Warsh refused. The dots, he said, are written "in pencil." He didn't even submit his own forecast. 𝗔 𝗽𝗼𝗶𝗻𝘁𝗲𝗱 𝗯𝗿𝗲𝗮𝗸 𝘄𝗶𝘁𝗵 𝘁𝗵𝗲 𝗽𝗮𝘀𝘁. He pledged to "fix five years of misses on inflation" — a rare, direct critique of the prior Fed. The 2% target stays. The closing line, repeated all conference: "The Committee will deliver price stability." 𝗔 𝗵𝗮𝘄𝗸𝗶𝘀𝗵 𝗱𝗼𝘁 𝗽𝗹𝗼𝘁. 9 of 18 officials now see at least one HIKE by end-2026 — and 6 of them see multiple. Just one sees a cut. 𝗙𝗶𝘃𝗲 𝗻𝗲𝘄 𝘁𝗮𝘀𝗸 𝗳𝗼𝗿𝗰𝗲𝘀. Communications, the balance sheet, data, productivity & jobs, and inflation frameworks — everything under review except the 2% target. Deliverables possible by year-end. 𝗧𝗵𝗲 𝗺𝗮𝗿𝗸𝗲𝘁 𝗿𝗲𝗮𝗰𝘁𝗶𝗼𝗻? ~$1.5 trillion erased across equities, metals and crypto in 10 minutes — with NO rate change. S&P 500 −1.2% • Nasdaq −1.35% • Gold −2.22% • Silver −3.95% • Bitcoin −1.8% The takeaway: this was a hawkish shock delivered through tone, not action. A Fed that stops pre-announcing its moves is a Fed that just reintroduced volatility as a feature, not a bug. The Powell put on certainty is over. Markets are still repricing what that means. What's your read — disciplined return to price stability, or a communication vacuum that markets will punish?

“These forecasts have been abysmal. My dots wouldn’t be perfect either, so I wouldn’t give them.”

Fed Chairman Kevin Warsh has spent 15 years arguing the central bank says too much. Wednesday is his first meeting. My story on the quiet revolution he wants: Source: Nick Timiraos @NickTimiraos

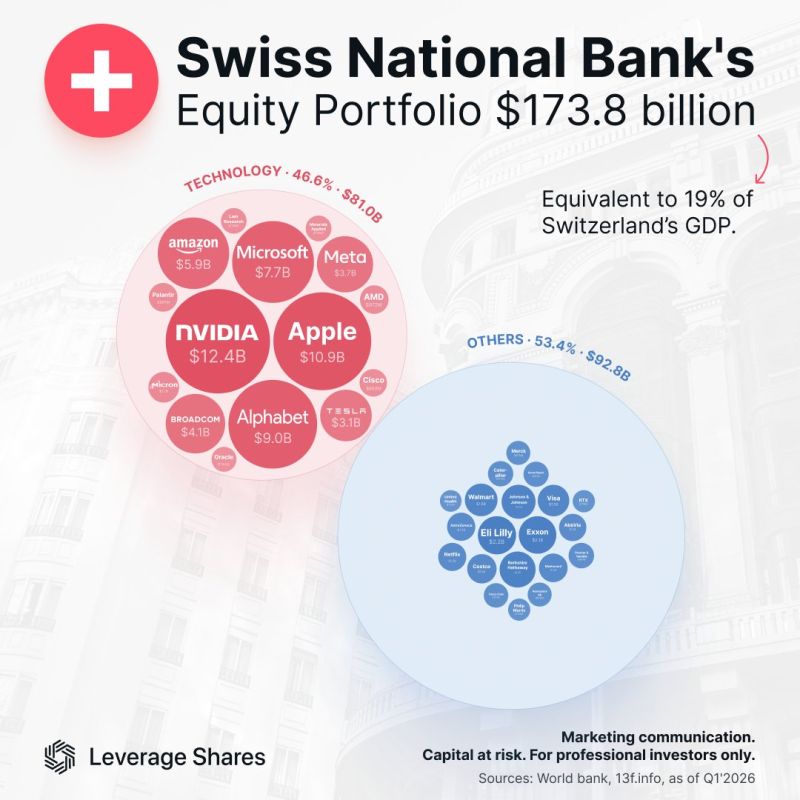

Swiss National Bank's $173B Portfolio

Source: The Market Mind

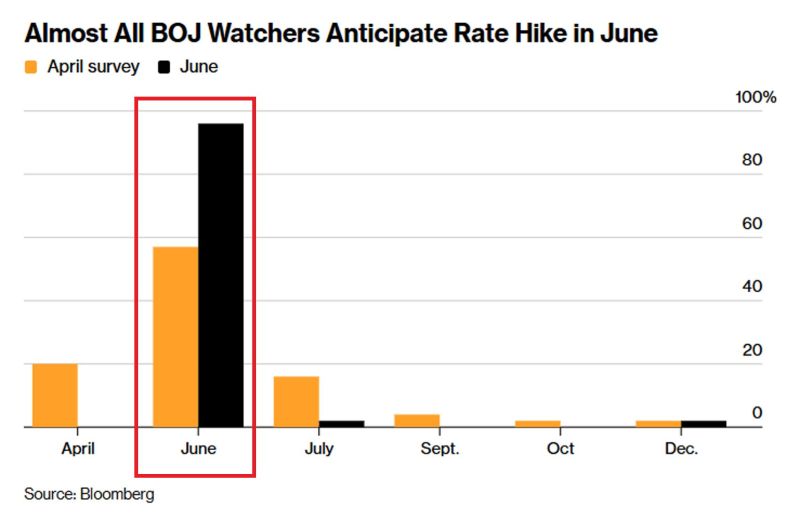

The Bank of Japan is set to HIKE RATES next week:

49 of 51 economists surveyed by Bloomberg expect the BOJ to raise its key interest rate by +25 basis points to 1.0% at its June 15-16 policy meeting. This would mark the highest level since 1995 and the first time above 1.0% in more than 3 decades. The same survey shows economists expecting a further hike to 1.25% by year-end, implying 2 rate increases in 2026 alone, with ~71% expecting hikes roughly once every 6 months. This comes as the Iran war-driven energy shock has pushed Japanese inflation risks higher, with 60% of survey respondents flagging a rising risk of the BOJ falling behind the curve in fighting inflation. The BOJ's decision on its government bond purchase reduction program will also be closely watched, with the majority of analysts expecting the central bank to slow or pause its tapering from April 2027. The Bank of Japan is gradually closing the gap with other major central banks. Source: Global Markets Investor, Bloomberg

As expected, the ECB hiked rates by 25 basis points the first increase since 2023.

The ECB lifted its main refinancing rate to 2.40% and its deposit facility rate to 2.25%, citing inflation pressures following an Iran conflict-driven energy shock that pushed eurozone inflation to 3.2%. The surprise move comes as the eurozone economy shows signs of weakness, with GDP contracting 0.2% in Q1. Policymakers said the hike is aimed at preventing higher energy prices from becoming embedded in broader inflation. While this may draw criticism from some given the current growth context, the Bank actually has little choice. Unlike the Fed’s dual mandate of inflation and employment, the ECB has a single mandate: price stability. Note a big jump in the ECB's 26/27 inflation forecasts, offset by a drop in GDP forecasts HICP 2026: 3.0%, from 2.6% in March HICP 2027: 2.3%, from 2.0% HICP 2028: 2.1%, from 2.0% GDP 2026: 0.8%, from 0.9% GDP 2027: 1.2%, from 1.3% GDP 2028: 1.5%, from 1.4%

In case you haven't noticed, there is just a tad excess liquidity out there...

SOFR – FF is the spread between two key US short-term rates: 1/ SOFR (Secured Overnight Financing Rate): the rate at which financial institutions borrow cash overnight, collateralized by US Treasuries (i.e. in the repo market). 2/ FF (Federal Funds rate, usually the effective fed funds rate, EFFR): the rate at which banks lend reserves to each other unsecured overnight. So the spread is secured rate minus unsecured rate. Under textbook conditions, secured borrowing is cheaper than unsecured borrowing — you're posting Treasuries as collateral, so the lender takes less risk and accepts a lower rate. That makes SOFR – FF slightly negative (typically a few basis points below zero) in calm markets. This is the "normal" state. SOFR materially below FF — usually means abundant reserves and ample cash chasing limited collateral. Cash holders accept low secured rates because they have nowhere else to put it. This is typically a sign of: - The Fed's RRP (reverse repo facility) being heavily used - QE having left the system flush - or scarcity of high-quality collateral (Treasury bills, in particular). Source: zerohedge

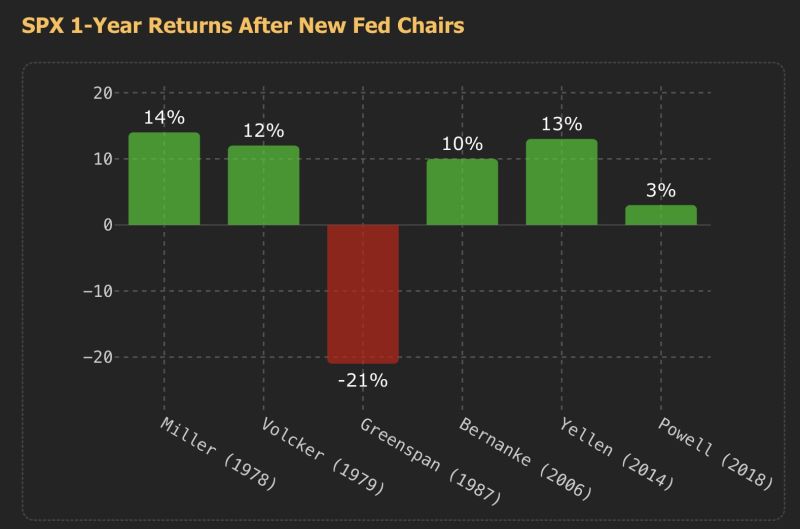

History has been kind to Fed Chairs in their first year. Besides Greenspan, who got handed Black Monday...

Source: TrendSpider