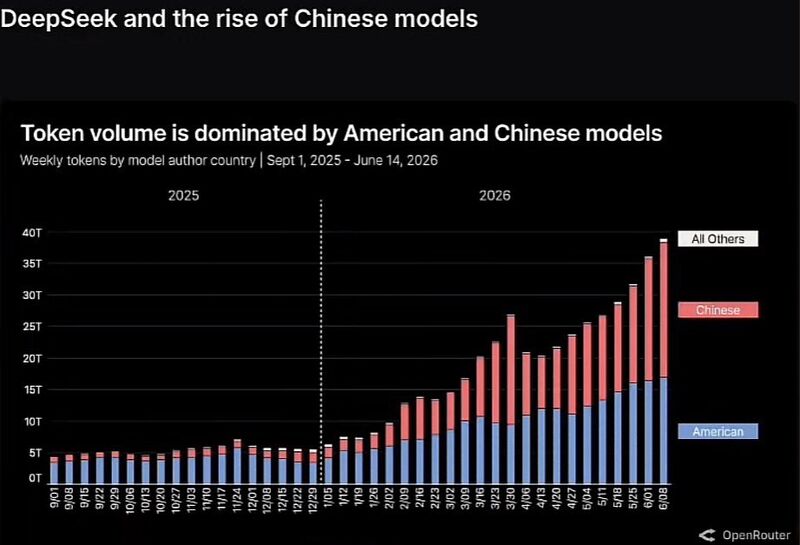

In 2025 American AI dominated with 90% market share.

Today Deep Seek and other AI open source Chinese AI has overtaken the US and now control about 52% of the market. Why? Because Chinese AI is much cheaper. Source: QE Infinity

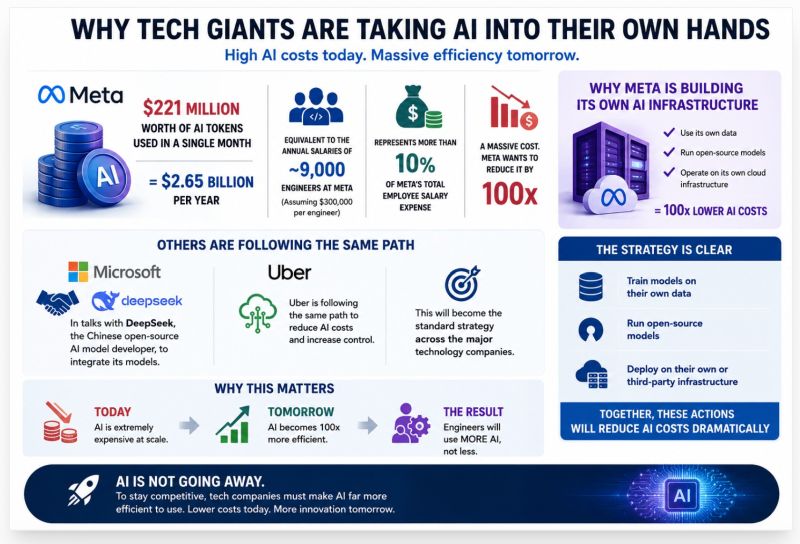

AI ECONOMICS: The bill for “tokenmaxxing” just came due.

Meta’s employees ran up a staggering internal AI bill in a single month. The number is reshaping how Big Tech thinks about the cost of intelligence.

🚨 BREAKING: OpenAI is reportedly discussing giving the U.S. government a 5% equity stake.

The proposal, reportedly floated by Sam Altman, would see leading AI companies allocate a small ownership stake to the public through a vehicle similar to Alaska's Permanent Fund. The idea is simple: if AI is set to create trillions of dollars in value, the public should directly share in the upside. The move could also help ease growing political pressure as Washington scrutinizes AI over jobs, cybersecurity, data centers, and national security. OpenAI and Anthropic have already seen their latest AI models delayed by regulatory review. The proposal would ideally extend beyond OpenAI to companies such as Anthropic, Google, and Meta, although it remains unclear whether they would participate. The discussions are still at an early, conceptual stage and would likely require congressional approval. If implemented, it would mark one of the most significant shifts in the relationship between government and private technology companies, potentially creating a new model where the wealth generated by AI is shared not only with investors, but with the public itself. Source: FT

In case you missed it... 🚨 AI stock euphoria just hit a wall in Asia.

More than $730 billion in market value has been erased across Asian equity markets today as AI and semiconductor stocks came under heavy selling pressure. 🇰🇷 South Korea's KOSPI: -7.89% ($324B wiped out) 🇯🇵 Japan's Nikkei: -2.47% ($214B wiped out) 🇨🇳 China's Shanghai Composite: -2.1% ($191B wiped out) The selloff follows two major warnings over the weekend. The IMF cautioned that AI-related equity valuations have become increasingly speculative and detached from fundamentals. Meanwhile, Wealspring Asset, whose founder famously called the 2007 market peak, warned that a massive global AI bubble has formed, adding that its "collapse point may not be far away." After months of relentless optimism, markets are suddenly being forced to price in the possibility that AI expectations have run too far, too fast. Source: Bull Theory

The META effect

Meta Platforms (NASDAQ:META) climbed more than 10% on Wednesday after a report said the social media company is developing a cloud computing business that would monetize surplus artificial intelligence computing capacity. Meta's plan to monetize excess AI compute may have exposed the first real crack in the AI CapEx narrative. If hyperscalers can generate revenue from spare capacity, or eventually reduce spending without sacrificing AI capabilities, the market's assumption of persistent compute scarcity comes into question. That would be a negative for the hardware and infrastructure layer, but potentially positive for hyperscalers that can monetize existing assets more efficiently (more here). Chart below shows KOSPI, SOX and META (inverted). Source: TME

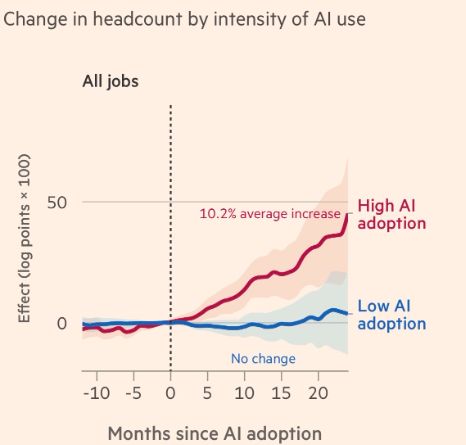

FT had a couple nice ones showing that AI is not causing job losses.. quite the opposite

Source: FT, RBC

BREAKING: The US government has lifted export restrictions on Anthropic's Fable 5 and Mythos 5 AI models.

The restrictions, imposed on June 12 over national security concerns, have now been fully removed after Anthropic agreed to strengthen safeguards and coordinate with the US government on AI security. Anthropic said it expects to restore user access starting Wednesday. Source: Bull Theory

BREAKING: OpenAI advisers are pushing Sam Altman to delay its IPO until next year, per New York Times

Advisers have reportedly cautioned that OpenAI could suffer from a lack of enthusiasm from retail investors. Source: Trend Spider, NYT