There are 2 markets currently 1) The AI stocks; 2) The sources of funds to buy the AI stocks

This scatterplot chart below shows that earnings do matter for AI-themed stocks, but for the rest of the Technology universe, earnings really don't matter YTD. Source: Konstantin Fominykh

While oil's trajectory dominated most of the headlines, a rough weekend for Dario Amodei left Anthropic's Tokenized Stock down notably on the day...

Source: zerohedge

Who owns Anthropic

Stocks World @anandchokshi19

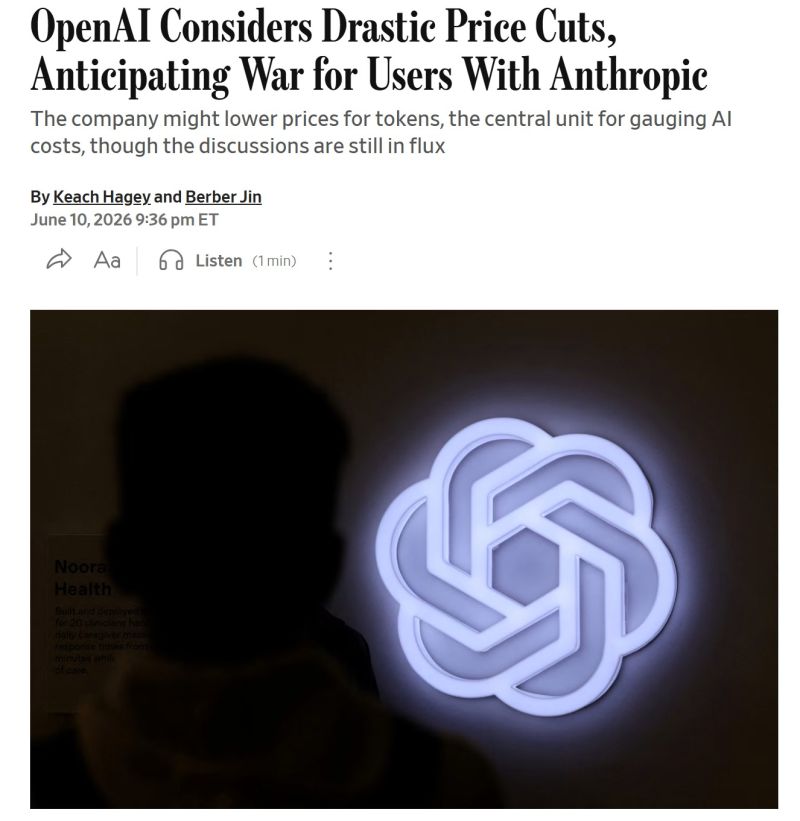

OpenAI is reportedly considering drastic price cuts on its token costs to compete with Anthropic for users

Source: WSJ

S&P 500 ex AI vs. S&P 500 5-day change

That is the biggest spread since AI was birthed... Source: zerohedge, Bloomberg

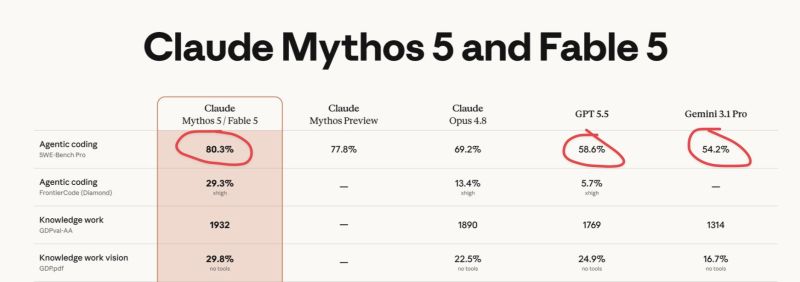

This chart is comparing how different AI models perform on a set of benchmark tests — mainly around coding, reasoning, and knowledge tasks.

The key takeaway: Claude Mythos 5 / Fable 5 is claiming better performance than GPT-5.5 and Gemini 3.1 Pro on these specific benchmarks. Example: SWE-Bench Pro (agentic coding): Claude: 80.3% GPT-5.5: 58.6% Gemini 3.1 Pro: 54.2% What does that actually mean? “Agentic coding” This measures how well an AI can: understand a software engineering task, navigate codebases, edit files, debug issues, and complete coding workflows autonomously. So higher % = the model solved more real-world coding tasks correctly.

Apollo and Blackstone have finalised a $35bn private credit deal that will help finance Anthropic’s growth plans, as banks and investment groups across Wall Street pour capital into the AI boom.

The two private investment groups led the financing, one of the largest private credit deals completed, which will fund Anthropic’s purchase of Alphabet-developed chips. It underscores the massive appetite investors have for AI and the deep pockets they are willing to dig into to finance the data centre infrastructure and computing power needed by companies including Anthropic, OpenAI and Meta. Yet the deal, dubbed project “Big Sky”, comes amid concerns that the AI frenzy has overheated the broader market. Shares in chipmakers rebounded on Monday after tumbling last week, led by Broadcom’s fall in market value. It adds to a deluge of chip-backed loans that sparked debate over how quickly graphics processing units would depreciate as AI technology evolves. The transaction wrapped up days after Alphabet completed one of the largest equity offerings in history, as it looks to raise $85bn to fund Google’s AI build-out, and as SpaceX prepares for a flotation that could raise a record $86bn. Anthropic is readying its initial public offering, following its blockbuster $65bn private financing round. Source: FT

OpenAI just pulled the trigger on what could become the biggest IPO in tech history.

The ChatGPT maker confidentially filed to go public. Potential valuation? 👉 Over $1 TRILLION. And the timing is wild. Within days: • SpaceX is preparing a massive IPO at a $1.78T valuation • Anthropic has already filed • Wall Street’s AI race just went fully public This isn’t just another tech listing. It’s the moment AI officially becomes the center of global capital markets. But here’s the fascinating part: OpenAI is still losing enormous amounts of money. Despite: • 900M+ ChatGPT users • Explosive revenue growth • Record-breaking fundraising • Massive investor hype The company continues burning billions on: • AI research • Data centers • Compute infrastructure • Talent wars And investors still can’t get enough. That tells you everything about where markets believe the future is heading. OpenAI says it “hasn’t decided on timing yet.” Translation: They want optionality. Stay private long enough to move fast… But be ready to tap public markets the second conditions are perfect. Meanwhile: • Elon Musk’s lawsuit against OpenAI was thrown out last month • Discussions with the US government are reportedly happening • Employees may soon get liquidity through a secondary sale This is no longer just a startup story. Source: FT