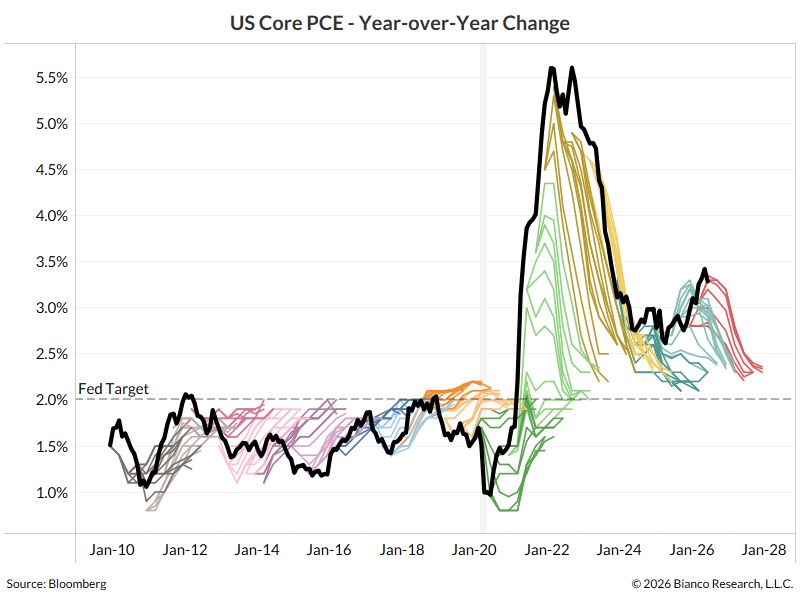

Wall Street has predicted inflation would return to 2% for 64 straight months. It has been wrong every time.

Yesterday, New York Fed President John Williams said he expects inflation to ease in the second half of this year and decline further next year. That is also the consensus view on Wall Street. The chart tells a different story. For the past 64 months, Bloomberg's survey of around 70 economists has consistently projected core PCE inflation would return to roughly 2% within the next six quarters. It never happened. Before the pandemic, forecasts generally expected inflation to rise back toward target. Since COVID, the opposite has been true: economists have repeatedly predicted inflation would fall to 2%, yet core PCE has remained persistently above target and has even trended higher over the past 18 months. The key question is whether this time is genuinely different. If the same forecast has missed reality for more than five years, investors should ask what has fundamentally changed that would finally make it accurate. Source: Jim Bianco