2 Jul 2026

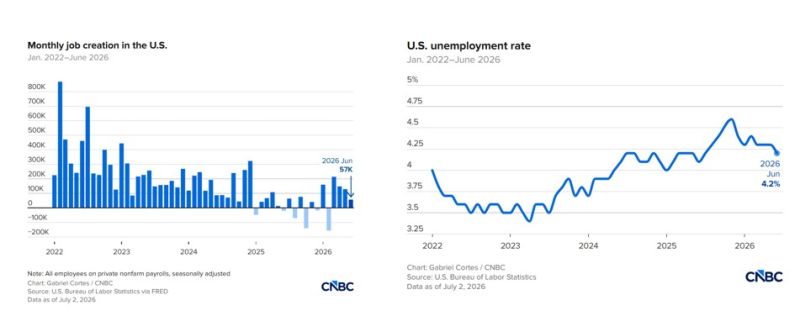

June payrolls rose by only 57,000, well below expectations of 115,000 and down sharply from May's revised 129,000.

At first glance, the unemployment rate improved to 4.2%.

But the headline masks growing weakness.

The labor force participation rate fell to 61.5%, its lowest level since March 2021, while household employment plunged by 507,000 people in a single month.

Wage growth remained resilient, with average hourly earnings rising 0.3% month-over-month and 3.5% year-over-year, suggesting inflationary pressures have not fully disappeared.

Under the surface, the picture is mixed:

📈 Professional & business services: +36K

📈 Social assistance: +25K

📈 Healthcare: +22K

📈 Government: +8K

But leisure & hospitality LOST 61,000 jobs 🚨, despite expectations that the World Cup would boost seasonal hiring.

The labor market is no longer collapsing.

But it is clearly cooling.

For the Fed, this report strengthens the case that growth is slowing, even if wage pressures remain sticky.

Source: CNBC