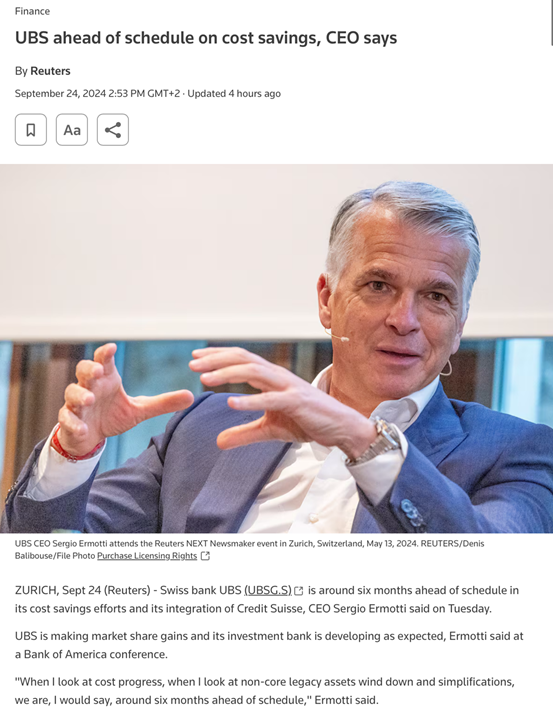

UBS is ahead of schedule on cost savings according to CEO S. Ermotti

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Related Articles

in the current context of weak inflation, upward pressures on the Swiss franc and worrying dynamics in neighboring European countries. The 50bp rate cut is half-a-surprise for financial markets, that were not fully convinced of the possibility of such large movement and were rather pricing a 25bp rate cut. swiss franc initially weakened 0.5% vs the Euro. But it is already back to 0.93. OUR TAKE (based on our Chief Economist Adrien Pichoud views) 👉 Swiss CPI inflation has slipped below 1% in the 4th quarter of 2024 (+0.7% in November) and it is expected to slow further in 2025. The SNB expects inflation to hover just above zero (+0.2%/+0.3%) for most of next year before picking up slightly as 2026 draws near. By averaging +0.3% in 2025, the inflation rate would be at the very bottom of the 0-to-2% range that the SNB targets. 👉 As the Swiss economy faces headwinds from the strength of the Swiss franc and the weakness of economic activity in Germany and most other European economies, monetary policy has no reason to be restrictive and had to be adjusted. After today’s rate cut, the monetary policy stance is about neutral (with a real short-term rate close to 0%). 👉 Looking ahead, more rate cuts are to be expected in 2025. We expect the CHF short-term rate to be lowered to 0.0% by June next year, with 25bp rate cuts at the March and June meetings. 👉 Will Switzerland move back to NEGATIVE RATES? This is not our scenario at this stage, even if it wasn’t ruled out by Mr Schlegel recently. Potential undue upward pressures on the CHF will then likely be addressed with interventions on the FX market and a possible expansion of the SNB’s balance sheet size. It would require a significant deterioration in global growth and inflation dynamics next year for the SNB to be pushed back into negative interest rate policies. Source chart: Bloomberg

The Bank of England will hide the identities of any pension funds, insurers or hedge funds bailed out under a new financial stability tool to prevent crisis contagion... Source: Radar @RadarHits - Bloomberg

[Dennis Porter] - Bitcoin Archive