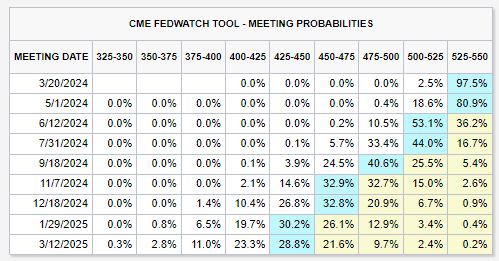

Interest rate cut expectations continue to scale back: Markets now see a ~38% chance of 4 interest rate cuts in 2024

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Related Articles

The World Gold Council reported net central bank gold purchases of 41 tonnes in May, more than double April's 19 tonnes. Poland was the biggest buyer, adding 18 tonnes in May, bringing its 2026 total to 64 tonnes. Its reserves now stand at 614 tonnes. China added 10 tonnes, its biggest monthly purchase since December 2024 and its 20th straight month of buying. Total Chinese reserves now sit at 2,331 tonnes. Turkey was the only major seller, offloading 3 tonnes in May, extending its 2026 net sales to 81 tonnes as it draws on reserves to defend the lira. The 2026 Central Bank Gold Reserves Survey shows 89% of central banks expect global gold reserves to increase over the next 12 months. A record 45% plan to increase their own holdings. Gold gained +2% last week after four straight weekly declines but remains -25.4% below its peak. Source: Bull Theory

USD/JPY surged to a fresh 40-year high of 162.84 before plunging to 160.90 within hours. A 1.2% intraday reversal in one of the world's most liquid currency pairs is highly unusual. It mirrors what happened in April and May, when Japanese authorities spent roughly $72–73 billion selling U.S. dollars and buying yen to slow the currency's collapse. The pattern looks strikingly familiar: • New multi-decade high. • Sudden, aggressive reversal. • Speculation of official intervention. There has been no official confirmation yet. But the speed and magnitude of the move are exactly what markets expect when Tokyo steps in. Even after the sharp rebound, the yen remains close to its weakest level in four decades, keeping pressure on policymakers as imported inflation rises and global markets watch for their next move. Source: Bull Theory

Unemployment fell to 4.2% for the wrong reason: participation cratered to 61.5% from 61.8%. Source: Holger Zschaepitz Bloomberg