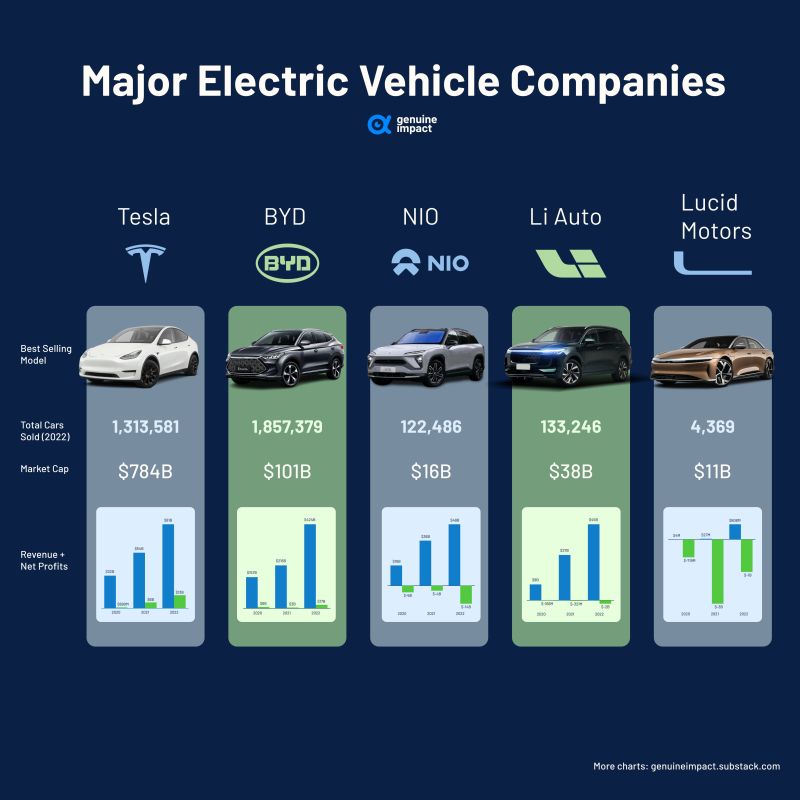

Tesla holds the undisputed leadership position among #electriccar companies based on market capitalization

Tesla holds the undisputed leadership position among electric car companies based on market capitalization. However, this year, BYD has surpassed Tesla to become the world's top-selling EV brand. Source: Genuine Impact

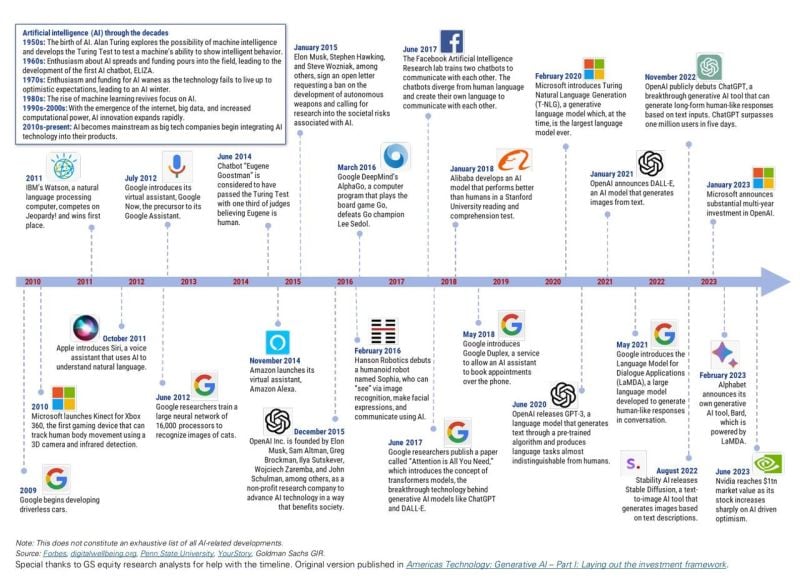

Artificial Intelligence through the decades - how did we get there?

Source: Forbes, Goldman Sachs

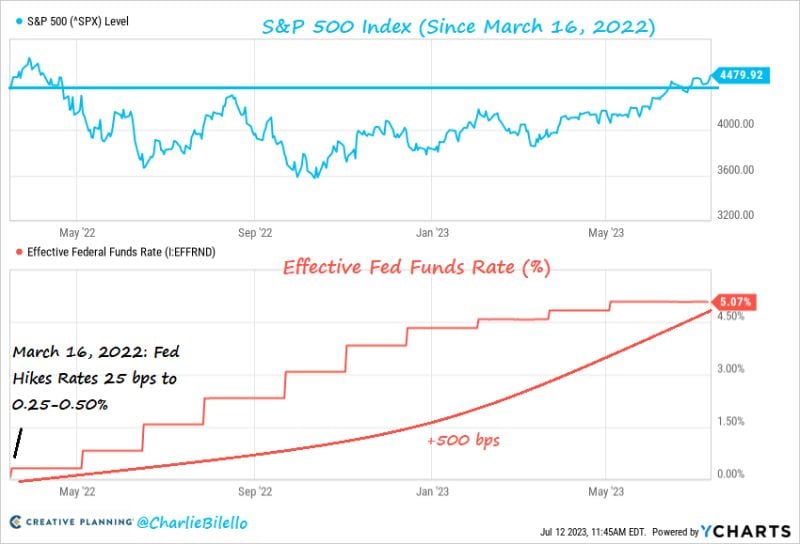

The S&P 500 is now 3% higher than where it was when the Fed started hiking rates in March 2022. $SPX

Source: Charlie Bilello

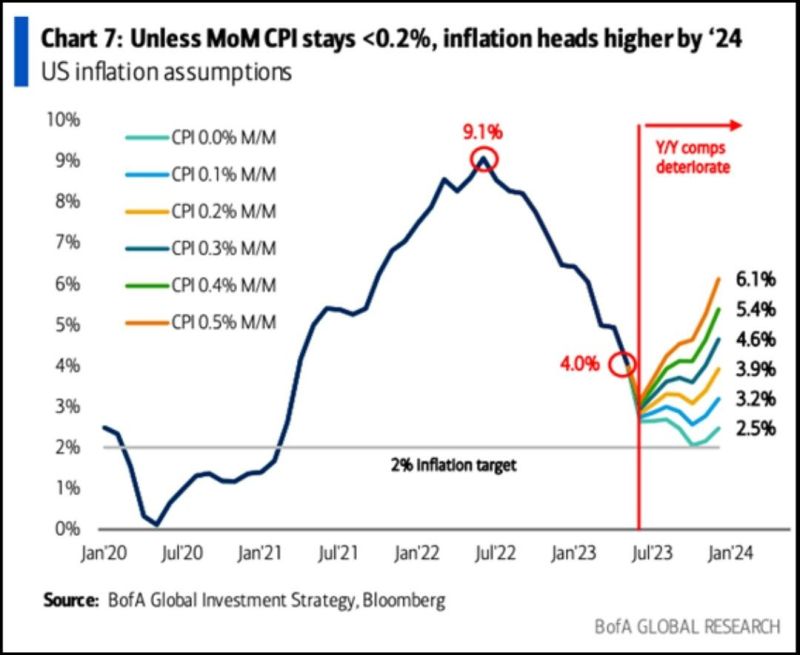

The easy part is over for disinflation as disinflationary base effects are behind us

The easy part is over for disinflation as disinflationary base effects are behind us. The MoM CPI now needs to be lower than 0.2% for #inflation to continue moving lower. Source: BofA

Ethereum activity on the rise as on-chain metrics print fresh highs

The total value of staked ether (ETH) continues apace, reflecting positive signs of growth and stability for the world’s second-largest digital asset. Following Ethereum’s critical PoS upgrade in April, the amount of ETH that has been deposited to the ETH 2.0 contract now stands above 25.6 million. Yield on staked ether is currently around 4.5%, paid in ETH. Participants continue to bank on the value of the Ethereum network, with those holding the underlying becoming more hesitant to relinquish their assets as they anticipate future demand.

Source: Blockworks

Phillips 66 Closed Above its Bollinger Band, Still in Downtrend

Phillips 66 closed above its upper Bollinger band, indicating shares may be overbought. In the past 12 months, the stock has crossed above this level 10 times and fell an average of 5.6% in the next 20 days. Can it break?

Source: Bloomberg

%20%20Dai%202023-07-13%2013-03-46.jpg)

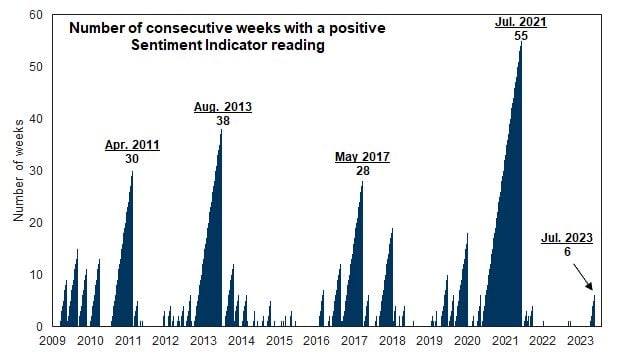

Over-optimistic sentiment can stay extended / “stretched” for long periods of time.

Over-optimistic sentiment can stay extended / “stretched” for long periods of time. Source: Goldman Sachs

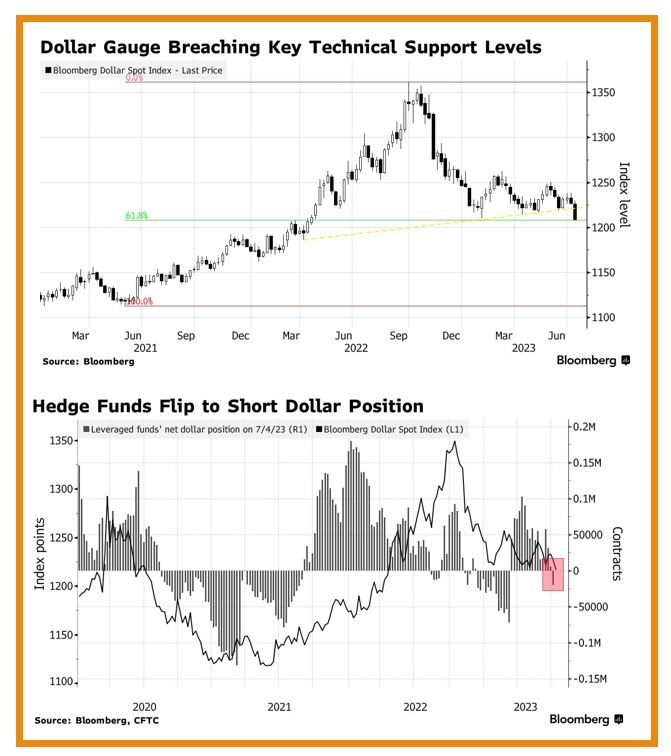

The Bloomberg Dollar Spot Index slumped to a 15-month low, with the gauge now down over 11% from a September peak

The Bloomberg Dollar Spot Index slumped to a 15-month low, with the gauge now down over 11% from a September peak. hedgefunds had been bracing for weakness, as they turned net sellers of the dollar for the first time since March, according to data from the Commodity Futures Trading Commission aggregated by Bloomberg. The dollar’s resilience has confounded bears who had warned that the currency was headed for a multi-year decline following a surge in 2022. But there’s a growing conviction that they may finally be proven right as easing inflation backs the case for the us central bank to wrap up its rate-hike campaign in the coming months. Source: Bloomberg