Are silver prices about to CRASH next week?

Next week's commodity index rebalancing could force massive selling of silver futures, pushing prices lower regardless of fundamentals. Silver faces the largest selling pressure among major commodities, with rebalancing demand at -25% of open interest. Index funds will be forced to dump silver futures just to rebalance. Why? Silver's recent surge was driven by speculation, not fundamentals, fueled by ETFs, retail traders, and thin liquidity. Source: DB, Global Markets Investor

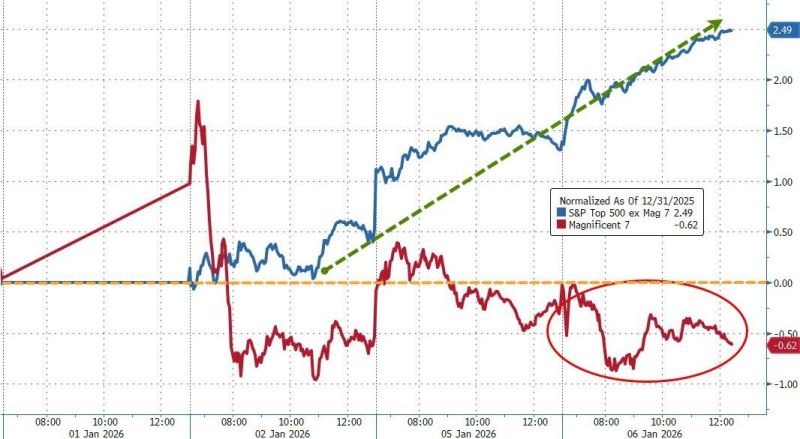

From Mag7 to Lag7...

Mag7 stocks have significantly lagged the rest of the market in 2026 so far... The S&P 493 is up 2.5% YTD, Mag7 -0.6%... Source: www.zerohedge.com, Bloomberg

Some inspiring thoughts by Ibrahim Majed on X And why this is not about Maduro. Not even about Venezuela. 🌎

We are witnessing the rollout of a global energy stranglehold. If you think the recent moves in South America are local politics, you’re missing the forest for the trees. This is a masterclass in Geopolitical Chess, and the target is much bigger. Here is why Venezuela is the "Patient Zero" for a new era of American dominance: 🔴 1. Cutting China’s Lifelines By taking control of Venezuela’s oil and aligning Nigeria under Western oversight, Washington is effectively pulling the plug on China’s access to cheap, reliable energy. Control the supply + control the transit = control the rival. 🚢 2. The Chokepoint Strategy Look at the map. From the Bab al-Mandab (Somaliland/Yemen) to the Strait of Hormuz, the U.S. is positioning itself to insulate its own economy while leaving China’s economy vulnerable to any disruption. 🛡️ 3. Neutralizing the Iran Factor Securing the world’s largest oil reserves in Venezuela provides a massive "buffer." If the Persian Gulf goes dark in a conflict with Iran, the U.S. won't flinch. Venezuela becomes the ultimate insurance policy, making military escalation in the Middle East "affordable." 💵 4. Defending the Petrodollar This is about ensuring the U.S. Dollar remains the undisputed king of energy markets. By restructuring sovereign states to align with U.S. interests, Washington is reinforcing the financial plumbing of the global economy. The Bottom Line: Venezuela is a strategic precedent. If this succeeds, it’s a blueprint for reasserting dominance over trade routes and energy flows for the next 50 years. But there’s a massive "IF." If the U.S. gets bogged down in a prolonged crisis in Caracas, it drains the very capital needed to project power in the Middle East and Asia. Is this a brilliant strategic realignment, or a high-stakes gamble that could overextend American power?

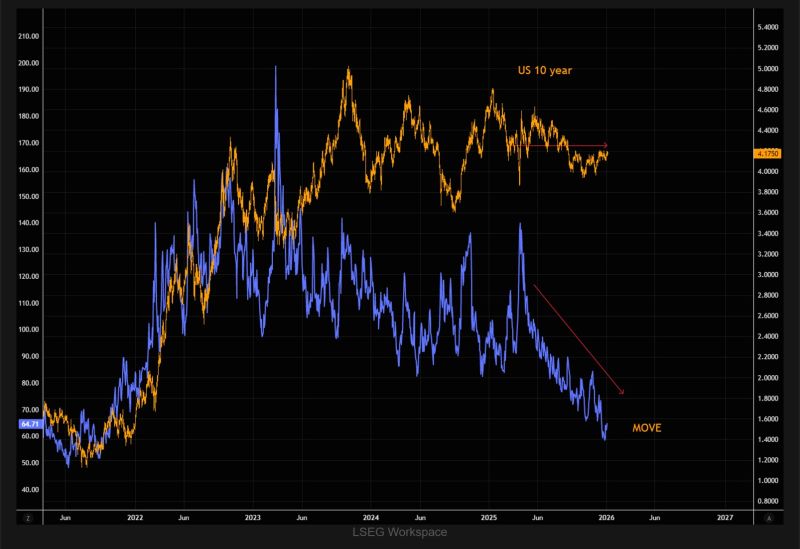

The great vol reset

We’ve seen a massive reset in bond volatility since the Liberation Day chaos. US Treasuries yields have gone nowhere, but at these levels owning some bond volatility offers limited downside with asymmetric upside. Source: The Market Ear, LSEG

We aren't just talking about trade embargoes or "backdoor deals" anymore. We are talking about a direct naval showdown on the high seas. 🌊⚓️

Here is the situation: The U.S. is moving to seize the Marinera, a Russian-flagged tanker carrying sanctioned Venezuelan oil. Russia’s response? They deployed a submarine to escort it. 🇷🇺🇻🇪🇺🇸 The Breakdown: -> The Move: The U.S. is enforcing sanctions with physical force. -> The Counter: Moscow is signaling they will use military hardware to protect their assets. ->The Global Ripple: China is watching closely. 🇨🇳 Why this matters: This isn't just about oil prices. It’s about the shift from Economic Diplomacy to Kinetic Confrontation. If the U.S. succeeds, American sanctions become the ultimate global law. If Russia blocks them, the era of U.S. naval dominance faces its biggest test in decades. Source: Mario Nawfal on X, Reuters, @sentdefender, WSJ

Financial conditions keep loosening as investors get excited about the potential for both fiscal and monetary stimulus this year.

Yields on junk bonds have fallen to the lowest since 2022, despite bankruptcies starting to creep higher. Source: Bloomberg, Lisa Abramowicz @lisaabramowicz1

In case you missed it... In Germany, inflation slowed more than expected at the end of last year.

Consumer prices rose 1.8% in Dec YoY, below the 2.1% forecast. The slowdown was driven mainly by falling energy prices and a sharp easing in food inflation, which dropped to just 0.8%. Core inflation also declined to 2.4%, although service inflation remains stubbornly high at 3.5%. Source: HolgerZ, Bloomberg

Saudi Arabia has removed all restrictions for foreigners to buy local stocks.

The decision allows non-residents to invest directly in the main market effective Feb. 1.