₹5.5 trillion has now been wiped out from the Indian stock market today.

Top 4 losers: State Bank of India (SBI) down -4.14%, banking sector pricing in a full economic slowdown as India's energy crisis deepens. Titan Company down -6.72%, PM Modi directly asked 1.4 billion Indians to stop buying gold for a year. Titan makes jewellery. ABB India down -8.77%, capital goods and manufacturing collapsing as energy costs make industrial operations unviable. IndiGo down 4.8%, jet fuel costs have exploded and PM Modi just discouraged all foreign travel. India's forex reserves have fallen by $38 billion since the war started as the RBI has been selling dollars to defend the rupee. At the current rate of drawdown, India has roughly 8 months of import cover remaining. The rupee hit an all time low of 95.23 against the dollar today. Every $10 per barrel increase in crude oil prices raises India's annual import bill by approximately $13–$14 billion. Source: Bull Theory

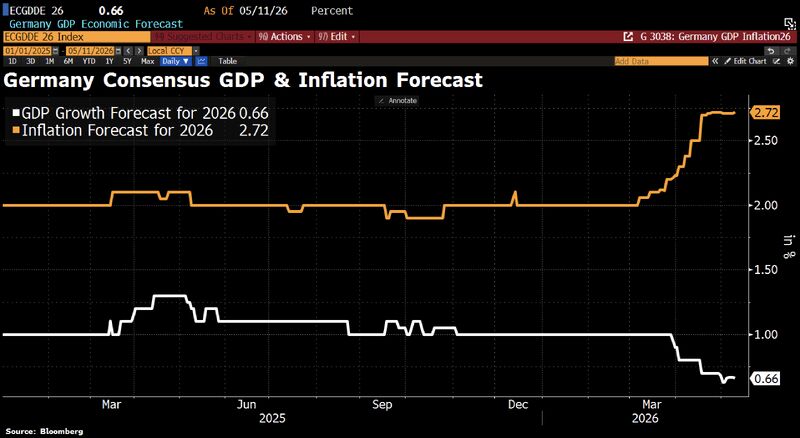

Germany appears to be heading towards stagflation.

Consensus GDP forecasts for 2026 have been revised down from more than 1% to just 0.66%, while inflation forecasts have climbed above 2.7%. Against this backdrop, the ECB is now expected to raise interest rates twice – at least, that is what markets are pricing in. Source: HolgerZ, Bloomberg

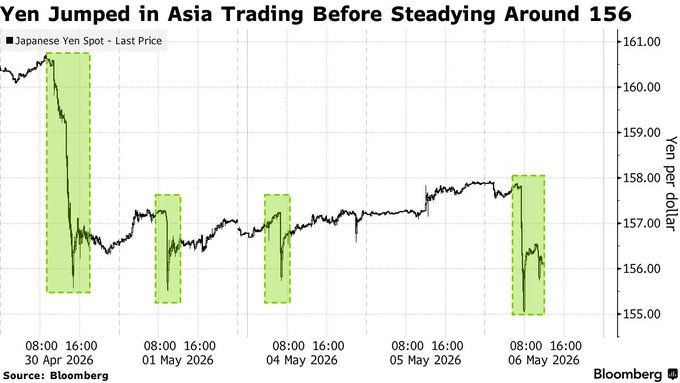

Japan's Ministry of Finance appears to be intervening in currency markets repeatedly:

The Japanese yen surged +1.8% in under 30 minutes during Asian trading on Wednesday, briefly touching 155.04 per US Dollar, the latest in a series of sharp moves consistent with official intervention. This comes after Japan's first intervention since 2024 on April 30, when Bank of Japan account analysis indicated authorities spent ~$34.5 billion to defend the yen. Meanwhile, Goldman Sachs estimates Japan still has enough reserves to intervene ~30 more times at this scale. The 157 level is emerging as the new line in the sand for Japanese authorities, with the Ministry of Finance warning speculators last week that "the timing for taking bold steps is nearing." Japan is desperate to prevent the Yen from weakening past 160 per US Dollar. Source: Bloomberg, Global Markets Investor

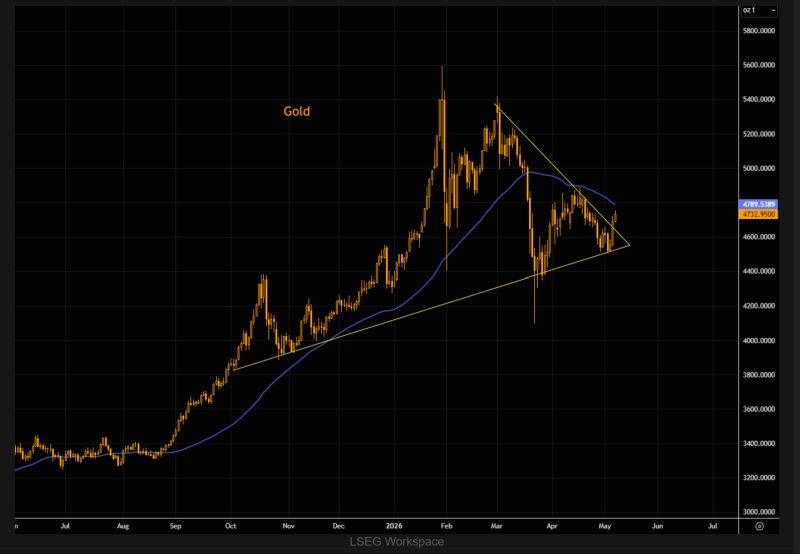

Yesterday, Gold put in its biggest up day in quite some time during yesterday’s session.

The shiny metal broke above the short-term downtrend line and also pushed out of a dynamic wedge-like formation. The key for a more sustained squeeze is a close above the $4800 area, right where the 50-day moving average comes in. More on gold. Source: TME

The bond market’s inflation outlook just collapsed from over 5.3% to 3.0% over the next twelve months.

Source: Hedgeye, Bloomberg

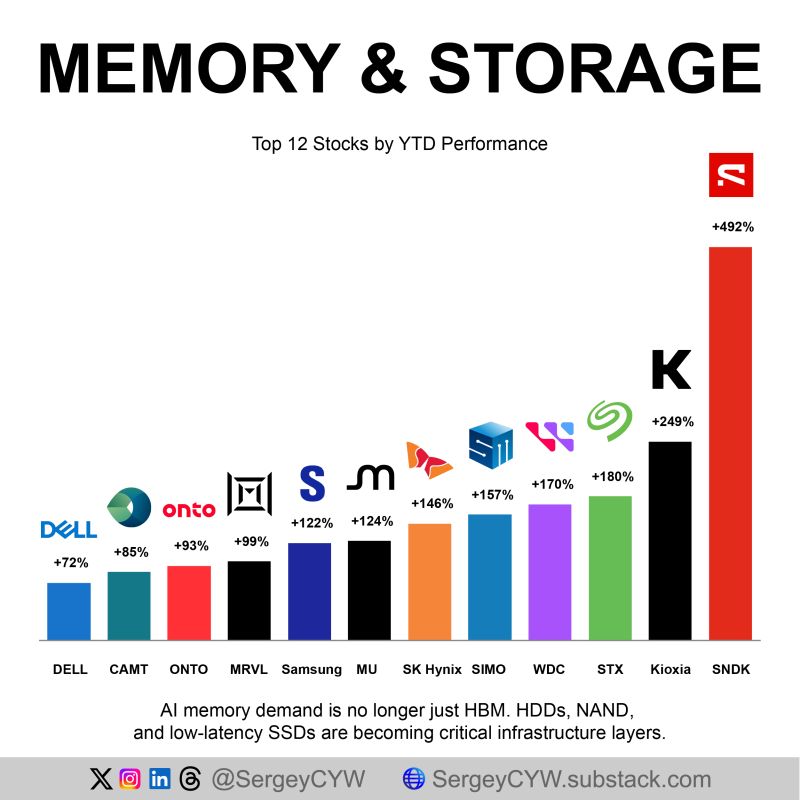

AI Memory Stocks Are Crushing the Market

The bottleneck is spreading across DRAM, NAND, SSD controllers, HDDs, advanced packaging, process control, server racks, and wafer fab equipment. Every layer of the stack is being repriced as AI workloads demand more bandwidth, more capacity, and faster data movement. Source: Sergey

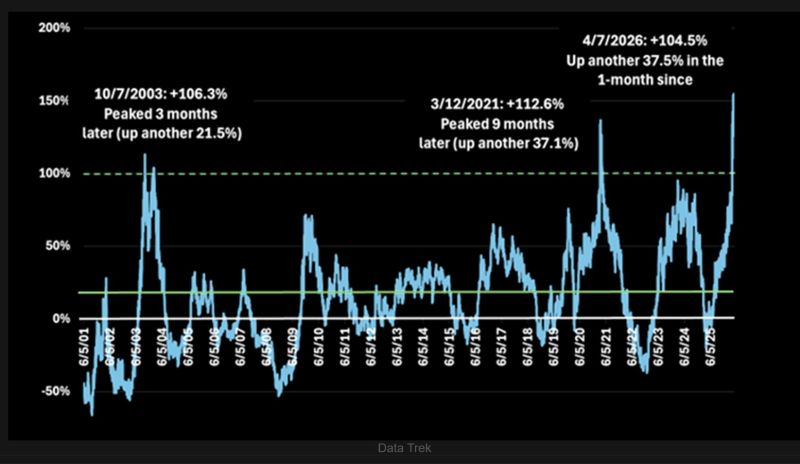

The semiconductors ETF $SMH is up roughly +153% over the past year, the strongest 1-year performance on record going back to 2001 and roughly 4 standard deviations above the long-run average.

As DataTrek notes, staying bullish from here increasingly requires confidence that the semiconductor cycle and AI-driven backlog can remain durable for much longer. Source: The Market Ear

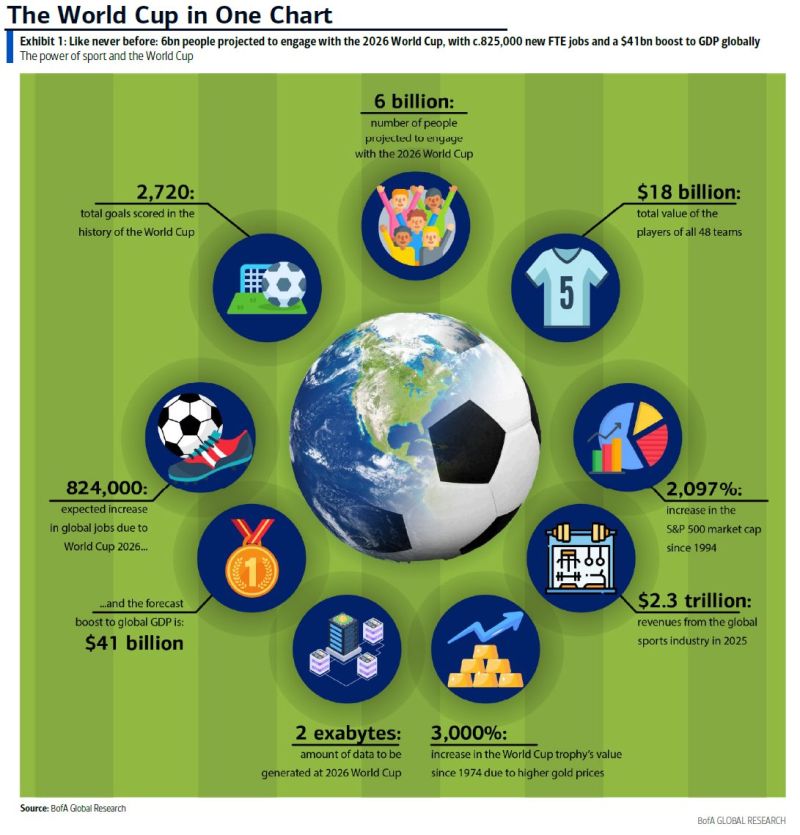

World Cup in one chart

Source: Zerohedge, BofA