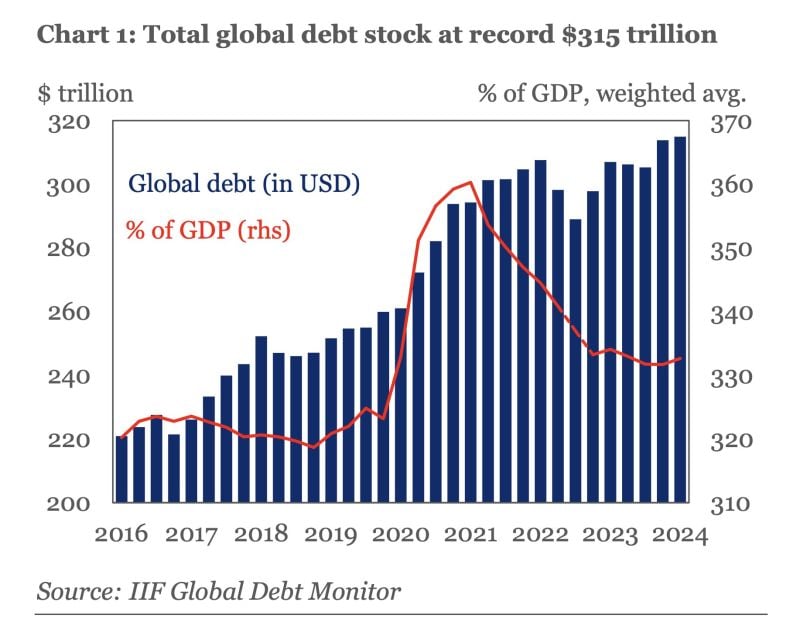

Global debt rose by $1.3tn to a new ATH of $315tn in Q1 2024.

Moreover, after 3 consecutive quarters of decline, global debt-to-GDP resumed its upward trajectory in Q1 2024. Emerging market debt topped $105tn in Q1 2024, w/largest increases coming from China, India, Mexico. Source: HolgerZ, IIF

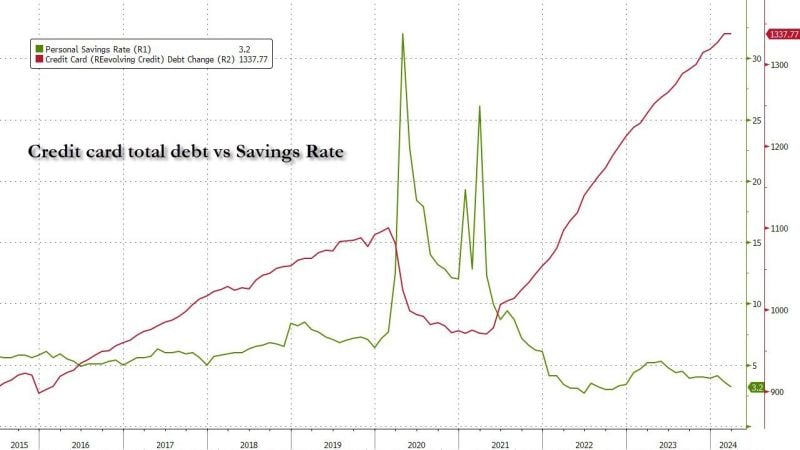

The US consumer (risk) in one chart: credit card debt at record high, personal savings rate record low

Source: www.zerohedge.com

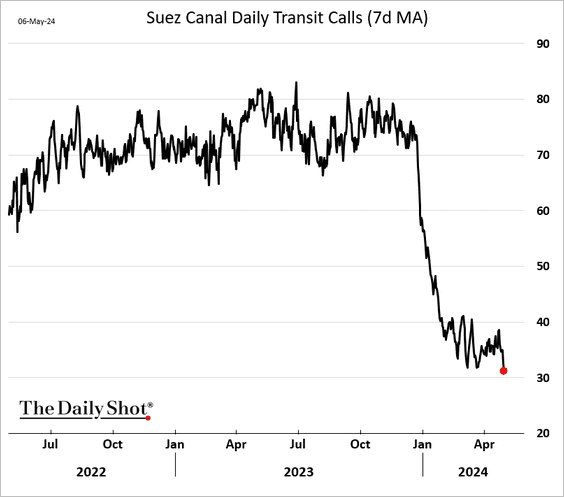

The Suez Canal ship transit volume has deteriorated further.

Source: The Daily Shot

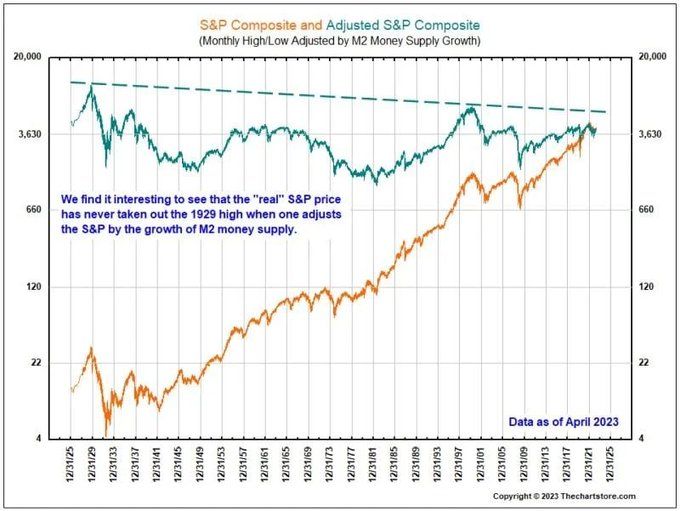

The real price of the S&P500 has never exceeded the 1929 highs...

...If adjusted for M2 money supply growth 💸 Source. Nicolas Cheron

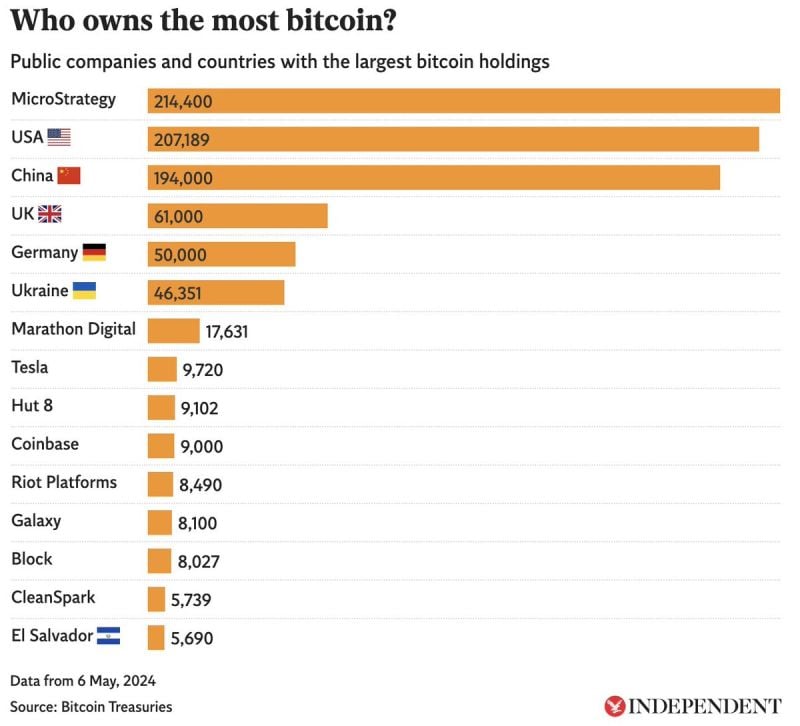

MicroStrategy now owns more Bitcoin than any country in the world.

Source: Bitcoin Magazine

ISM US manufacturing and services employment has simultaneously contracted for 3 consecutive months.

Over the last 20 years, this has happened ONLY twice, during the 2020 pandemic and 2008 Financial Crisis. More than 800 companies from manufacturing and services sectors claim that employment is falling. Meanwhile, according to US jobs data, the US job market has never been stronger. Are we going to see meaningful deterioration in jobs data in the coming months? Source: The Kobeissi Letter

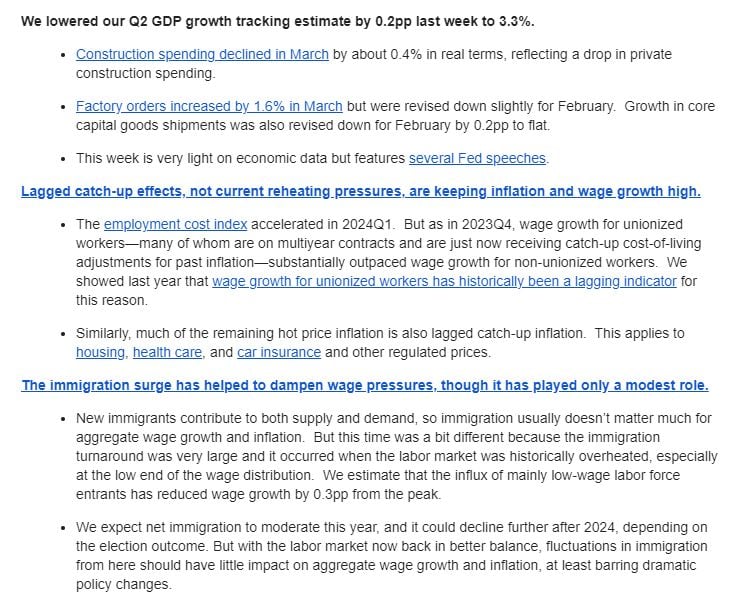

GS: much of the remaining hot price inflation is also lagged catch-up inflation.

This applies to housing, health care, and car insurance and other regulated prices Mike Zaccardi, CFA, CMT

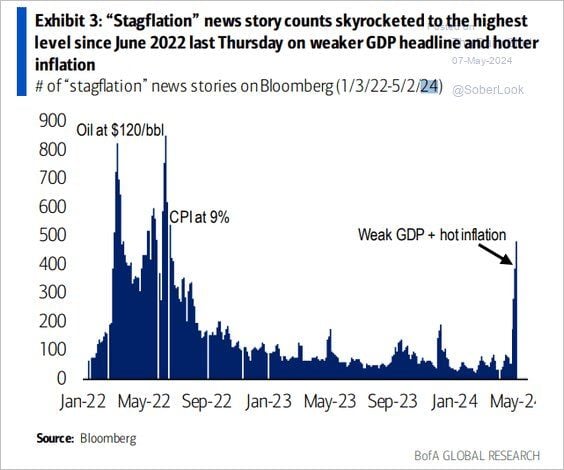

Stagflation fears are back.

Source: BofA Global Research; Mike Zaccardi