CSI 300 is up some 11% from early Feb lows.

The index is well above the 50 day, and touched the 100 day for the first time since last summer. Source: TME

Bloomberg city tracker European major cities

Berlin’s housing slump is over as shortage lures investors. The prospect of higher rents in the German capital is countering the downward pull of financing costs. Berlin rents jumped 20% YoY in Q4, faster than national average of 7.7%. As a side note, Athens' price jump is quite interesting Source: HolgerZ, Bloomberg

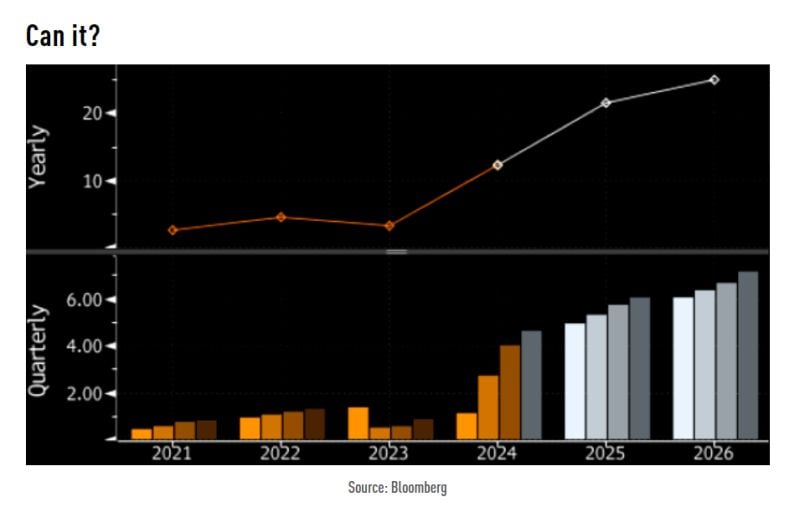

nvidia $NVDA EPS growth projections (grey) aren't modest...

Source: TME, Bloomberg

The Magnificent 7 is becoming the Magnificent 4

Source: Beth Kindig

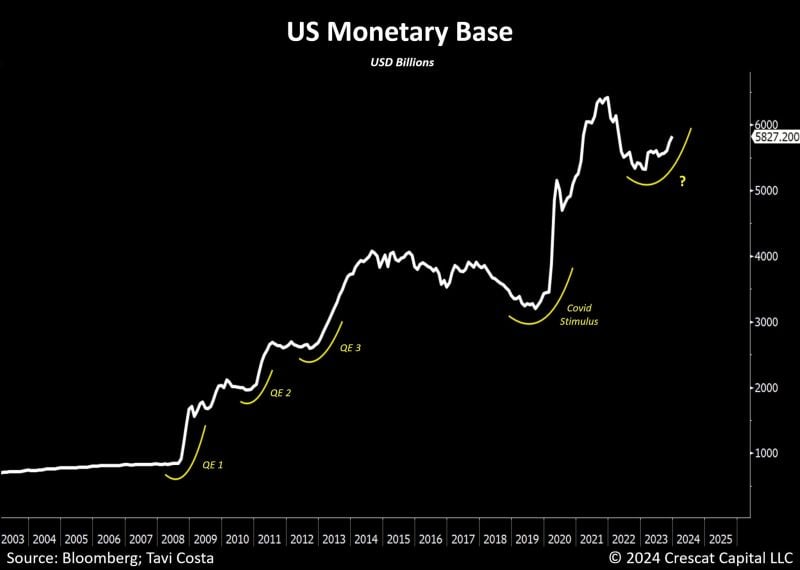

The US monetary base has been rising significantly recently.

In the last 12 months alone, there has been a rise of $420 billion, primarily fueled by bank reserves. While the Fed should not classify this as QE due to mechanical differences, it seems to echo the patterns of previous periods of monetary stimulus following the Global Financial Crisis. The economy (and markets) are addicted to liquidity. Source: Bloomberg, Tavi Costa

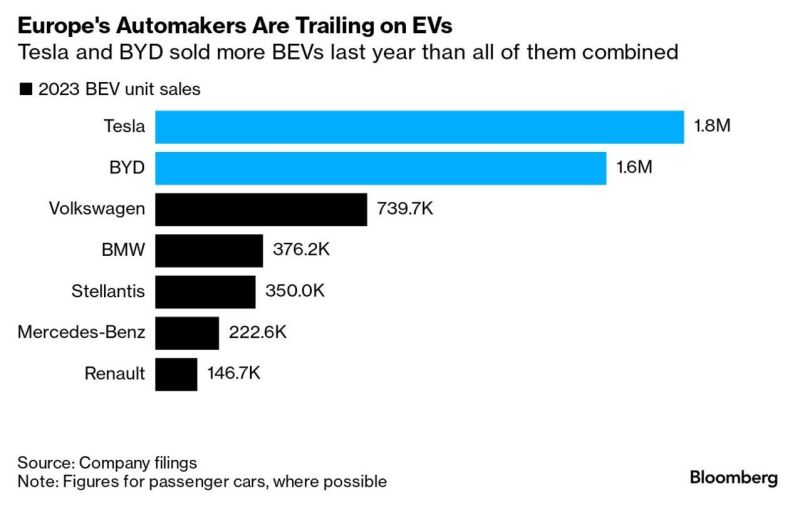

What‘s wrong with Europe in one chart.

These European companies have been in the automotive business for decades. Why are they so painfully slow to adapt to new reality? Source: Michel A.Arouet, Bloomberg

Nvidia options signal nearly $200bn swing after earnings.

Prices for short-term calls and puts imply a 10.6% move in the chipmaker’s shares on Thursday. Source: Bloomberg, HolgerZ

Should you exit equities (or avoid investing into equities) when they hit all-time high?

The answer is 'NO'. Returns have been higher than average, following all-time highs. More importantly, exiting at all-time highs is disastrous for your return! Massive chart by Duncan Lamont / Schroders thru Jeroen Blokland.