30 Jul 2024

As highlighted by Eric Balchunas

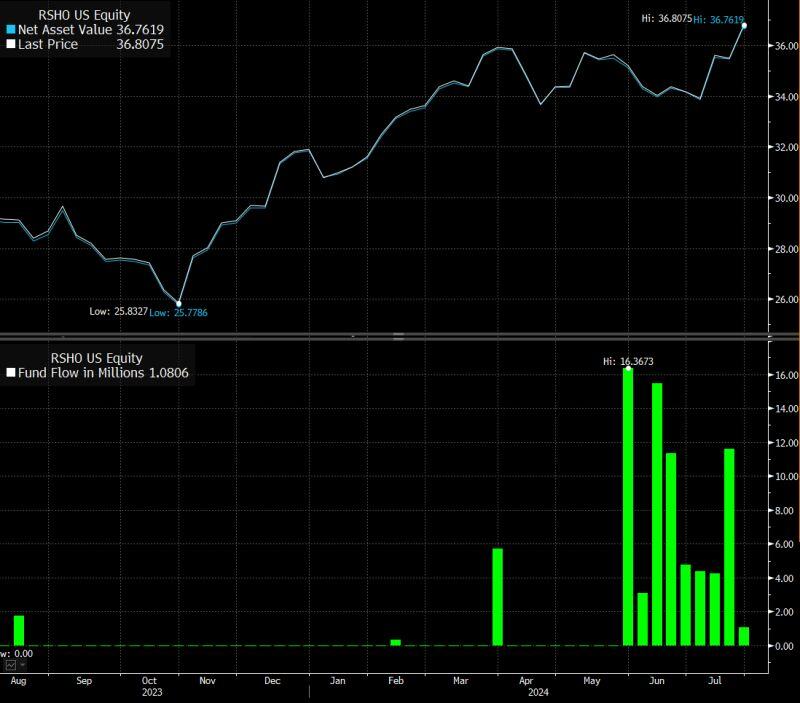

The Reshoring ETF $RSHO is quietly nursing a 9-week flow streak (after being ignored since birth) which boosted its assets under management 7x this year. The American Industrial Renaissance ($AIRR) 3ETF also saw AuM jump by $800m YTD. BlackRock noticed this and launched iShares US Manufacturing ETF $MADE. All these ETFS are exposed to Trump Trade 2.0 but this theme spans beyond politics. Source: Bloomberg, Eric Balchunas

30 Jul 2024

US Presidential elections >>> Are we back to square one?

Source: PredictIt, Bloomberg, www.zerohedge.com

30 Jul 2024

Microsoft and Alphabet are now exactly on par since the launch of ChatGPT at the end of November 2022.

Source: HolgerZ, Bloomberg

30 Jul 2024

The US government just moved $2 billion of seized bitcoin $BTC, two days after Trump's speech 👀

Source: Joe Consorti

30 Jul 2024

The biggest risk is taking NO risk

Source: Seek Wiser

29 Jul 2024

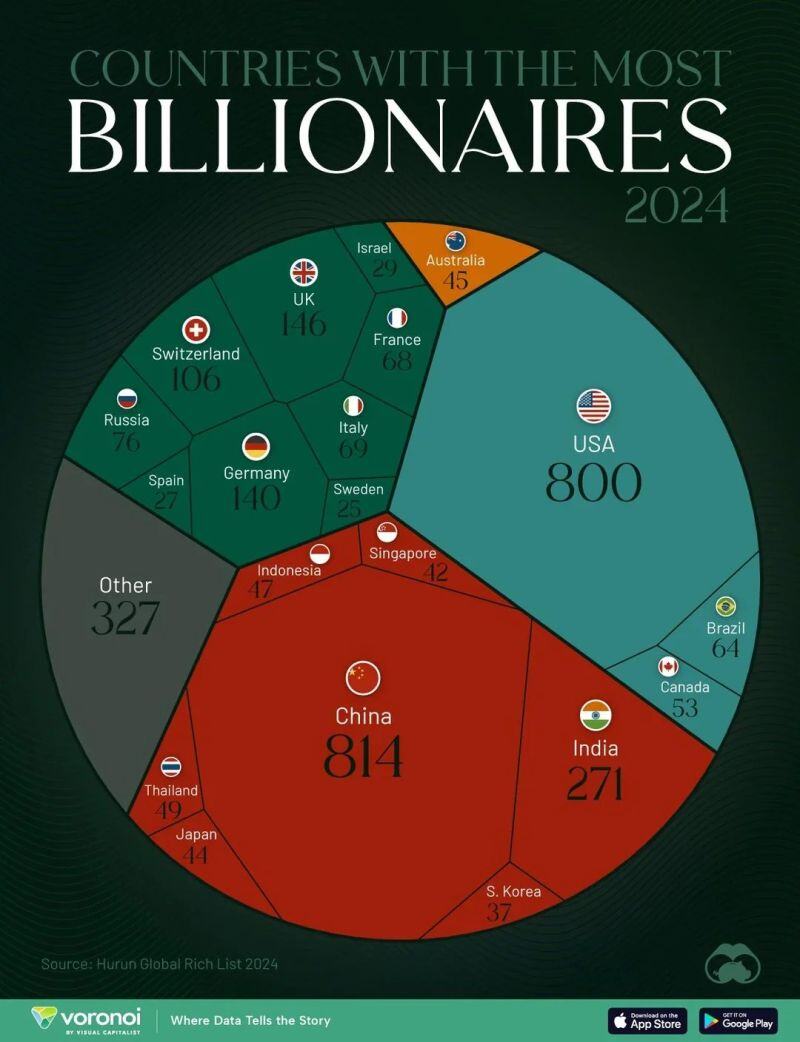

Countries with the most billionaires 📊

Source: Voronoi, Visual Capitalist

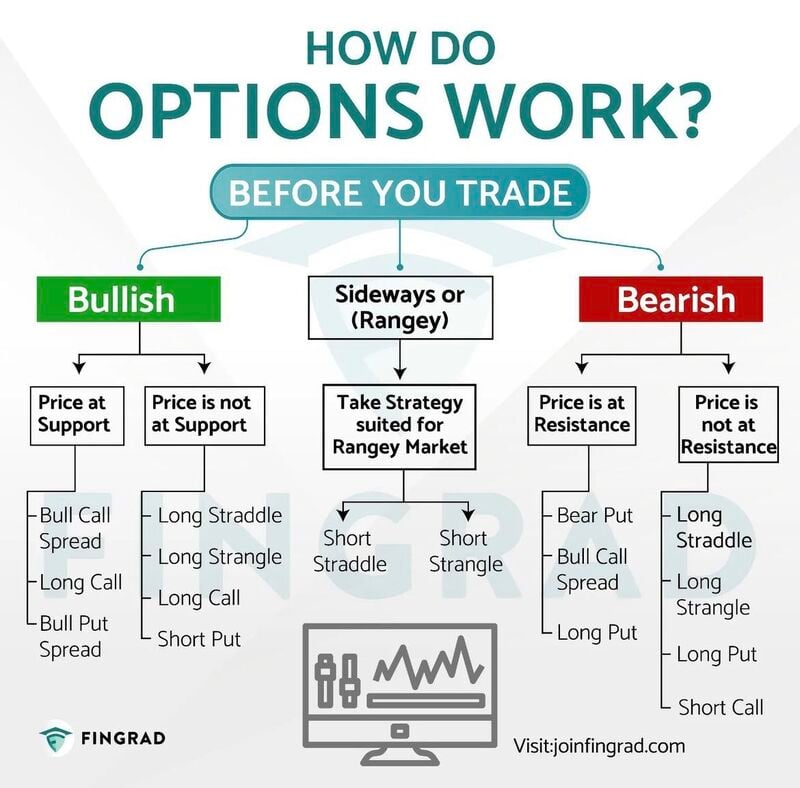

29 Jul 2024

How do options work?

Source: Market insights

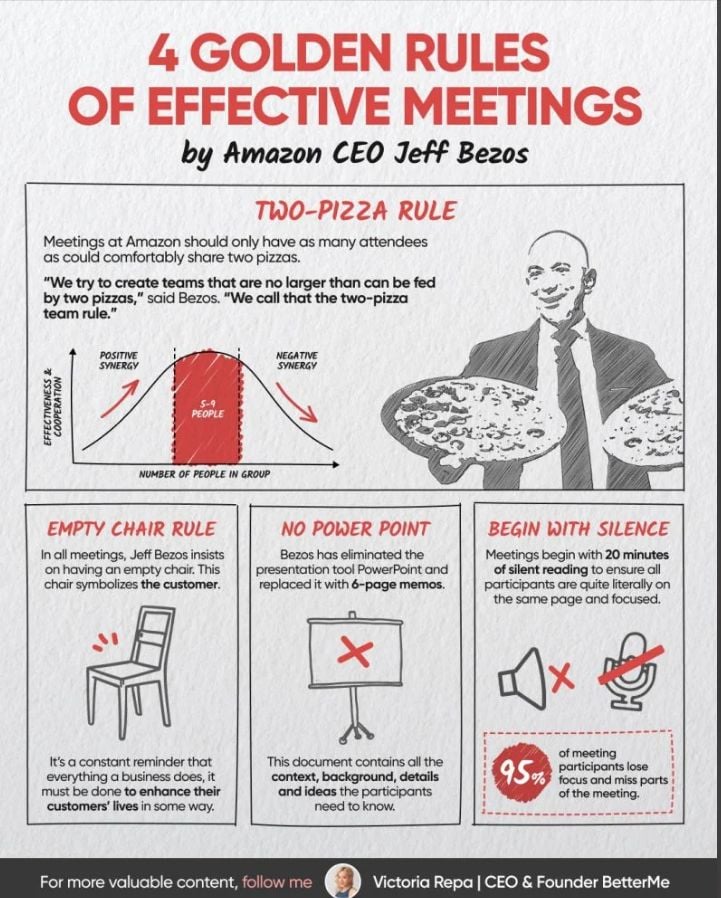

29 Jul 2024

4 Golden rules of effective meetings by Jeff Bezos

Source: Victoria Repa