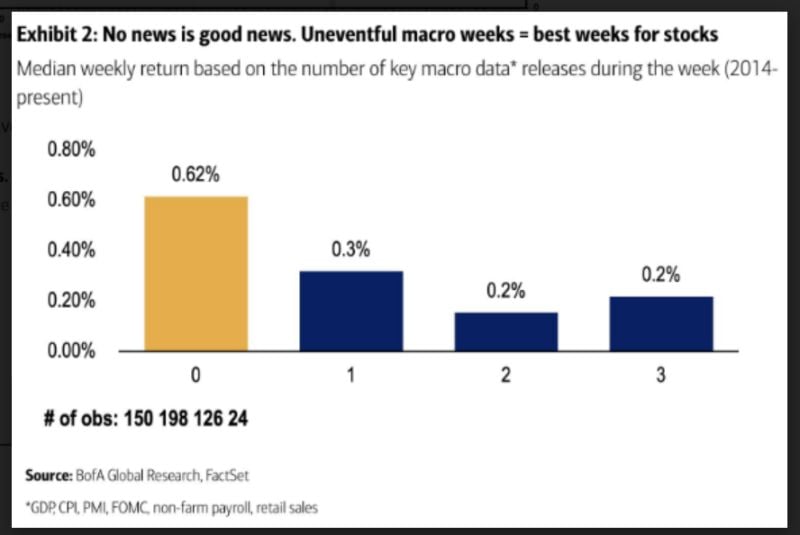

Non major macro weeks have been better...

Source: BofA

The true definition of ‘micromanager’ ?

Source: Corporate Rebels

JUST IN: The odds of SEC rejecting Ethereum ETFs by claiming ETH is a security have gone up

Source: Bloomberg's @JSeyff

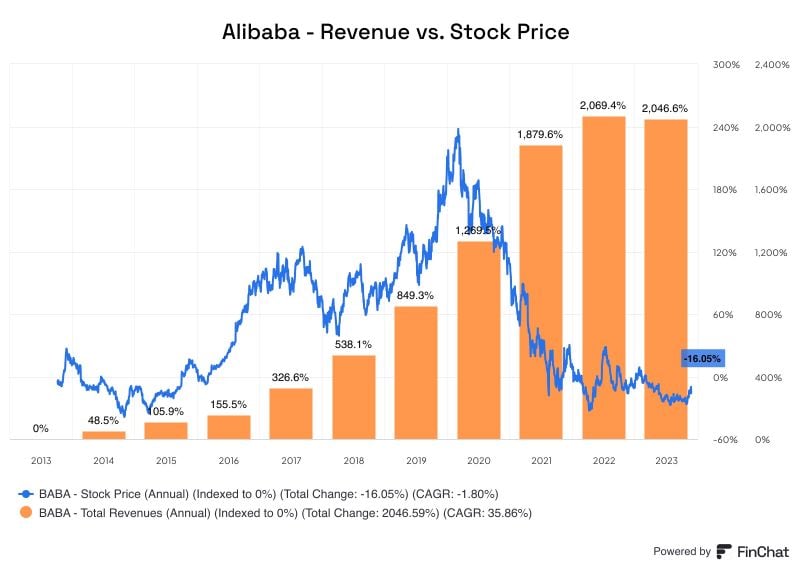

Alibaba revenue vs. stock price over the last 10 years

Revenue: +2,047% Stock Price: -16% $BABA

Radar🚨

BREAKING: Short sellers of GameStop $GME and $AMC have lost $5 billion in 2 days. Who are the short sellers by the way hedge funds ?

SUMMARY OF FED CHAIR POWELL'S COMMENTS (5/14/24):

1. "Overall a good picture looking at US economic data" 2. Inflation was notable in Q1 for the lack of further progress 3. Housing inflation has been a bit of a puzzle for the Fed 4. Restrictive policy may take longer than expected to lower inflation 5. Unlikely the Fed's next move will be an interest rate hike 6. "Credibility is everything for central banks" Source: The Kobeissi Letter

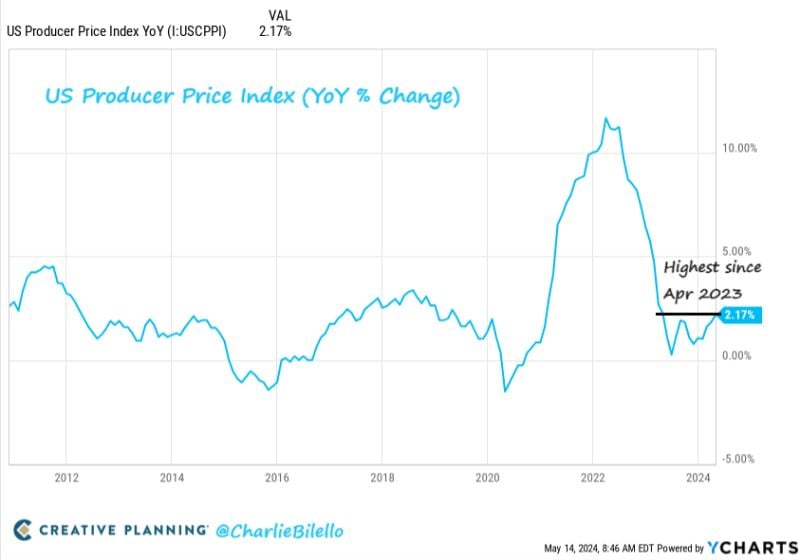

BREAKING: April PPI inflation RISES to 2.2%, in-line with expectations of 2.2%

Core PPI inflation was 2.4%, in-line with expectations of 2.4%. PPI inflation is now up for 3 straight months for the first time since April 2022. This is the highest PPI reading since April 2023. Note that revisions from last month’s PPI left people feeling it wasn’t as “hot” as initially thought on headline numbers. Source: Charlie Bilello

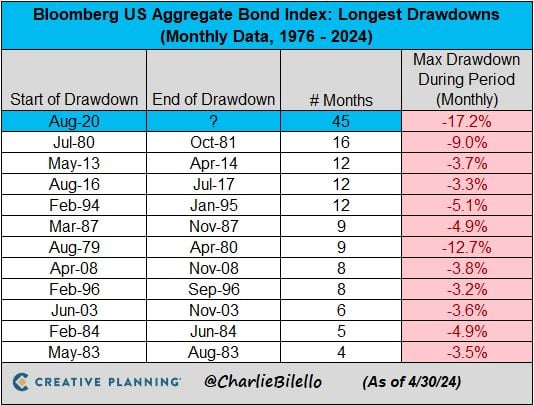

The US Bond Market has now been in a drawdown for 45 months, by far the longest bond bear market in history

Source: Charlie Bilello