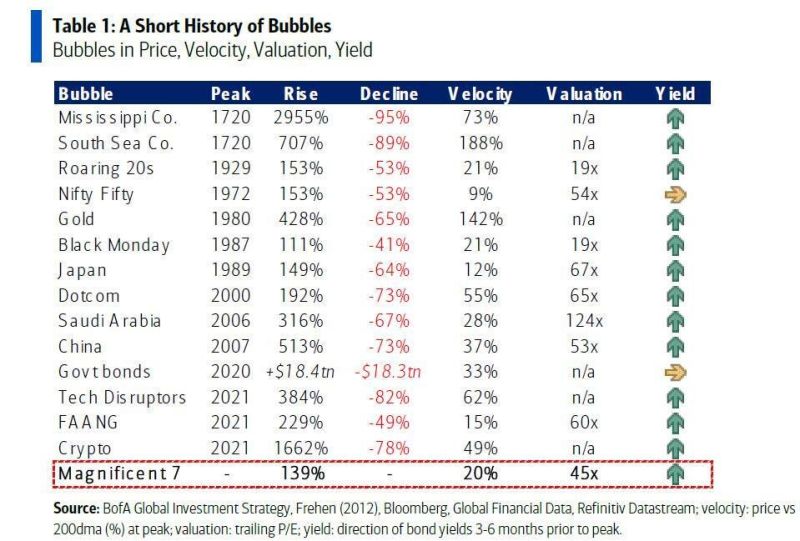

Is this time different?

Source: Markets & Mayhem, BofA

Storytelling is a powerful tool in presentations.

It connects ideas to emotions, making lessons memorable. Source: agrassoblog.org

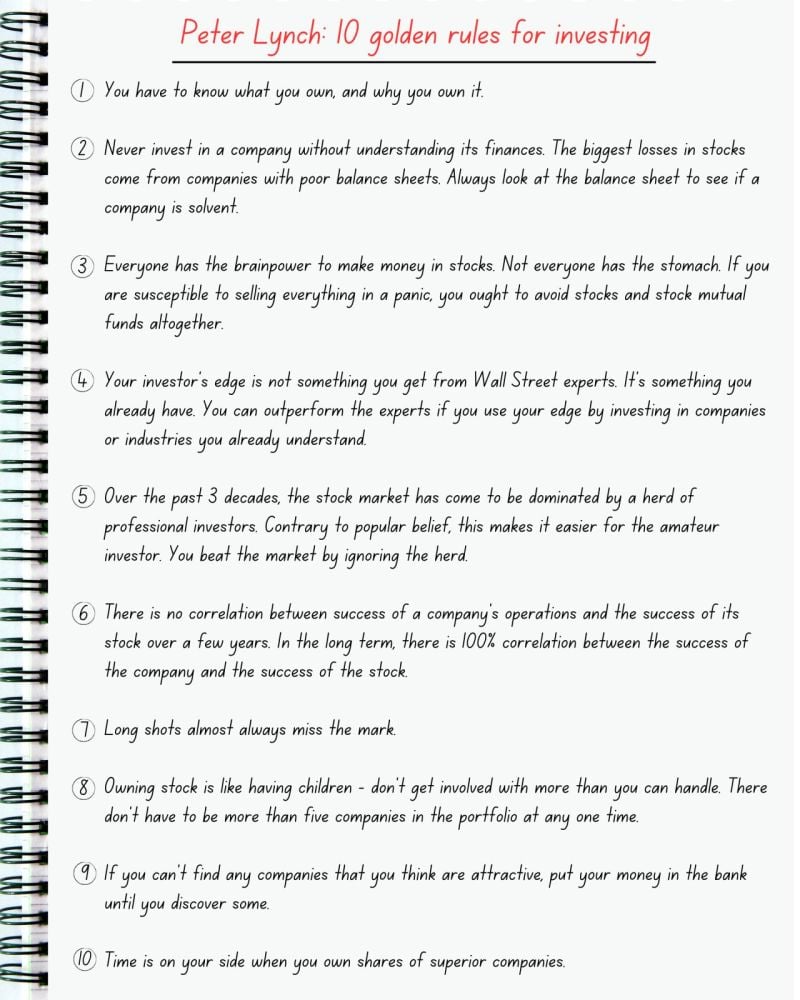

10 Golden rules for investing by Peter Lynch

Source: Compounding Quality, Pieter Slegers

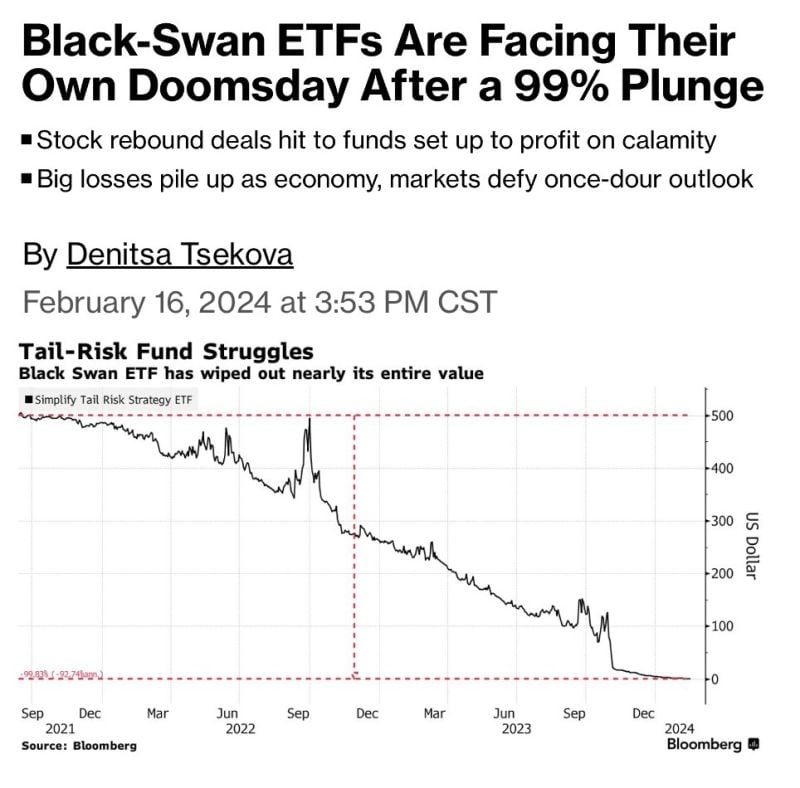

BREAKING 🚨: Black Swan ETFs

Black Swan ETFs have plunged 99% after doomsday dream scenario fails to play out Source: Barchart, Bloomberg

Invest In Assets | Stock Market Investing

If the business model is not right, the long-term returns won't be superior. You might have a temporary great management team that delivers superior results. However, in the long term, the returns will equate to the potential of the underlying business model. Source: Invest in Assets

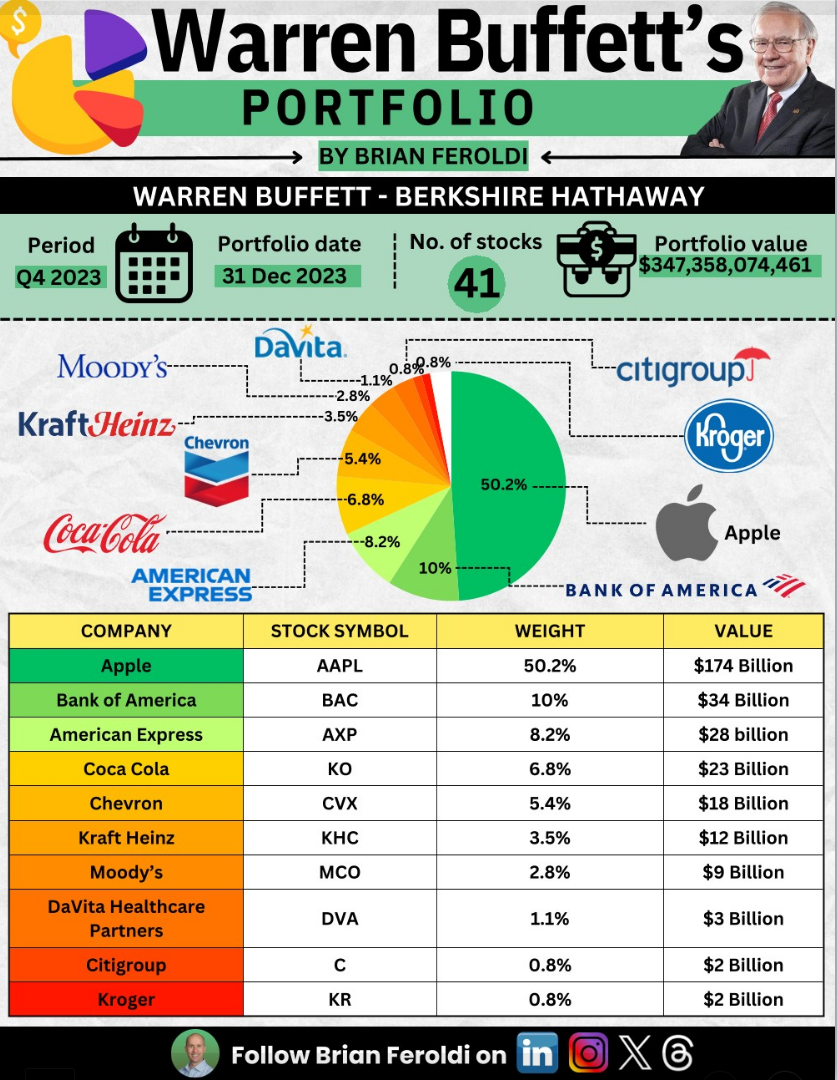

SUPER INVESTOR PORTFOLIO UPDATES - Q4 2023 📈by Brian Feroldi

Every 90 days, portfolio managers must disclose their holdings to the SEC. Attached are the current top holdings of 10 incredibly successful investors: 1: Warren Buffett - Value Investor 2: Howard Marks - Value Investor 3: Seth Klarman - Value Investor 4: Terry Smith - Growth Investor 5: Mohnish Pabrai - Value Investor 6: Guy Spier - Value Investor 7: Tom Gayner - Value Investor 8: Mark Massey - Growth Investor 9: Francois Rochon - Value Investor 10: Dan Davidowitz - Growth Investor

Nikkei 225 hit 38k level this week. Last time it happened was 1989...

See below the level of other indices at the time... Source. Bloomberg

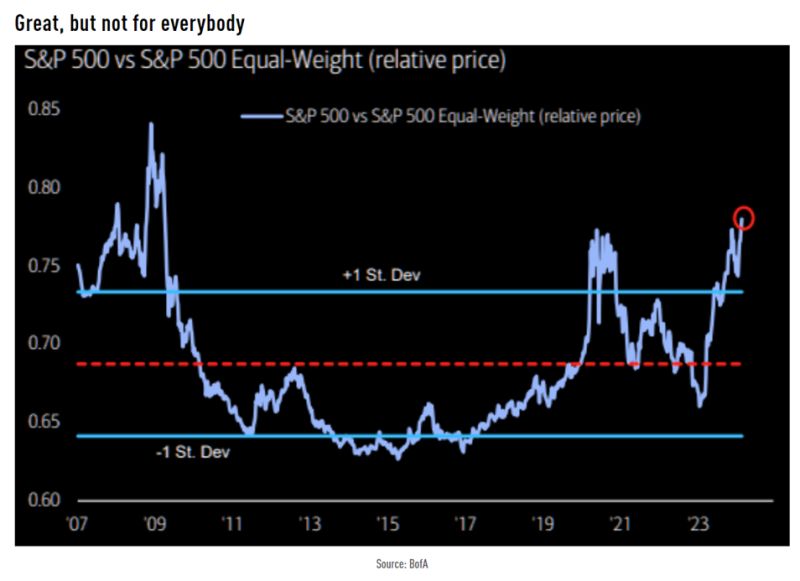

BofA Hartnett: "top 5 stocks = 75% of S&P500 YTD gain

Top 3 tech stocks = 90% of tech sector YTD gain, US equity “breadth” currently worst since Mar’09". Source: BofA, TME