The Atlanta Fed's gauge of sticky inflation has risen to about 5% on a 3-month annualized basis.

Inflation is moving in the wrong direction for the Fed, so it's interesting that the market's base case is still that the Fed is going to cut rates by about 100bp by January 2025. Source: Bloomberg, Lisa Abramowitz.

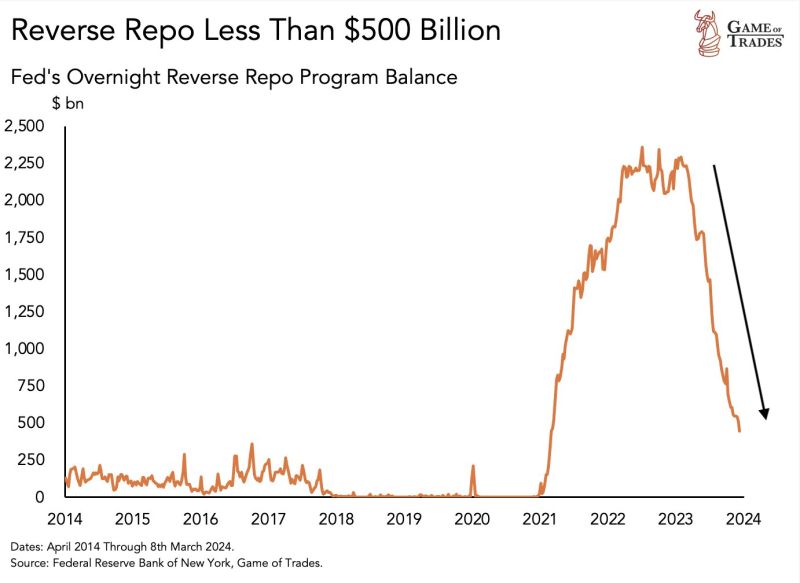

WARNING: Reverse Repo is falling off a cliff.

And has declined from more than $2500 billion to less than $500 billion since 2023. Source: Game of Trades

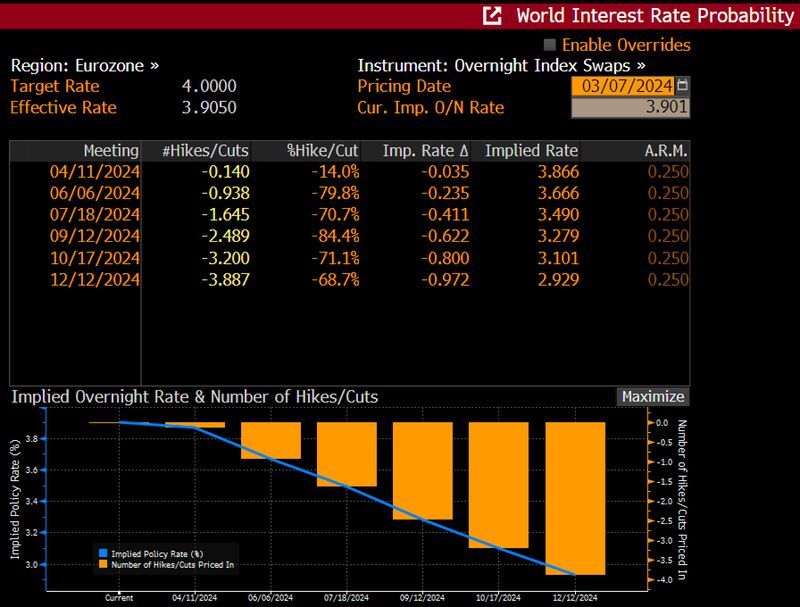

ECB’s Lagarde signals June rate cut w/2% inflation in sight.

Markets agree and price in 97bps cut for 2024. Source: Bloomberg, HolgerZ

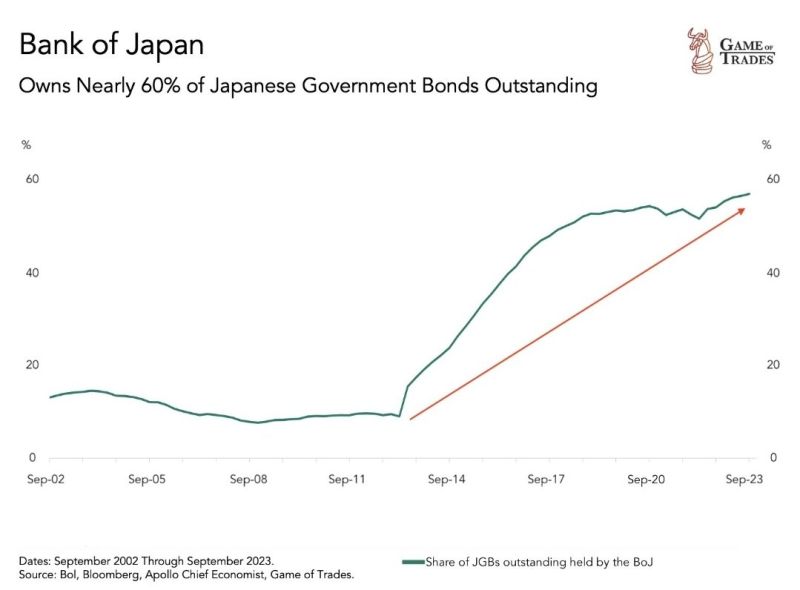

Bank of Japan boj now owns nearly 60% of the entire Japanese government bonds

Source: Game of Trades

As expected, the ECB lefts rates unchanged.

The European Central Bank approach continues to follow a data-dependent approach in determining rate path. THE STATEMENT • Inflation forecasts by ECB staff have been lowered, especially for 2024, largely due to reduced energy price pressures. Inflation is now expected to average 2.3% in 2024 and to stabilize around 2.0% in the following years; core inflation projections also revised downwards. They nevertheless say that domestic price pressures remain high, partly due to wages. They say that domestic price pressures remain high, partly due to wages. • Growth projections for 2024 have been downgraded to 0.6%, with a gradual recovery anticipated, leading to 1.5% growth in 2025 and 1.6% in 2026. • The ECB believes current interest rates, if maintained, will significantly contribute to reducing inflation and has committed to keeping rates at restrictive levels as needed. MARKET REACTION • EUR/USD is weaker on the news (to 1.0875) and EUR rates extend their move lower (they were already down every day this week, and prior to the ECB announcement). German 10y is down -7bp to 2.25% at the time we write • Rate cuts expectations are slightly increased for this year, but not massively so far (still four 25bp rate cuts by the end of the year when rounding the probabilities) OUR TAKE • Overall, this is a rather dovish statement for now - let see if Lagarde press conference will reinforces the dovish reading or if she counterbalances the message from the downward revisions on growth in inflation. Source: chart: Bloomberg

With Powell's remarks, Wall Street's hopes for a March rate cut (once 97%) officially hit 0.

With Powell's remarks today, Wall Street's hopes for a March rate cut (once 97%) officially hit 0. "Maybe he should consider using models that have been consistently accurate, instead of listening to those who give him 'different answers' (his words) that have been consistently wrong." From : Mitchel Krause, hedgeye : With Powell's remarks today, Wall Street's hopes for a March rate cut (once 97%) officially hit 0. "Maybe he should consider using models that have been consistently accurate, instead of listening to those who give him 'different answers' (his words) that have been consistently wrong." From : Mitchel Krause, hedgeye :https://app.hedgeye.com/insights/147337-mitchel-krause-how-wall-street-s-hopes-for-march-cuts-quickly-collaps?type=guest-contributors

What will happen to gold if/when Fed cuts and real yields plunge to negative territory?

Source chart: The Macro Guy, Macrobond

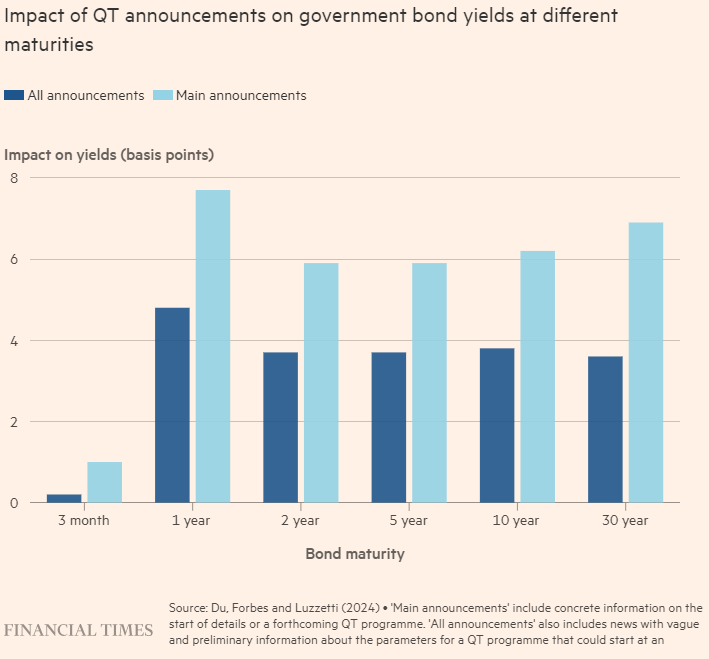

Unveiling the Impact of Quantitative Tightening: Intersting Insights from FT

🌟 Delving into recent insights from the Financial Times sheds light on the impact of Quantitative Tightening (QT) and its implications for financial markets. Let's break it down: 📊 QT's Functionality: Recent evidence from a study involving seven central banks, including the Fed's earlier QT efforts from 2017-2019, reveals that QT operates "in the background," subtly supporting central banks' endeavors to tighten financial conditions without significantly disrupting market functioning or liquidity. 💼 Market Reaction: Announcements of QT's commencement have led to slight increases in government bond yields. However, the actual implementation of QT, including outright bond sales, has had minimal disruptive effects on market dynamics and liquidity. 🔄 Passive vs. Active QT: The distinction between passive and active QT strategies is crucial. While passive QT (letting bonds mature) impacts short-end yields, active QT (outright sales) tends to steepen the yield curve, highlighting the nuanced effects of different QT approaches. 🤝 Market Support: The smooth adjustments observed in response to QT can be attributed partly to domestic nonbanks and, to a lesser extent, foreign investors stepping in to purchase securities as central banks reduce their holdings, maintaining market stability amidst changes in monetary policy. 💡 Navigating Future Challenges: What strategies will central banks employ to navigate the looming challenges posed by high government debt issuance and absorbed pandemic-era liquidity, in light of the insights gleaned from recent evidence on quantitative tightening's impact? #QuantitativeTightening #FinancialMarkets #CentralBanks #EconomicInsights