Global gold Production

Source: Barchart, Visual Capitalist

This is how store of values perform against a collapsing fiat currency...

Source: Trading view

China is buying/importing gold like there is no tomorrow

Source: Willem Middelkoop

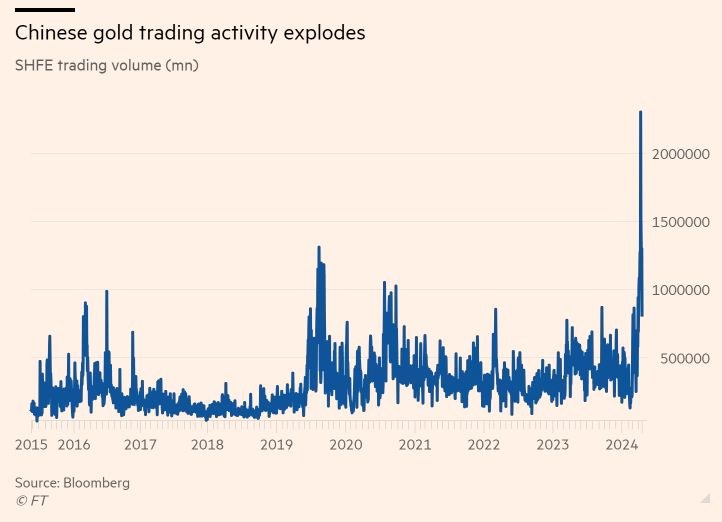

Gold Trading Volume in China has exploded to 5x the average in 2023...

Source: FT, Barchart

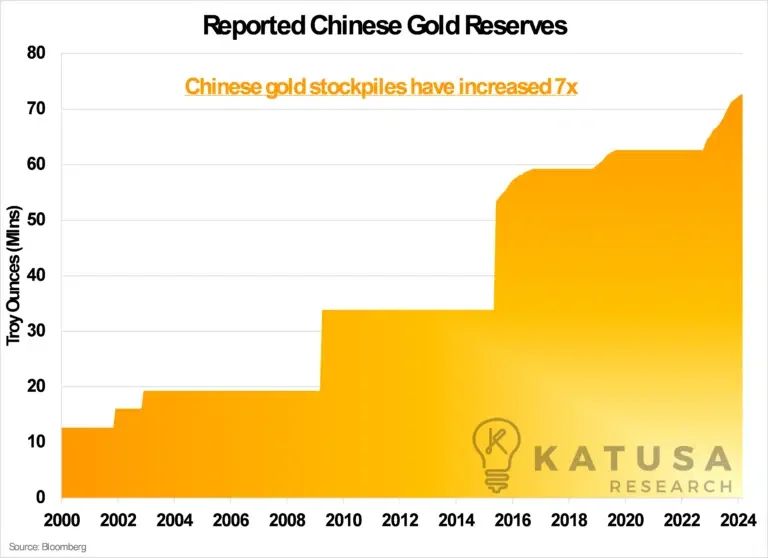

China has quietly accumulated large quantities of gold for 17 straight months – to the tune of 72.7 MILLION ounces (about 2,250 tonnes).

Despite its rise as an economic power, China’s vast reserves are predominantly in USD, an exposure it aims to minimize. To reduce this reliance, the People’s Bank of China is diversifying by increasing its gold holdings. Since 2011, China has decreased its dollar reserves by a third, down to approximately $800 billion. Meanwhile, China’s gold reserves have skyrocketed. China’s economic strategy involves diversifying away from the US dollar, which dominates global trade and commodity pricing. Source: Katusa Research

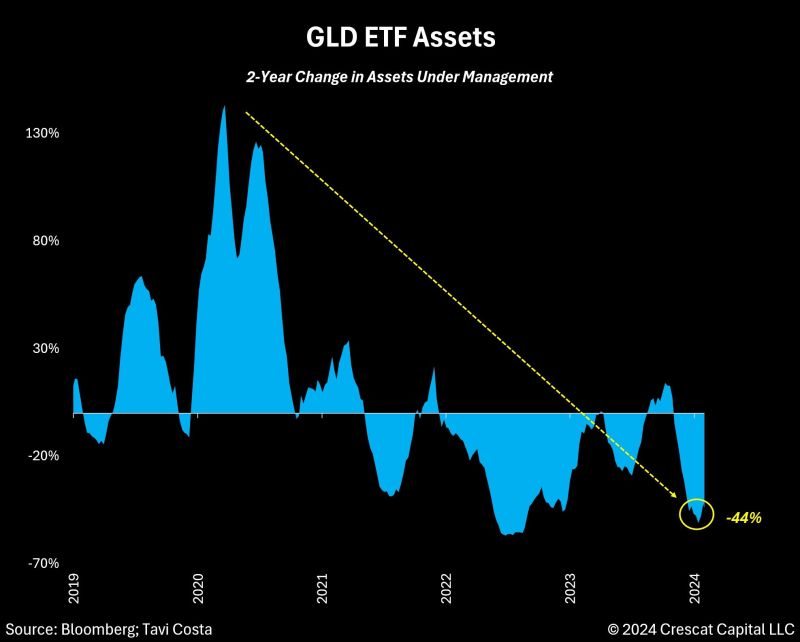

Gold rallied strongly again yesterday, disregarding entirely the significant reversal seen on Friday.

Meanwhile, the $GLD ETF is still facing significant outflows on a 2-year basis of nearly 45%. Source: Tavi Costa, Bloomberg

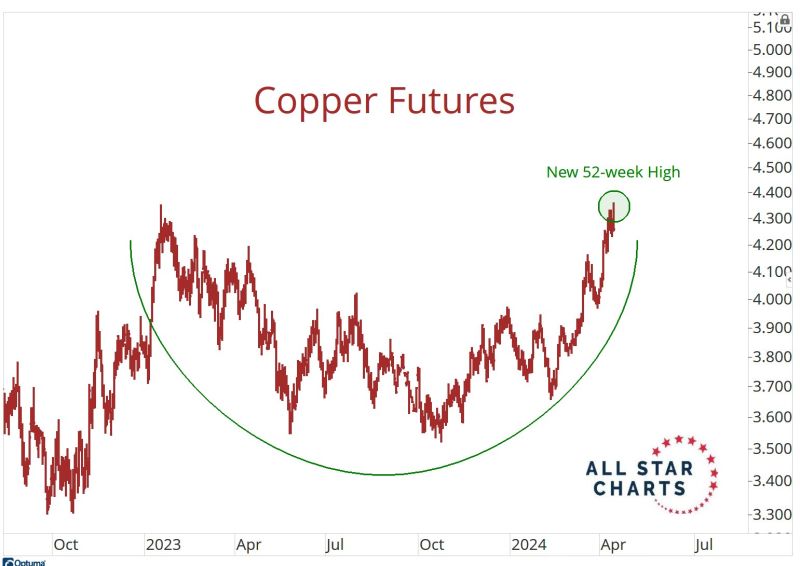

It's not just a Gold thing. It's a metals thing.

Copper hitting new 52-week highs. Source: J-C Parets

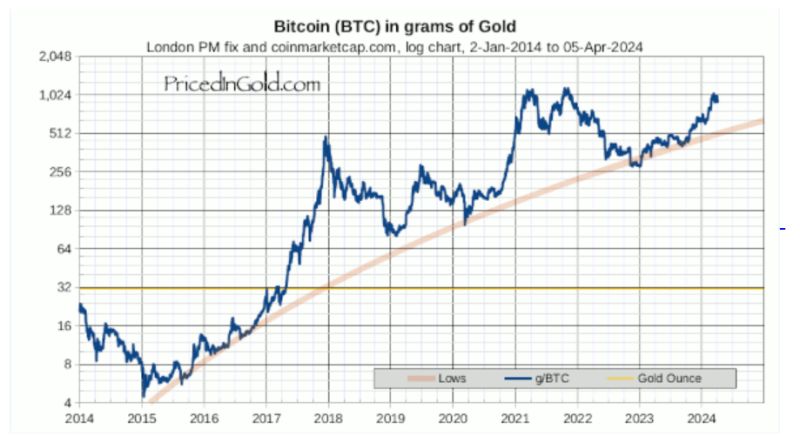

Bitcoin $BTC priced in grams of gold... (log chart)

Note that 1) $1,000 seems to be a key resistance; 2) Bitcoin hasn't made a new all-time high yet... Source: www.priceingold.com