Feed a family of 5 (hamburger, fries, shake) for $2.25 in June 1961

BLS CPI calculator says that's same as $23.24 today... Inflation calculator -> Source: Rudy Havenstein

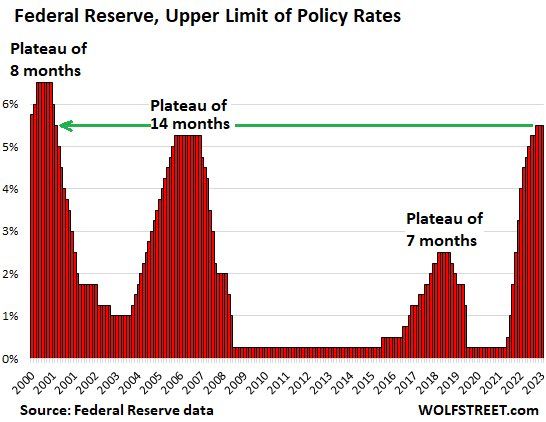

The end of the rate hikes is typically followed by plateaus before rate cuts begin

The end of the rate hikes may not be here yet, and the Fed has already said a many times for months that the plateau is going to be “higher for longer". How long will the plateau be this time? Source: Wolfstreet

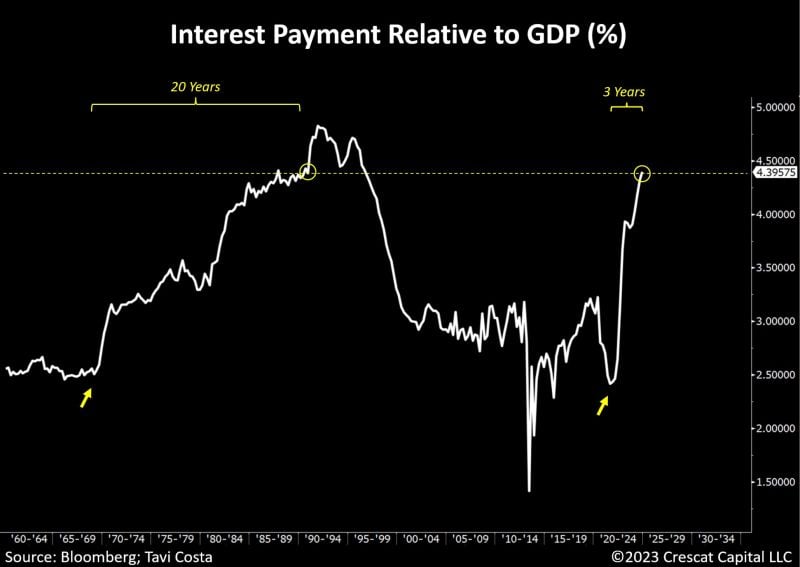

It took 20 years for US interest payments to reach 4.5% of GDP in the 1970s and 80s

Today, achieving the same level will take less than 3 years. This starkly highlights the speed of the rise in Treasury yields and the magnitude of the debt problem. Source: Tavi Costa, Bloomberg

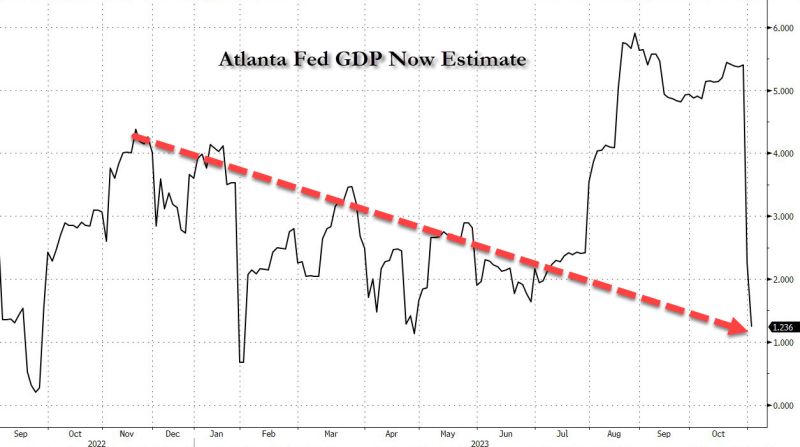

And we're back to Bidenomics trendline

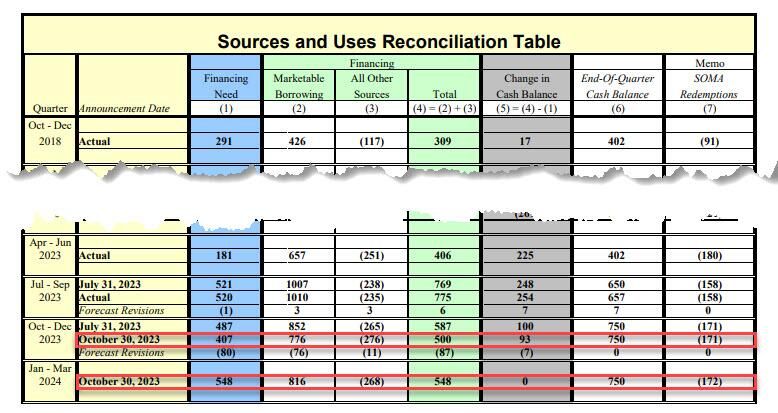

Source: www.zerohedge.com

No change as expected

Nothing really new except that they acknowledge strong growth and strong wage gains versus September, effectively upgrading their economic assessment. This is the 3rd time they upgrade their view on growth. Our view is unchanged: we are due for a long pause. High rates is the new normal.

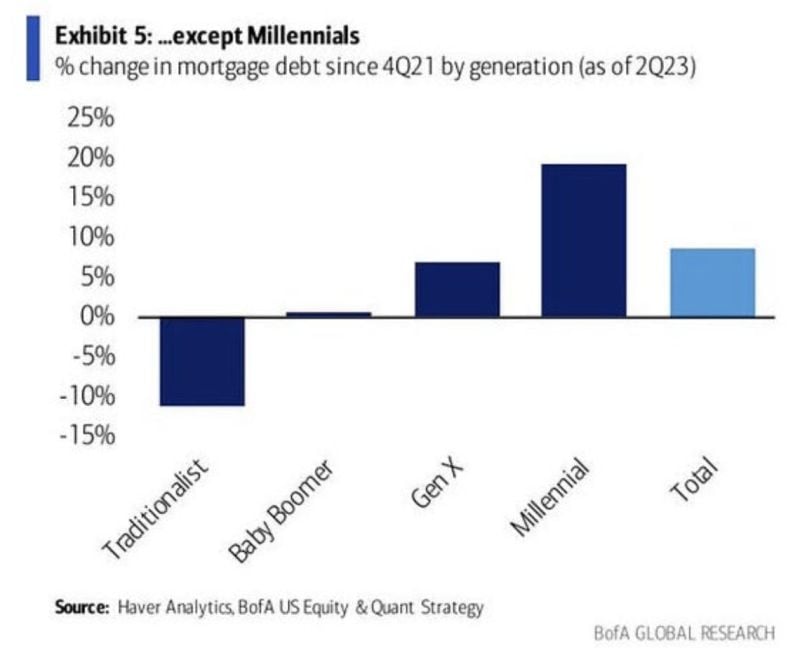

Who's buying houses with record high prices and 8% mortgage rates. The answer?

Millennials are piling in to new mortgages even with the spike in rates. Since Q4 2021, Millennials have seen a ~20% increase in mortgage debt. This is the same group of people who just had student loan payments return at an average of $500/month. It's a tough time to be a Millennial... Source: The Kobeissi Letter, BofA

US To Borrow $1.5 Trillion In Debt This & Next Quarter, After Borrowing A Massive $1 Trillion Last Quarter

During the October – December 2023 quarter, Treasury expects to borrow $776 billion in privately-held net marketable debt, assuming an end-of-December cash balance of $750 billion. The borrowing estimate is $76 billion lower than announced in July 2023, largely due to projections of higher receipts somewhat offset by higher outlays. During the January – March 2024 quarter, Treasury expects to borrow $816 billion in privately-held net marketable debt, assuming an end-of-March cash balance of $750 billion. Source: www.zerohedge.com

Eurozone inflation sinks to 2y low as Eurozone economy shrinks:

CPI slowed to 2.9% in Oct, down from 4.3% and better than expected 3.1%. But Core CPI – that excluding food & energy is retreating less rapidly. It moderated to 4.2% in October from 4.5% the previous month. Our take: disinflationary trend is firmly in place in the EZ although wage inf’still stickiness and more difficult comps in H2 prevent core inflation to decline more meaningfully. We believe there is enough progress for the ECB to stay put (i.e rates hike cycle is over) and potentially cut rates next year if EZ economy slows down meaningfully Source: HolgerZ, Bloomberg