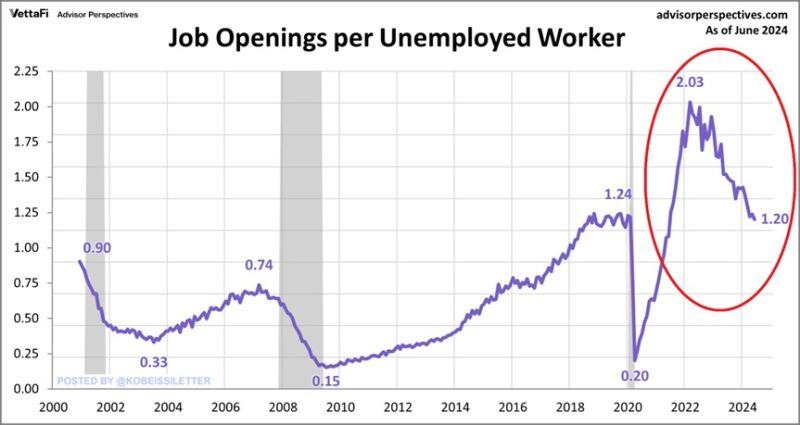

BREAKING: US job openings declined to 8.18 million in June, down from 8.23 million in May, near their lowest level since 2021.

Year-over-year, job openings fell 10.3%, marking the 23rd consecutive monthly decrease, the longest streak since the 2008 Financial Crisis. The ratio of vacancies per unemployed worker, a metric the Fed follows closely, fell to 1.20, the lowest since June 2021. At the same time, the private sector hiring rate declined to 3.7%, the lowest level since April 2020. The private quits rate, measuring the number of people who voluntarily leave their jobs, fell to 2.3%, the lowest since August 2020. This means that Americans are the least confident that they will find a new job since the 2020 Pandemic. => The US labor market is weakening. Source: The Kobeissi Letter

ISM PMI Employment came in at 43.4.

Only time lower: 1) the internet bubble popping. 2) the GFC. 3) Covid-19. Source: James E. Thorne, Bloomberg

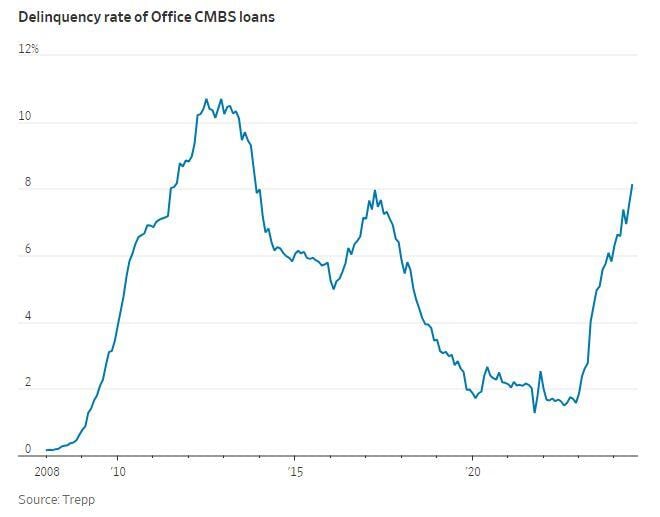

Delinquency rates on Office building loans hit 8.11%, the highest in more than a decade 🚨

Source: Barchart

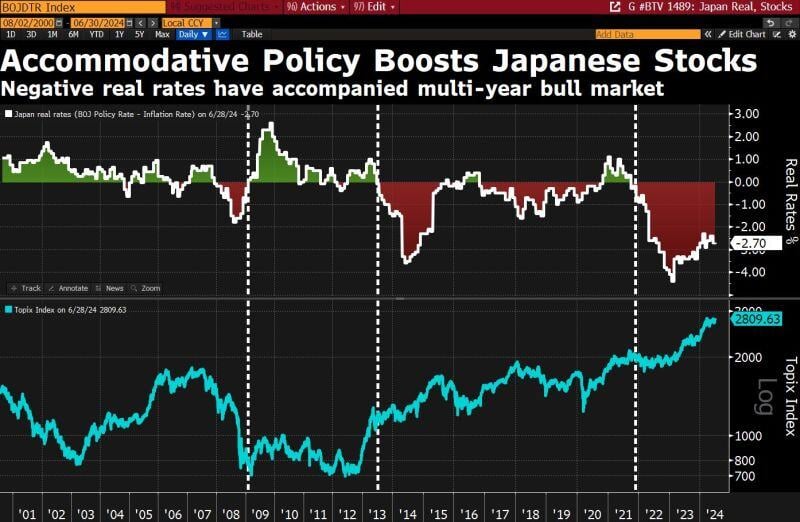

Loose policy = Bull market

Even if the BOJ hikes a few more times, real rates will remain deeply negative, a sign of accommodate policy. Chart tracks Japan real rates & market performance ➡️ 2009 -2013: period of high real rates, languishing stock market🔻 ➡️2013-2021: BOJ floors rates, pushes rates negative and fuels stock rally ✅ ➡️ 2021-2024: inflation picks up, real rates drop even further negative, Topix rallies 50% ✅✅ Source: David Ingles, Bloomberg

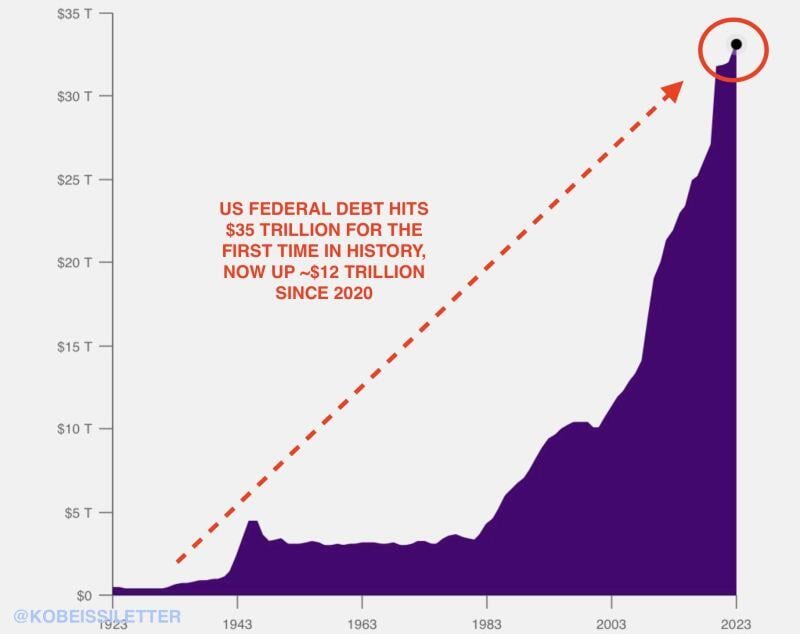

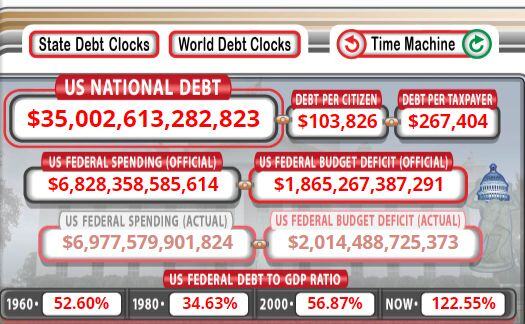

Total US Federal debt has officially hit $35 trillion for the first time in history.

Since 2020, the US has now added ~$12 TRILLION in Federal debt. In other words, the US has added an average of ~$280 BILLION of Federal debt EVERY MONTH since January 2020. This means that the US now has ~$105,000 in Federal debt for every person living in the country. All while deficit spending as a percentage of GDP is currently at World War 2 levels. Source: The Kobeissi Letter

German inflation unexpectedly accelerated in July to 2.3% YoY from 2.2% in June as food price inflation keeps rising, core inflation, and services inflation remain sticky at 2.9% and 3.9%.

Source: HolgerZ, Bloomberg

JUST IN: U.S. National Debt surpasses $35 Trillion for the first time in history

Source: Barchart

In the US, if your income and net wealth has not increased by 25% since 2020 you are poorer now than four years ago...

Source: Michel A.Arouet