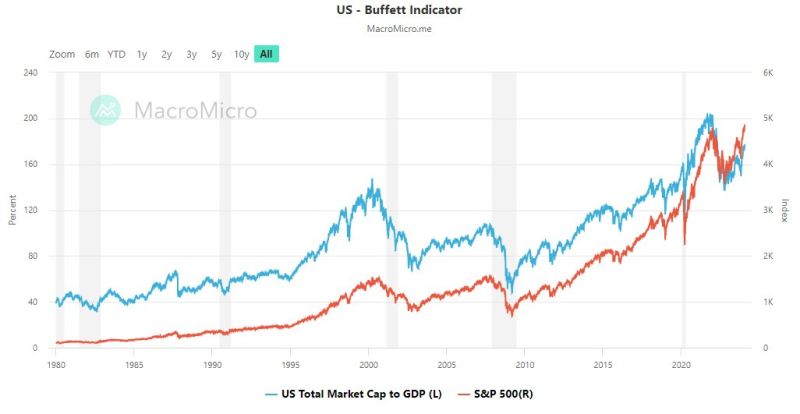

The Buffett Indicator (total value of all publicly-traded stocks/GDP) is near all-time highs and at a significantly higher level than during the Dot Com Bubble and the Global Financial Crisis.

Source: Macro Micro, Charlie Bilello

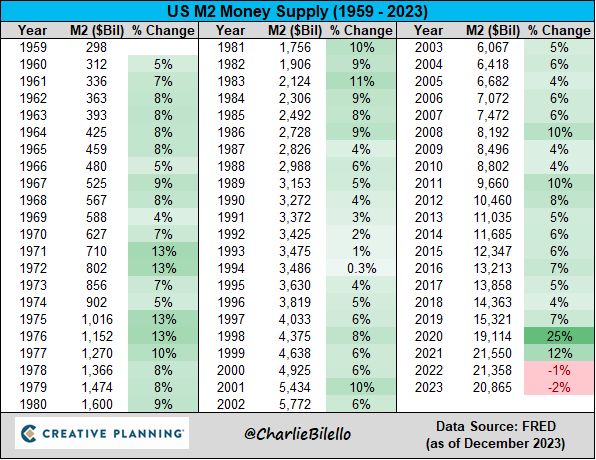

The US Money Supply decreased by 2% in 2023, the largest annual decline on record with data going back to 1959

This was the second straight annual decline which followed the record 40% expansion in the money supply in 2020-21. Source: Charlie Bilello

US earnings: things get fun starting this week

Source: The Transcript, Brad Freeman / StockMarketNerd

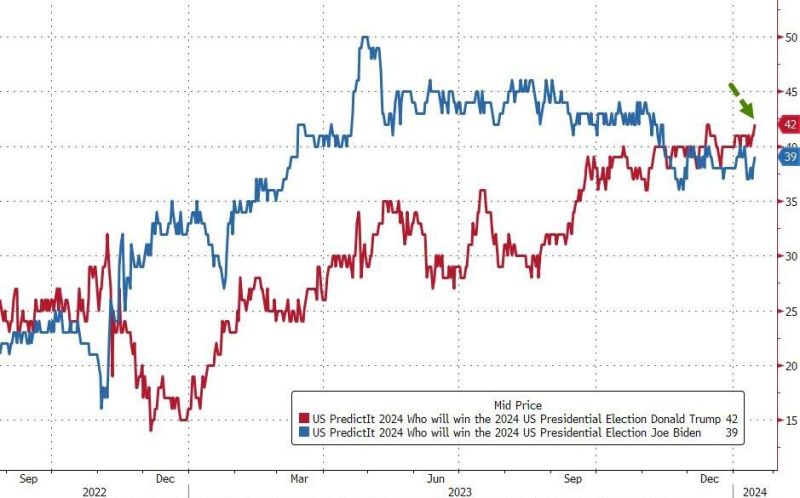

US presidential election update:

DeSantis drops out of Republican race

Trump's odds of winning the election are now at the highest, and 3 ppts above Biden.

As Goldman notes, on balance, a Republican 'sweep' looks likely to increase the chances of a stronger USD, higher breakeven inflation rates, higher yields, and a steeper yield curve. It may also increase the tails in both directions for energy prices. Source: Predictit, www.zerohedge.com, Bloomberg

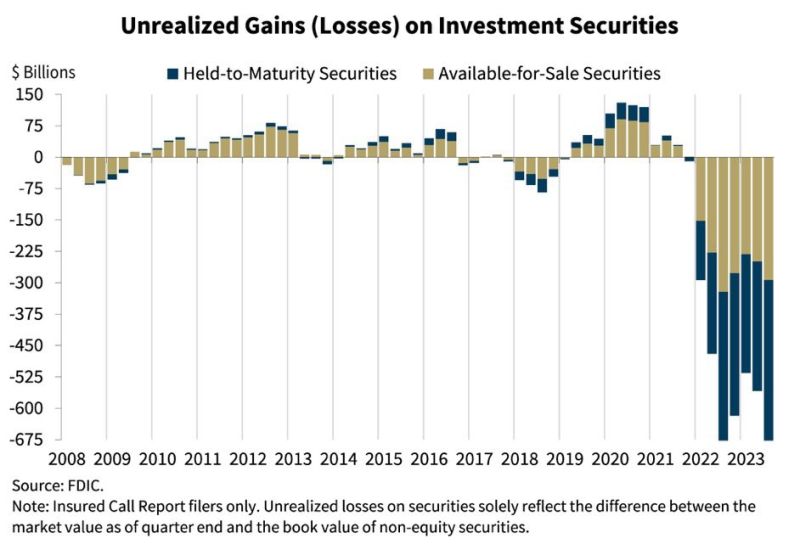

U.S. Banks are facing unrealized losses of roughly $685 billion. They are desperately hoping the Federal Reserve will cut rates sooner rather than later.

Source: Barchart, FDIC

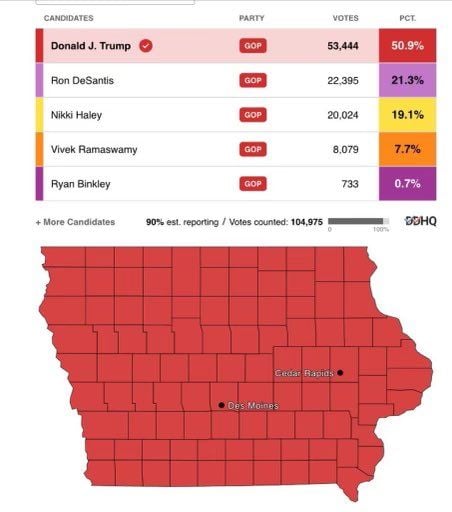

IOWA REPUBLICAN CAUCUS: TRUMP MADE HISTORY BY WINNING ALL 99 COUNTIES AND WINNING BY THE LARGEST MARGIN EVER.

The Iowa caucus on January 15 launches the long designation process of the Republican and Democrat candidates to the US presidential election. On that day, only Republicans will vote (Democrats will hold their own later in 2024). While Iowa is a small state, and not very representative of the country’s population (90% of Iowa’s population is white and in past elections, the Iowa caucuses have rarely predicted what will happen in other primaries), it is seen as very important for candidates to gather positive momentum for the remaining of the campaign and the following state caucus and primaries. In the current context, the Iowa caucus may already provide a hint on whether any challenger to Trump within the Republican party has the potential to compete with the former President, or not. Rival campaigns and many political pundits had argued that if Trump failed to top 50% of the vote, he wouldn't meet expectations.

NEW: US BlackRock updated their home page to showcase their new spot Bitcoin ETF

Source: Bitcoin Magazine