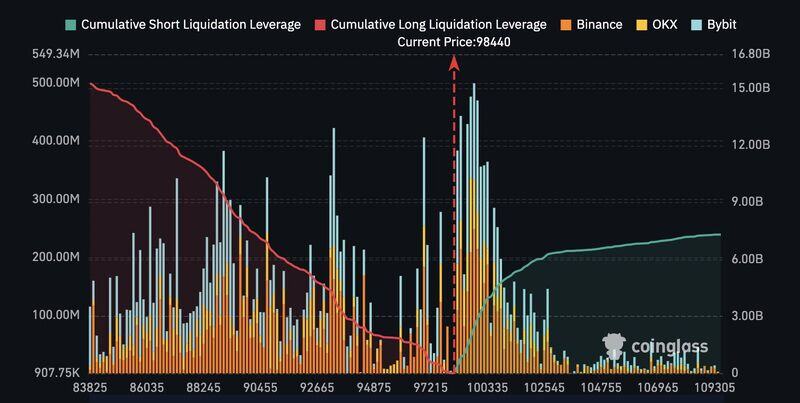

$8 BILLION worth of Bitcoin shorts to be liquidated at $110,000

Source: Vivek

HISTORY: With OVER 1,200,000 BTC, Wall Street hashtag#ETFs now hold more Bitcoin than Satoshi Nakamoto

Source: The Bitcoin Historian

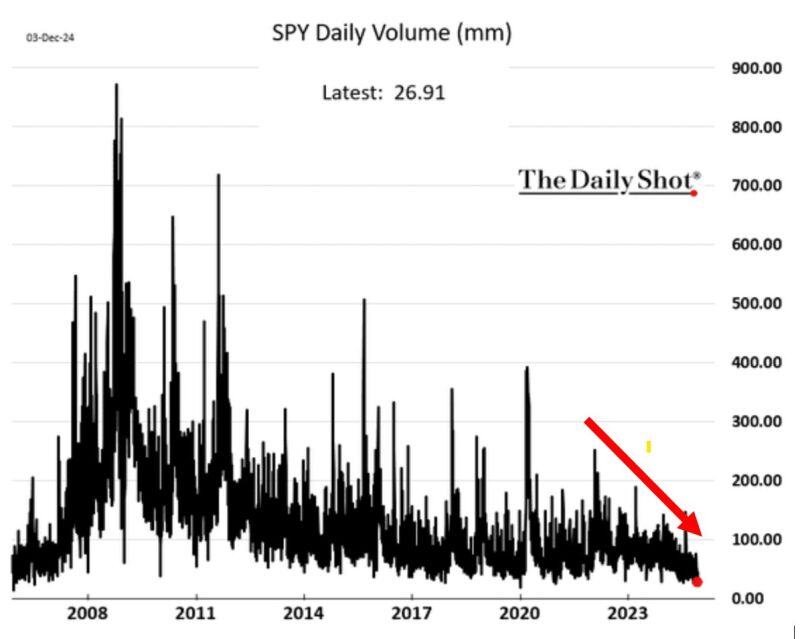

US STOCK MARKET LIQUIDITY IS FALLING

S&P 500 ETF daily trading volume PLUNGED to 26.9 million on Tuesday, near the lowest since 2007. At the same time, S&P 500 futures trading volume FELL to the lowest in 3 YEARS. This increases the risk of some wild moves going forward. Source: Global Markets Investor, The Daily Shot

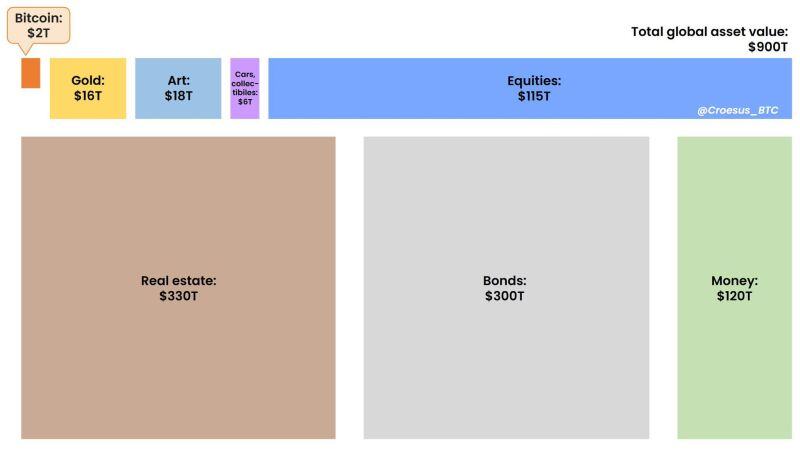

Bitcoin is still just 0.2% of global asset value.

Here is the latest update of this chart, which you may have seen in Microstrategy CEO Michael Saylor's presentations. With Bitcoin's price over $90k and ~$2T in market value, it may feel like you're late to Bitcoin... but it is still a tiny bucket in the global asset ocean. Source: Jesse Myers (Croesus 🔴) @Croesus_BTC

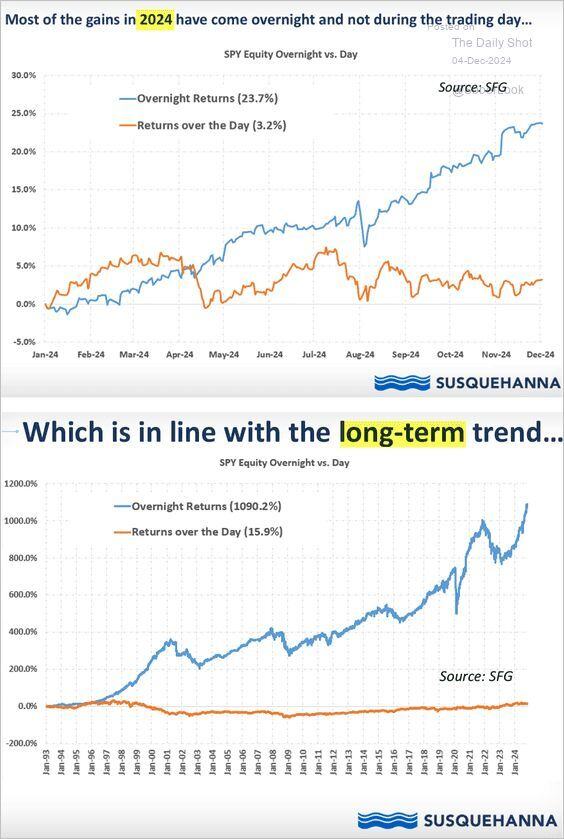

Overnight gains in US equities have massively outpaced intraday gains.

Source: Chris Murphy, Susquehanna International Group, The Daily Shot

As the old adage says... "Concentration makes you rich. Diversification keeps you rich".

#BTC

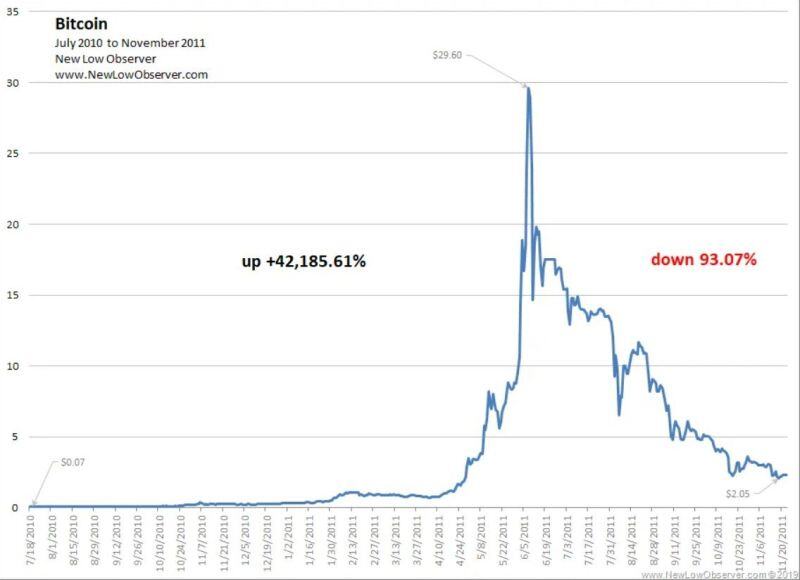

How it started... the first 16 months of existence of bitcoin

Source: zerohedge

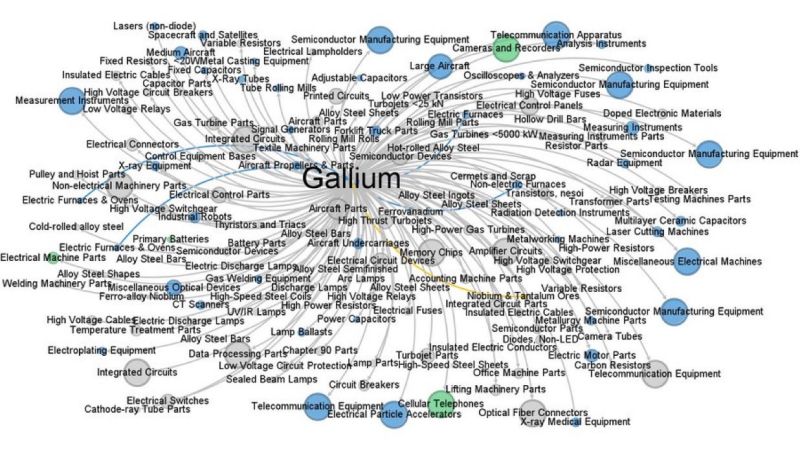

🚨China export bans Gallium & Germanium🚨

Why it matters: Gallium is central to countless downstream industries: semiconductors, aerospace, telecommunications, & more. This image shows how interconnected it is👇 Source: DeepBlueCrypto