The bulls are running WILD pre-market. Thank you Mr Powell...

$DIA +1.18% $SPY +1.61% $QQQ +2.18%

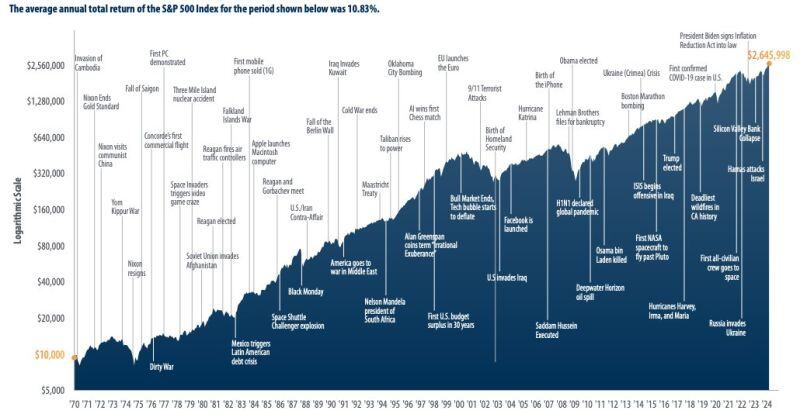

Regardless of what is happening in the world, or who happens to be President, the market finds a way forward.

Source: Peter Mallouk

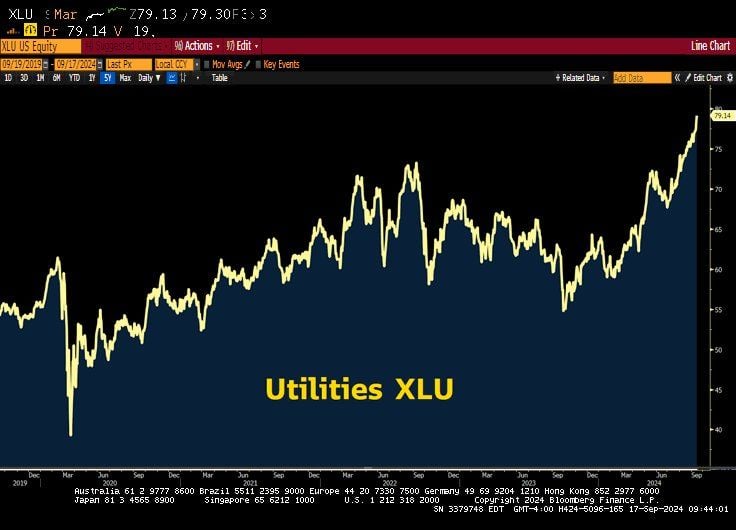

Utilities Destroying Mag 7 in 2024?

Utilities $XLU +27% Amazon $AMZN +21% QQQ +16% Microsoft $MSFT +15% Apple $AAPL +13% Google $GOOGL +13% Tesla $TSLA -9% Source: Lawrence McDonald @Convertbond, Bloomberg

BlackRock is preparing to launch a more than $30bn artificial intelligence investment fund

With technology giant Microsoft to build data centres and energy projects to meet growing demands stemming from AI, people briefed about the matter said https://on.ft.com/3Bh2aGG Source: FT

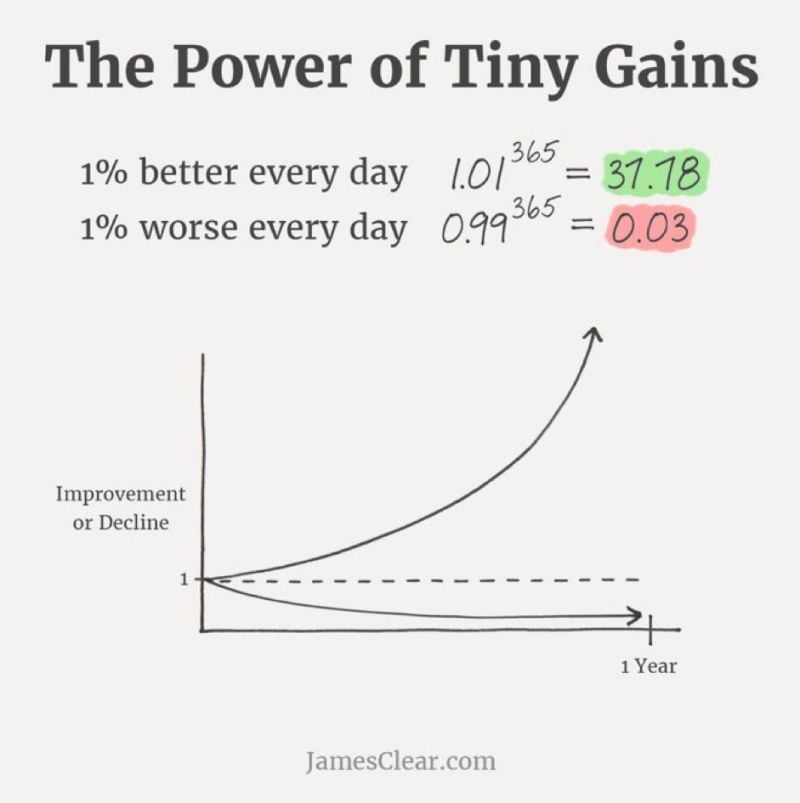

The power of tiny gains

Source: Invest in Assets

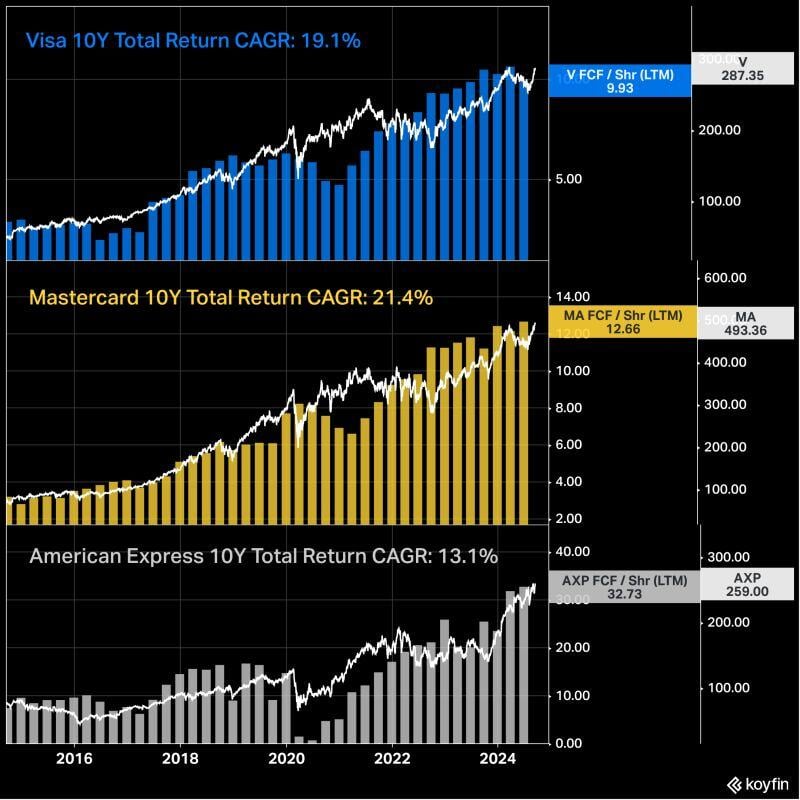

Visa, Mastercard, and American Express' FCF per share and share price over the last decade.

10Y Total Return CAGR: $V Visa: 19.1% $MA Mastercard: 21.4% $AXP American Express: 13.1% Source: @KoyfinCharts

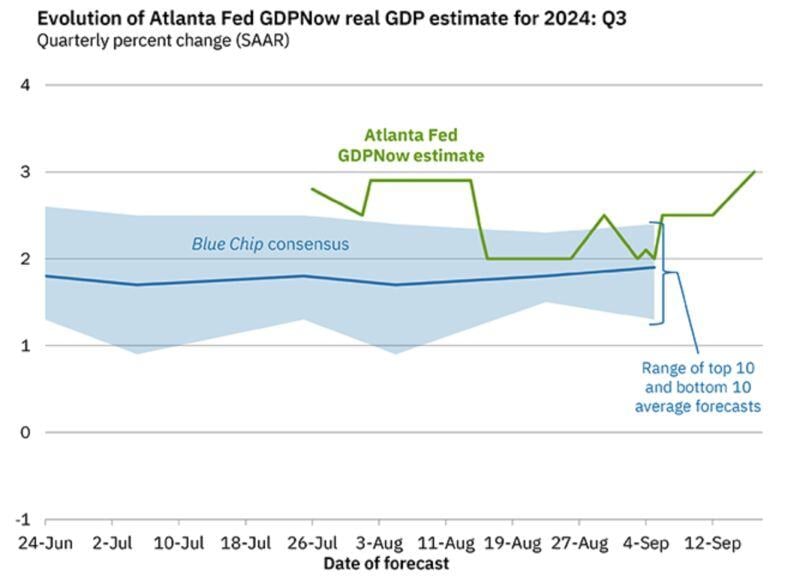

Soft landing? Hard landing? Or no landing?

Atlanta Fed Q3 Real GDP growth Nowcast model just hit 3%...

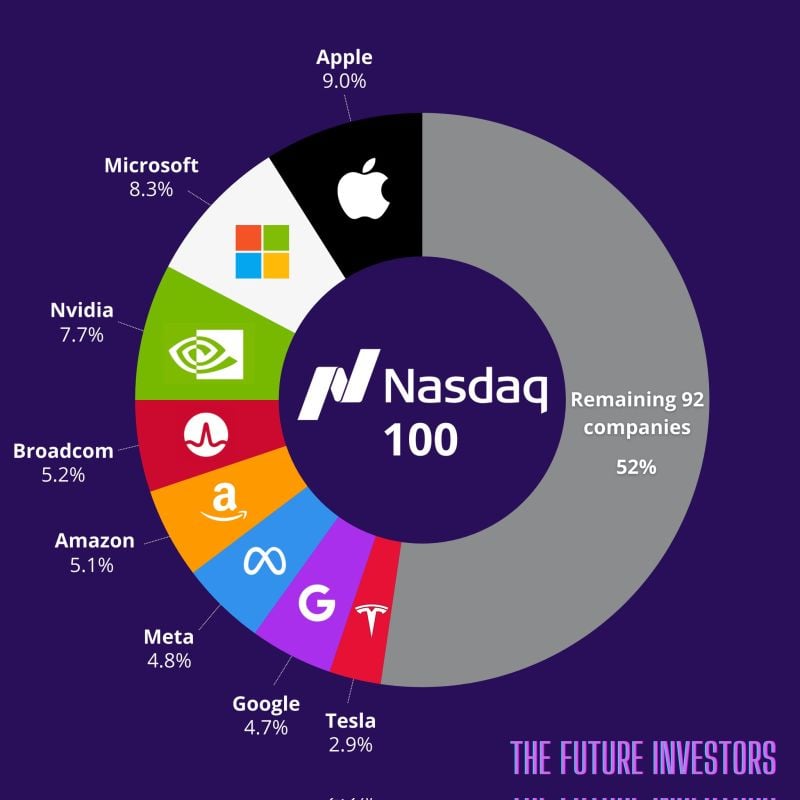

Here’s what you actually buying when you invest $1,000 in a Nasdaq 100 ETF $QQQ:

$AAPL - Apple - $90 $MSFT - Microsoft - $83 $NVDA - Nvidia - $77 $AVGO - Broadcom - $52 $AMZN - Amazon - $51 $META - Meta - $48 $GOOGL - Google - $47 $TSLA - Tesla - $29 Remaining 92 stocks: $523 Source: The Future Investors