The European Commission has denied that its internal market commissioner had approval from Ursula von der Leyen to send the letter

one EU official saying, 'Thierry has his own mind and way of working and thinking'. Source: FT

Naval Ravikant Happiness Theory

Source: artofpoets.com

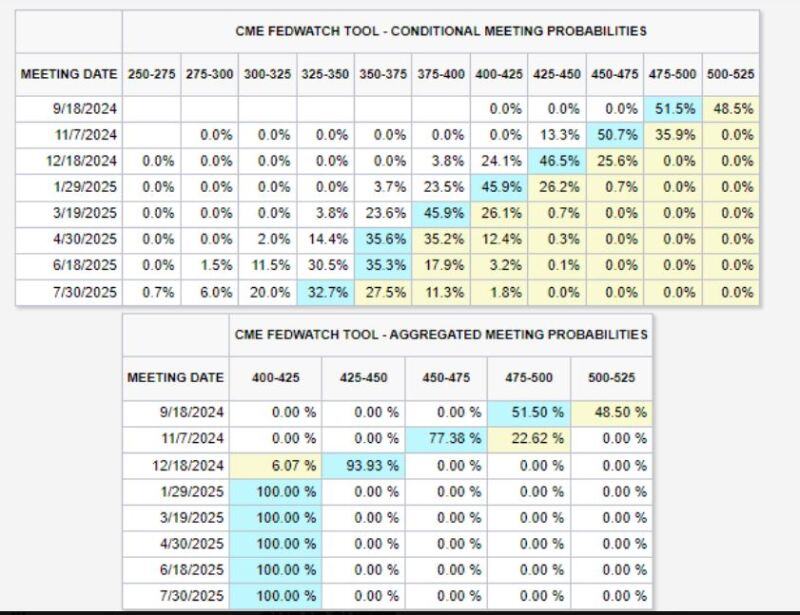

105bps of fed rate cuts are now priced into 2024.

Source: Mike Z.

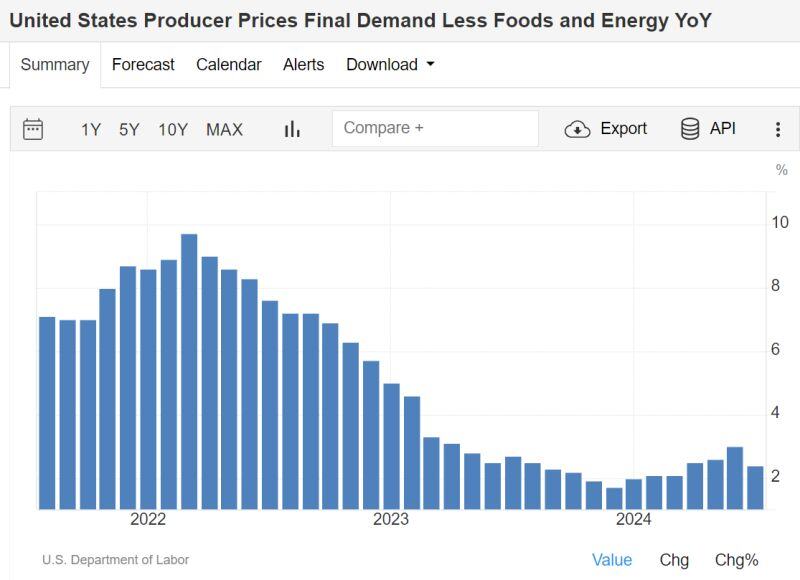

BREAKING: US July PP inflation falls to 2.2%, below expectations of 2.3%

Core PPI inflation falls to 2.4%, below expectations of 2.7%. This is the first drop in Core PPI YoY since December last year... In another constructive sign, PPI inflation is now at its lowest level since March 2024. A September hashtag#fed rate cut seems to be on its way. PPI numbers in a nutshell: - PPI 0.1% MoM, Exp. 0.2% - PPI Core 0.0% MoM, Exp. 0.2% - PPI 2.2% YoY, Exp. 2.3% - PPI Core 2.4% YoY, Exp. 2.6% Source: The Kobeissi Letter, US Department of Labor, Mike Z.

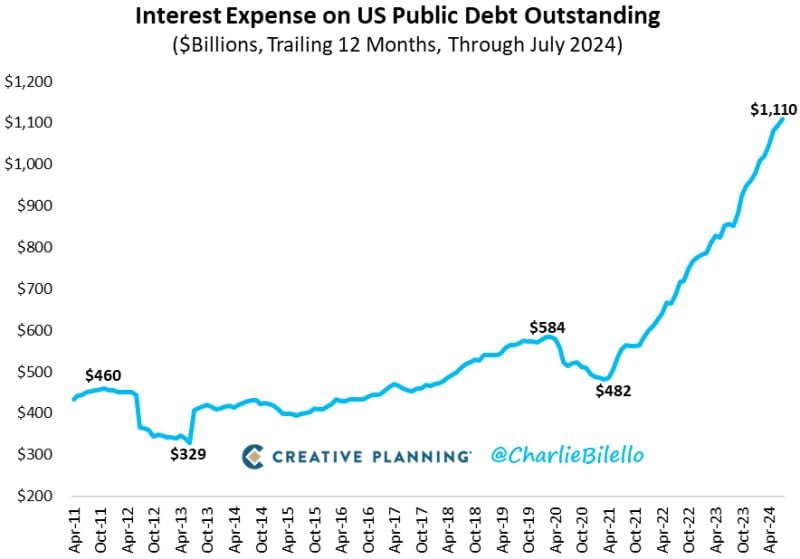

The Interest Expense on US Public Debt rose to a record $1.11 trillion over the last 12 months, more than doubling over the past two years

At the current pace it will soon be the largest line item in the Federal budget, surpassing Social Security. Source: Charlie Bilello

Athletes from four California universities won 89 Olympic medals. (The United States won 126 total).

Athletes from Stanford University alone won more medals than all but seven countries in the world. Source: Erik Brynjolfsson

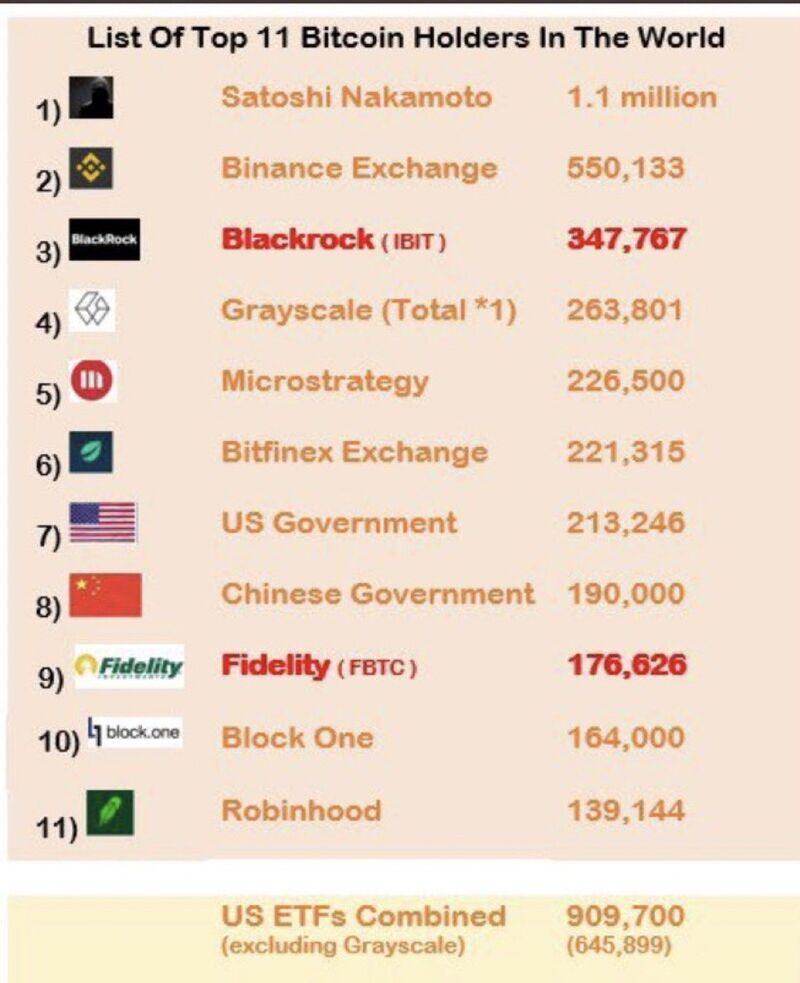

Bitcoin, ETFs on track to surpass the Satoshi stack by the end of 2024

Source: Bitcoin news

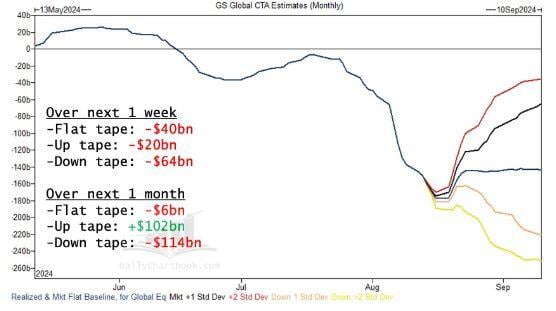

CTAs are projected to sell global stocks in every single scenario over the next week, up to a total of $64 billion if the market trades lower, warns Goldman Sachs!

Source: GS, Barchart