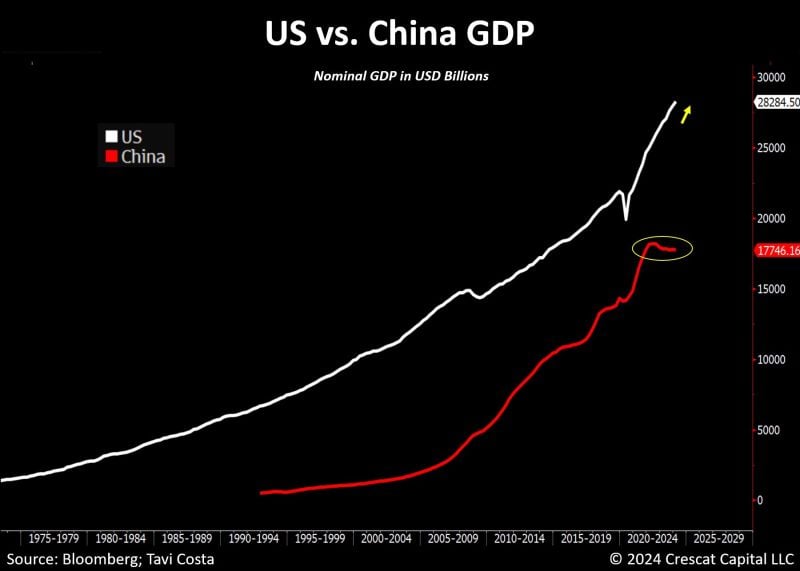

As highlighted by Tavi Costa, this is one of the reasons China is enhancing teh quality of its international reserves and accumulating gold:

China’s macro imbalances are increasing pressure on its monetary system to devalue. Source: Bloomberg, Tavi Costa, Crescat Capital

One step at a time.

Source: Psyche Wizzard

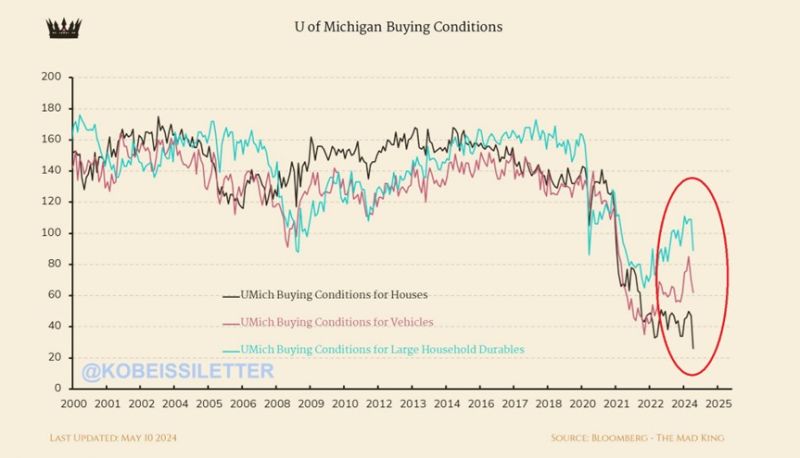

Homebuyer conditions for US consumers plummeted to their lowest level in history this month.

The index of buying conditions for houses fell to ~30 points which is below the previous low of ~40 points in the early 1980s. In just 4 years, conditions for buying a house have dropped by 110 points, a massive 73% decline. Meanwhile, buying conditions for vehicles and large household durables are down for 3 straight months. Source: The Kobeissi Letter

S&P 500 $SPX hasn't declined by 2% or more for 317 consecutive trading days, the longest streak since a 351-day stretch that lasted from Sep 2016 through Feb 2018.

Source: Barchart

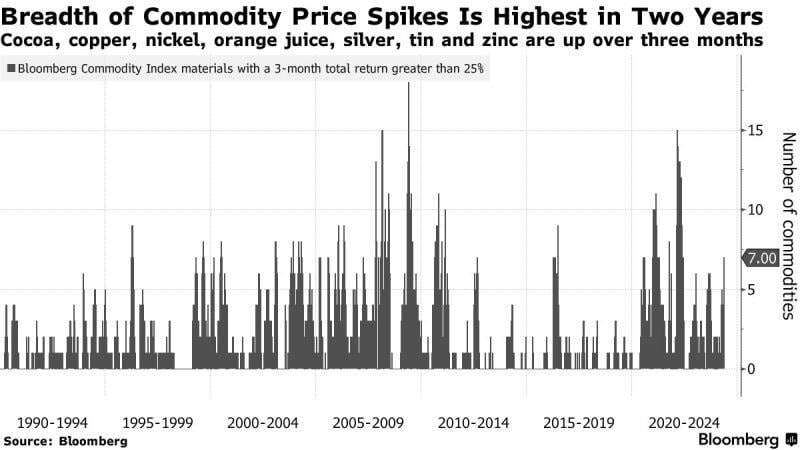

The breadth in commodity price spikes is the highest in two years

Source: Bloomberg

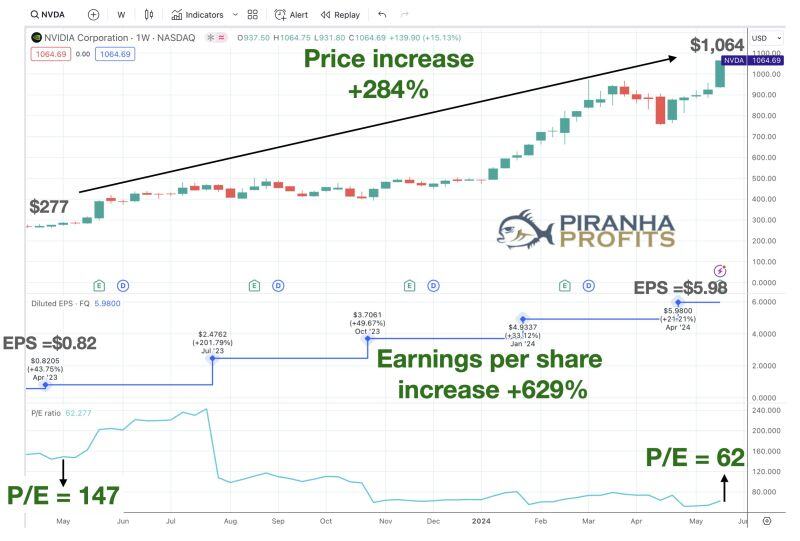

The higher a stock's price goes, the more expensive it gets. Right? Well, not always.

A year ago, when NVDA was selling at $277, its earnings per share was $0.82 and its P/E ratio was 147x Today, NVDA's share price is up +284% to $1,064.... BUT... Its earnings per share is up +629% to $5.98. Its P/E has fallen to 62x... forward P/E is now at 30x So, NVDA is CHEAPER today than it was a year ago. Source: Adam Khoo Trader, Piranha Profits

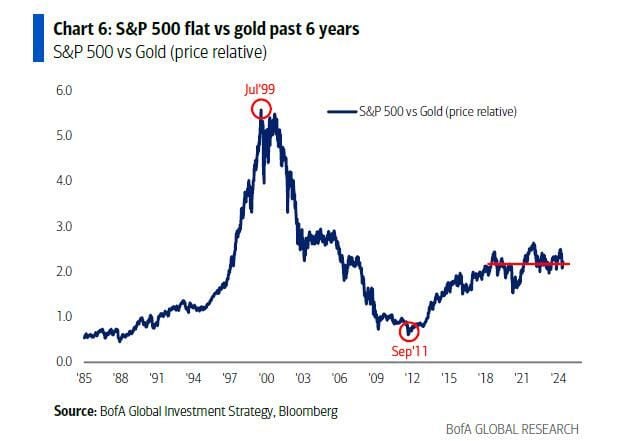

Did you know that the S&P 500 has been basically flat vs gold over the last six years? 🤔

Source: Markets & Mayhem, BofA

A key point on Nvidia story: $NVDA CEO Jensen Huang doesn't lack demand. What he lacks is supply.

In an exclusive interview following last week's earnings Huang said demand for its programs will soon outstrip supply, with the complexity of these chips also challenging the company's efforts to keep pace. Source: Yahoo Finance