Charlie Munger, Warren Buffett's Partner and 'Abominable No-Man,' dies at 99

Munger helped Buffett, who was seven years his junior, craft a philosophy of investing in companies for the long term. Under their management, Berkshire avg an annual gain of 20.1% from 1965 through 2021 — almost twice the pace of the S&P 500 Index. Source: Bloomberg, HolgerZ

Per Bloomberg, US Treasury issuance next year is expected to reach $1.9 trillion...

Excess supply of US Treasuries remains a key downside risk for bonds (and thus for equities given the still high correlation between the 2). Note that every Treasury auction is now very closely monitored by investors with some immediate consequences on market returns (e.g last week: strong auction triggered a drop in US Treasury yields on Wednesday and a rise in sp500). Source picture: Markets Mayhem

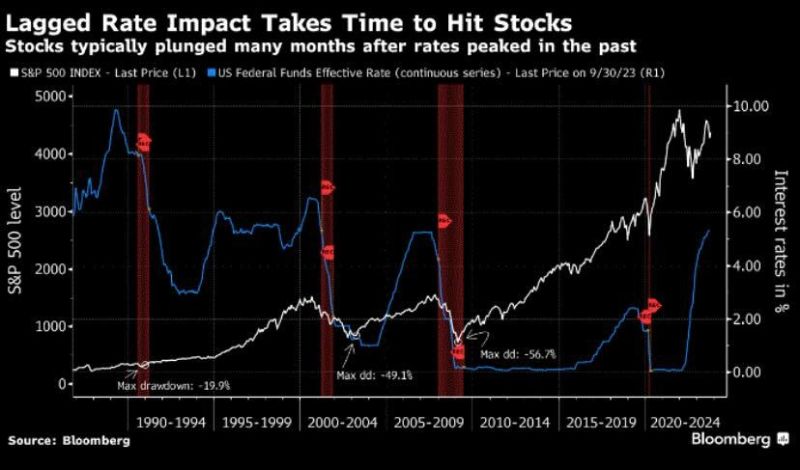

As we moved into 2024, one downside risk needs to be kept in mind:

tightening monetarypolicy cycle often operates with a lag. As shown on the chart below, stocks typically plunged many months after rates peaked in the past. Source. Bloomberg, Cheddar Flow

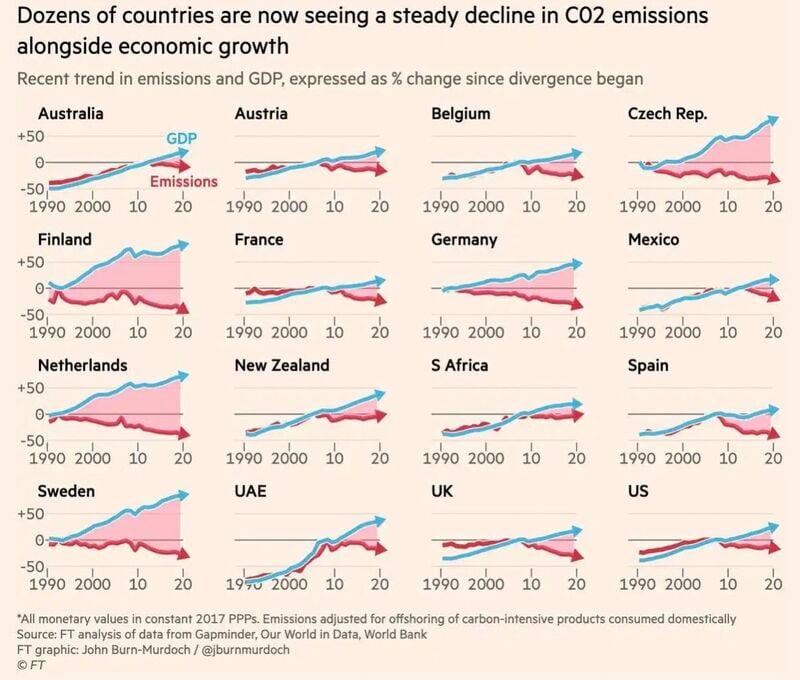

Dozen of countries are now seeing a steady decline in C02 emissions alongside economic growth

Another tangible proof that being green (or at least greener) does not mean de-growth Source: FT

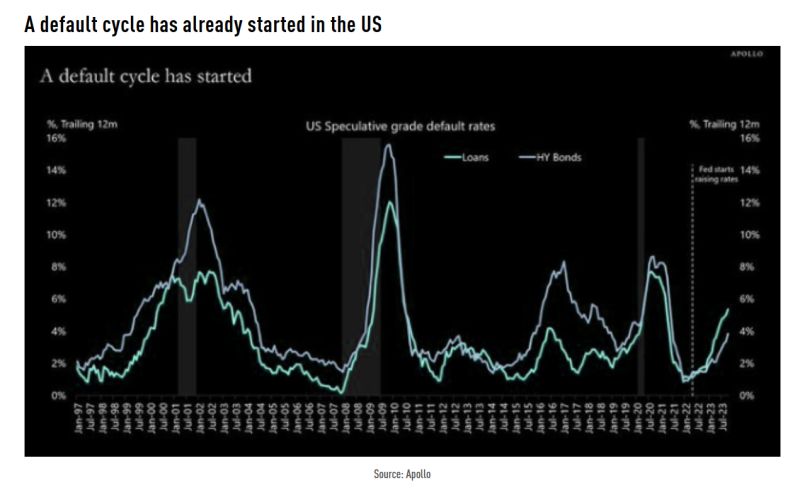

Since the Fed started raising rates in March 2022, default rates have gone from 1% to 5%+

Source: Apollo, TME

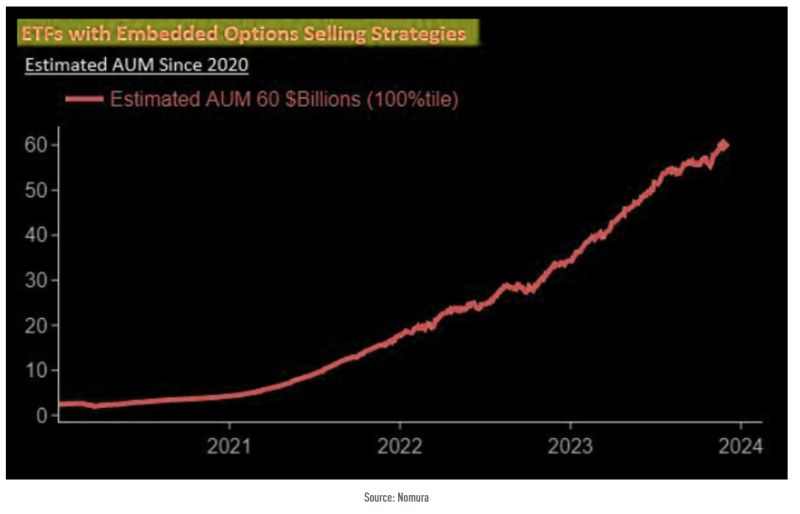

More and more capital going into the business of selling ETFs with embedded options selling features

Source: TME, Nomura

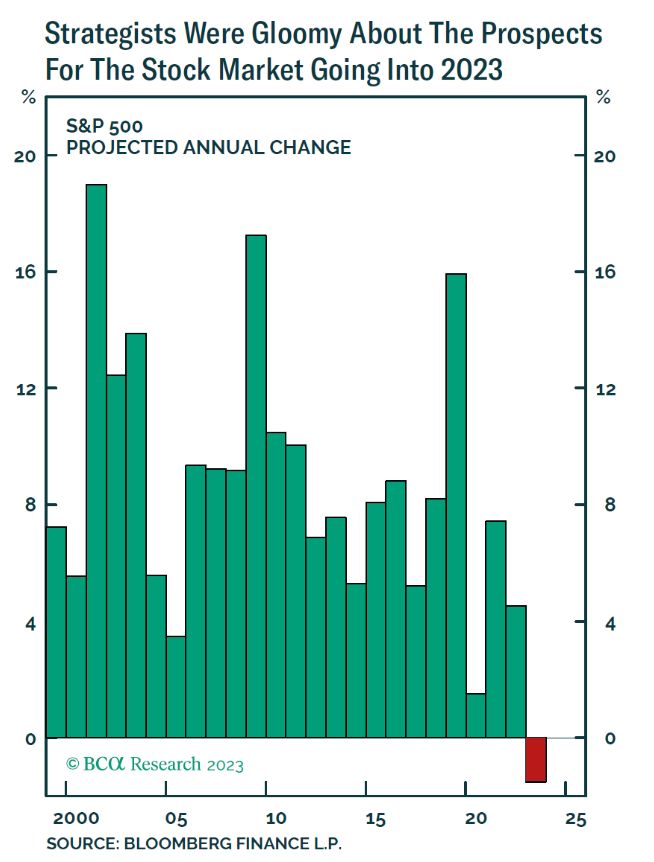

Here's a classical example of contrarian signal that can be used in your asset allocation decisions

Entering into 2023, Wall Street strategists were expecting the S&P 500 to decline. This was the first time ever (survey started in 2000) that aggregated 12-month S&P 500 targeted return was in negative territory. Fast forward to the end of November and the SP500 is up 18% year-to-date... As Warren Buffet said: "Be fearful when others are greedy and greedy when others are fearful" Source: BCA research, Barchart

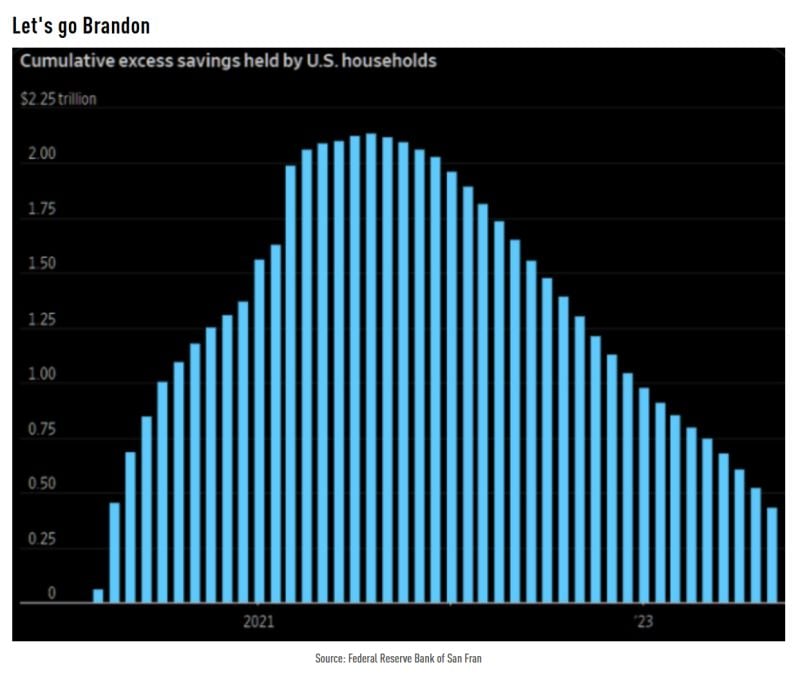

US households still have an estimated $433 billion in excess savings remaining from the 2020-21 stimulus programs

Source: TME