Berkshire Hathaway $BRK.A in danger of falling below its 200-day moving average for the first time since October 2023 🚨🚨🚨

Source: Barchart

Market cap:

Circle: $72 billion Coinbase: $78 billion Coinbase receives 50% of Circle's revenue. Source: Brew Markets @brewmarkets

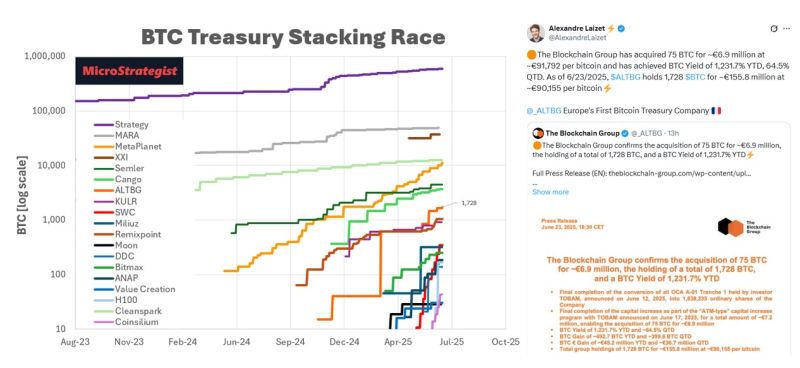

The bitcoin stacking race is raging!!!

In Europe, The Blockchain Group ALTBG continues snagging some regular BTC buys. They now own 1,728 $BTC for ~€155.8 million at ~€90,155 per bitcoin⚡️ Source: microstrategist on X, Alexandre Laizet, The Blockchain Group

Israel says ceasefire has been violated — Iran denies

The Israel Defense Forces have accused Iran of violating the ceasefire announced by U.S. President Donald Trump “In light of these severe violation of the ceasefire carried out by the Iranian regime, we will respond with force,” the IDF’s Chief of the General Staff Eyal Zamir said, according to a Telegram update from the Israeli military. Earlier, the IDF had reported it was working to intercept missiles launched by Iran toward Israel, with sirens blaring in the north of the Jewish state. News of Iran carrying out a missile attack against Israel after the ceasefire came into effect is “denied,” Reuters cites Iranian media as refuting. Source: CNBC

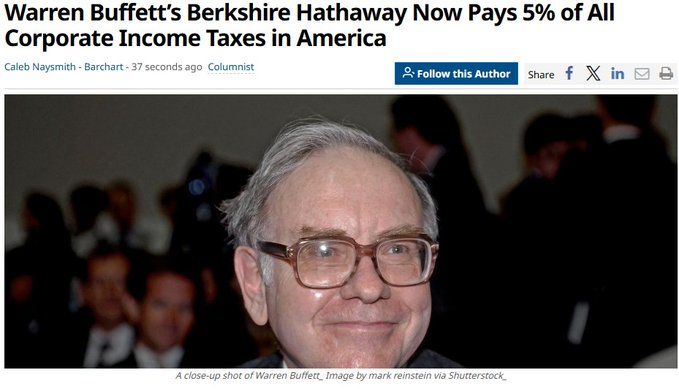

🤯Warren Buffett's Berkshire Hathaway Now Pays 5% of All U.S. Corporate Income Tax.

A 'record-shattering' $26.8 Billion: 🧵 Source: Caleb Naysmith @ccnaysmith

BREAKING: Crude Oil

Absolute Rug Pull in Crude Oil now plunging back below its 200D moving average tonight Source: Barchart

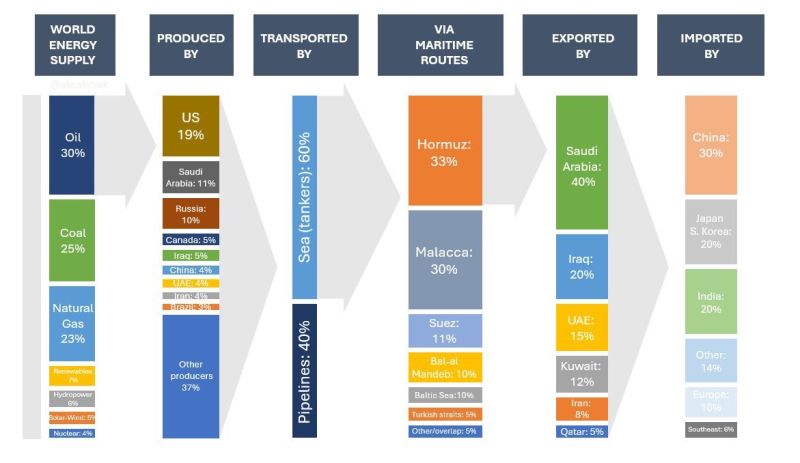

Oil Cheat Sheet.

Source: Menthor Q @MenthorQpro

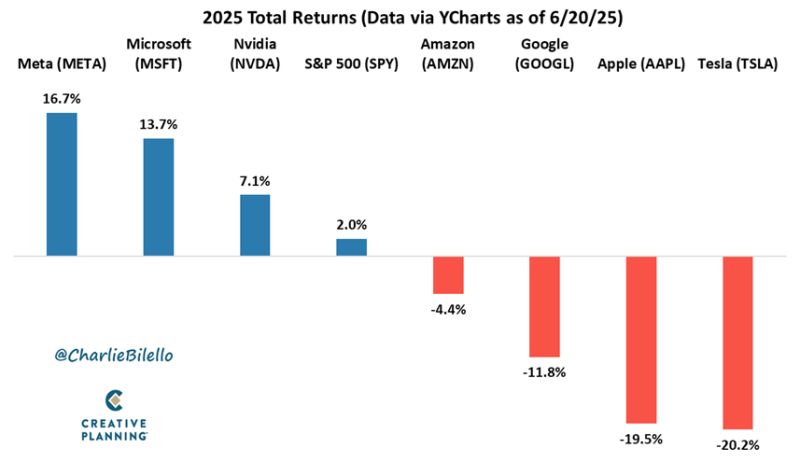

2025 so far:

The “Magnificent7” are no longer moving in lockstep like they did in 2023 & 2024: ✅ Meta +16.7% ✅Microsoft +13.7% ✅Nvidia +7.1% ❌Amazon -4.4% ❌Google -11.8% ❌Apple -19.5% ❌Tesla -20.2% Source: Charlie Bilello