Mind the gap...

France debt to GDP ratio ihas been diverging in a meaningful way vs. Germany debt to GDP. Rating agency Fitch already cut country's credit rating from AA to AA- last year, rating agency S&P has placed France under review... Source: Bloomberg, HolgerZ

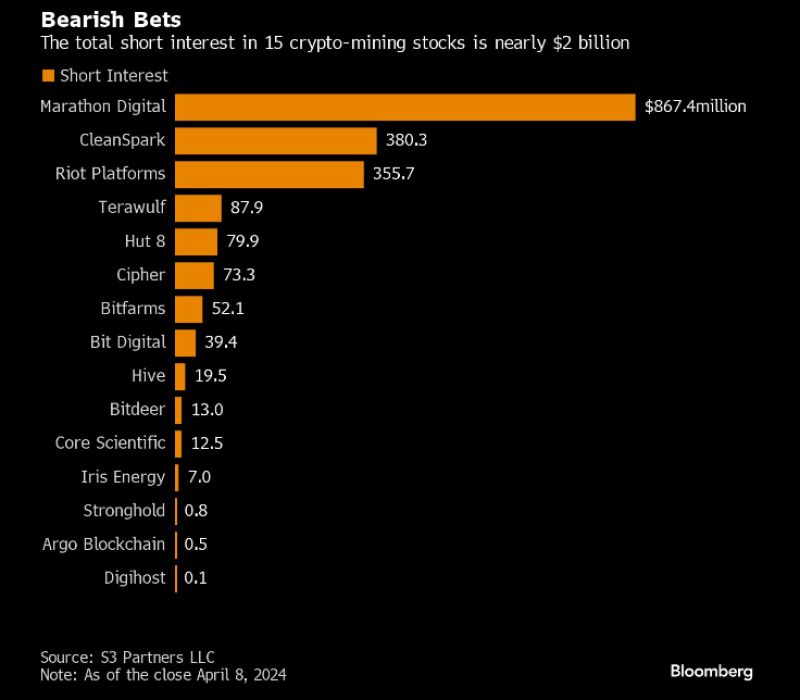

Bitcoin ‘halving’ will deal a $10bn blow to crypto miners.

Cryptocurrency’s update will slash new supply in late April. Competition for favourable electric rates is growing from AI firms. Some traders are thus betting that mining stocks will fall. Total short interest, dollar value of shares borrowed & sold by bearish traders, stood at ~$2bn. Source: HolgerZ, Bloomberg

CBOE Volatility Index $VIX surges to highest level of fear since Halloween 👻🎃

Source: Barchart

According to Alfonso Peccatiello, a $1 trillion worth liquidity wave is about to be unleashed on the US economy!

He is not talking about Powell or the Fed. He is talking about Treasury Secretary Yellen unleashing a large sum of stimulus further boosting the US economy right before elections! How? By almost emptying a $1 trillion+ Treasury General Account!

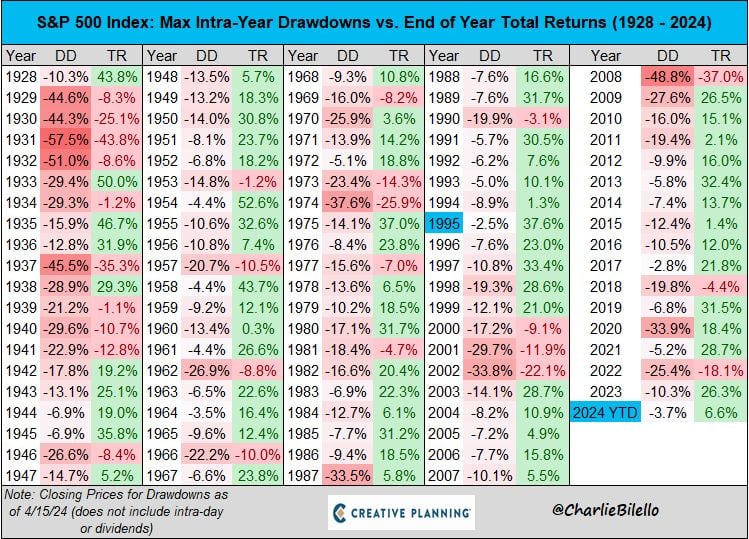

The S&P 500 is only down 3.7% from its peak closing price at the end of March.

The median intra-year drawdown since 1928 is -13%. What were seeing today is normal volatility - the first 3 months of the year were abnormally smooth. Source: Charlie Bilello

China’s economy in the first quarter grew faster than expected, official data released Tuesday by China’s National Bureau of Statistics showed.

Gross domestic product in the January to March period grew 5.3% compared to a year ago, faster than the 4.6% growth expected by economists polled by Reuters, and compared to the 5.2% expansion in the fourth quarter of 2023. On a quarter-on-quarter basis, China’s GDP grew 1.6% in the first quarter, compared to a Reuters poll expectations of 1.4% and a revised fourth quarter expansion of 1.2%. Beijing has set a 2024 growth target of around 5%. https://lnkd.in/eNZgs7zp Source: CNBC

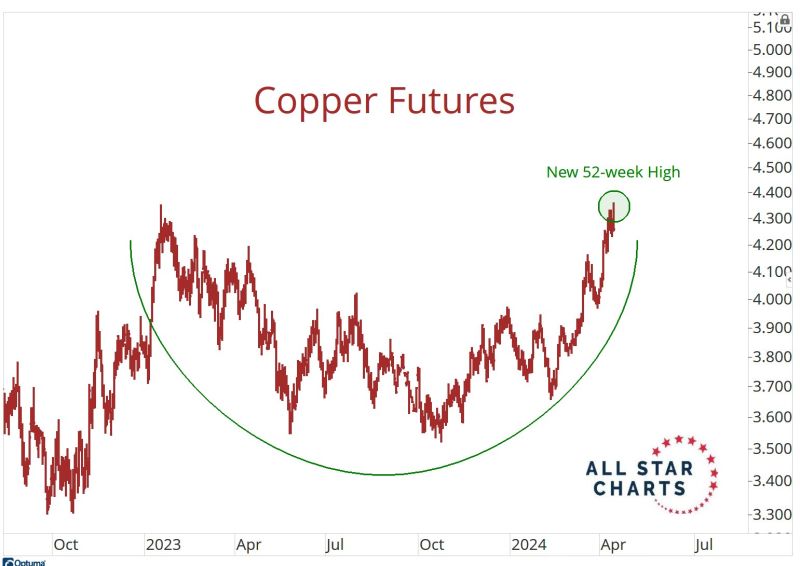

It's not just a Gold thing. It's a metals thing.

Copper hitting new 52-week highs. Source: J-C Parets

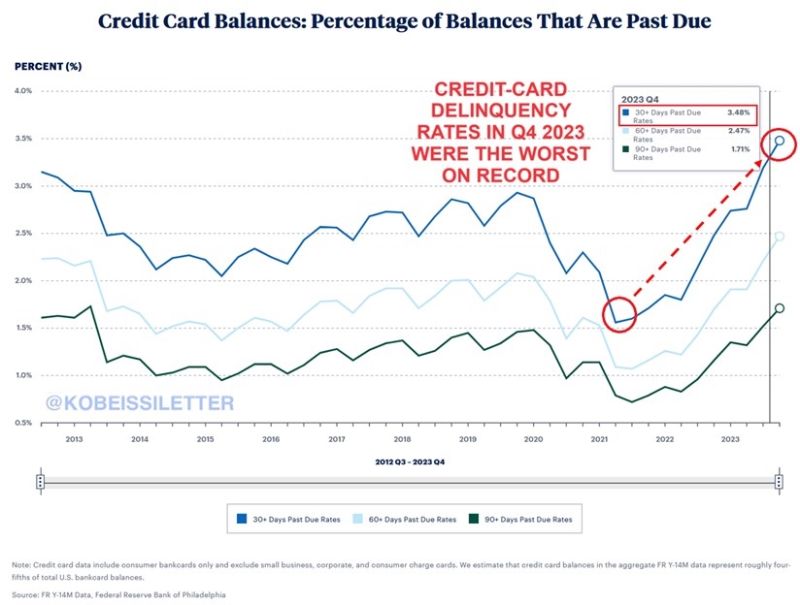

US credit card delinquency rates are now at their highest on record, according to the Philadelphia Fed.

In Q4 2023, more credit card balances were 30+ and 60+ days past due compared to any other period in history. The percentage of credit card balances at least 30 days past due is now ~3.5%. Meanwhile, total credit card debt has skyrocketed in recent months and is now at a record $1.3 trillion. The average credit card interest rate is also at record 28%, according to Forbes. Source: The Kobeissi Letter