Money-market fund assets rose to a fresh record high on expectations short-term rates will remain elevated for longer.

Total assets rose to $6.108tn from $6.077tn the week prior. Source: HolgerZ, Bloomberg

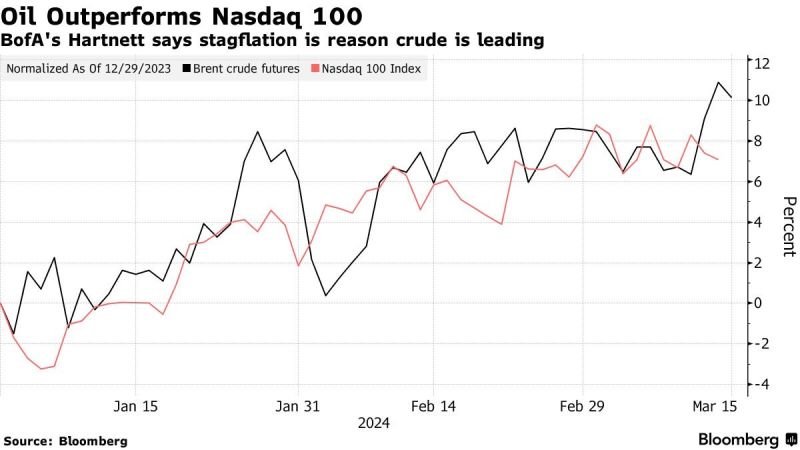

Believe it or not oil is outperforming the NASDAQ this year

Source: Bloomberg

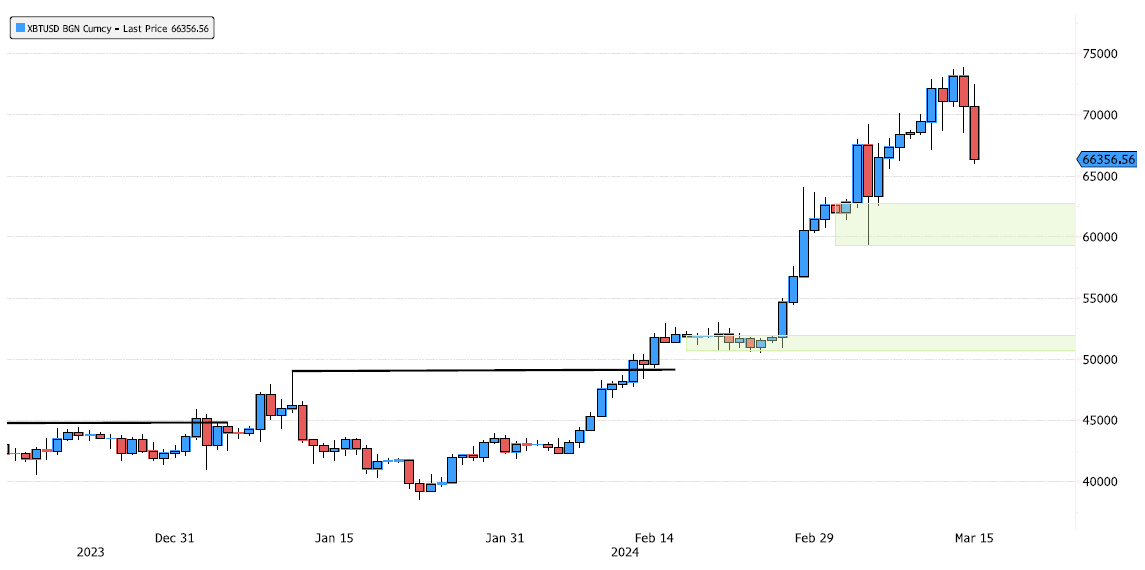

Bitcoin next support level ?

Bitcoin (XBTUSD) consolidating (down 6% now). Keep an eye on next support zone that seems interesting 59'317-62'750. Source : Bloomberg

Crude Oil confirming short term bullish trend

Crude Oil WTI confirmed yesterday it's short term bullish trend by closing over 79.77. Swing low support is at 76.79. Source : Bloomberg

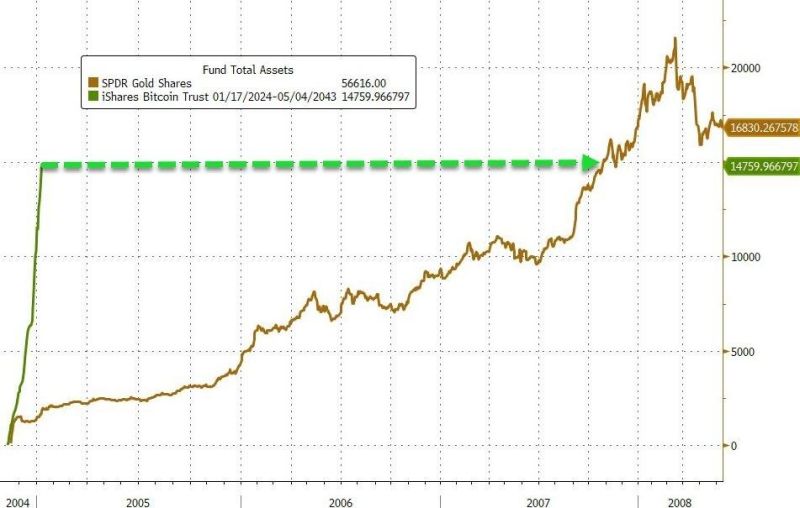

It took the iShares Bitcoin ETF, $IBIT, 8 weeks to hit $15 billion in assets under management.

By comparison, it took the Gold ETF, $GLD, 3 years to hit $15 billion in assets under management, per Zerohedge. At this pace, $IBIT could overtake $GLD in a matter of days...

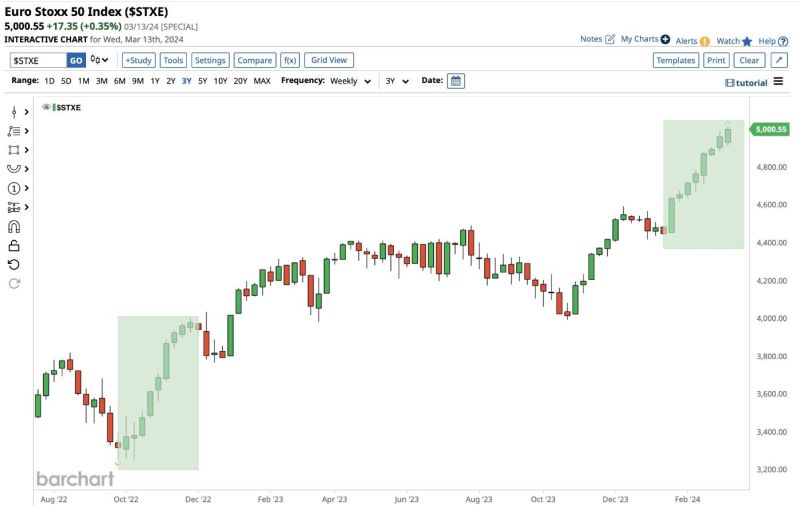

European Stocks are on track for their 8th consecutive green week which would be their longest winning streak since 2022

source : barchart

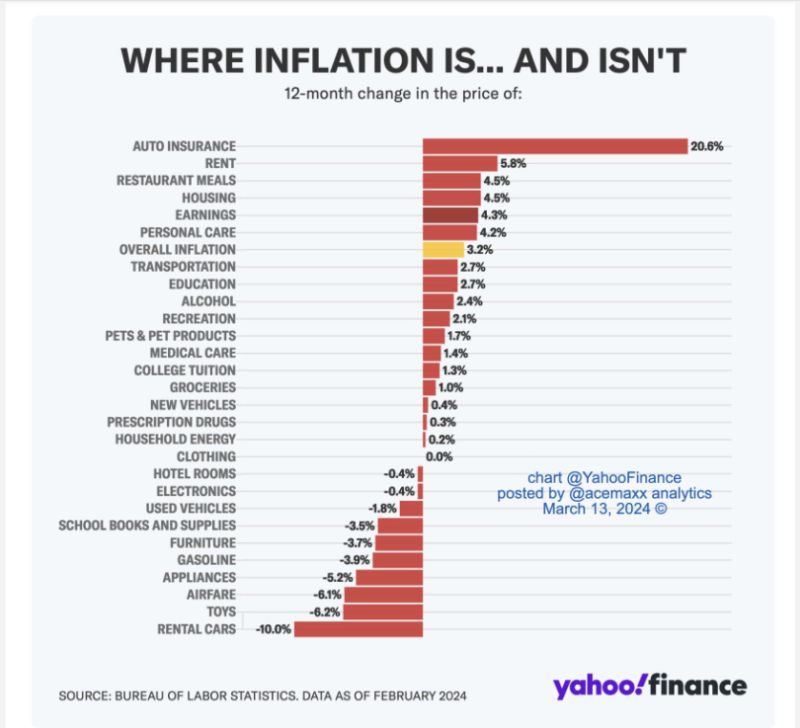

Where Inflation Is... and Isn't ...

source : yahoofinance, acemaxx

Japanese companies boost wages in departure from 'lost decades'

Japan's largest employers announced record pay increases on Wednesday. Every spring, unions and management hold talks, known as shunto, to set monthly wages ahead of the start of Japan's fiscal year in April. Toyota Motor, Hitachi and Panasonic Holdings were among the companies that on Wednesday fully met labor unions' demands to raise wages. Nippon Steel's response exceeded the union's demands, raising monthly wages by a record 35,000 yen ($237), or 14%. Toyota did not disclose details of its wage increases but said it fully met union demands. The Toyota Motor Workers' Union has demanded a record bonus payment worth 7.6 months of salary, citing the company's all-time high annual operating profit forecast of 4.5 trillion yen for the current fiscal year. The union has also proposed specific demands for each job category, up to a 28,440 yen monthly wage increase. Hitachi and Toshiba said their pay hikes are the largest since the current negotiation style was introduced in 1998. According to the Japan Council of Metalworkers' Unions (JCM), an alliance of unions in the manufacturing industry, 87.5% of member organizations had their demands either fully met or exceeded. source : nikkeiasia