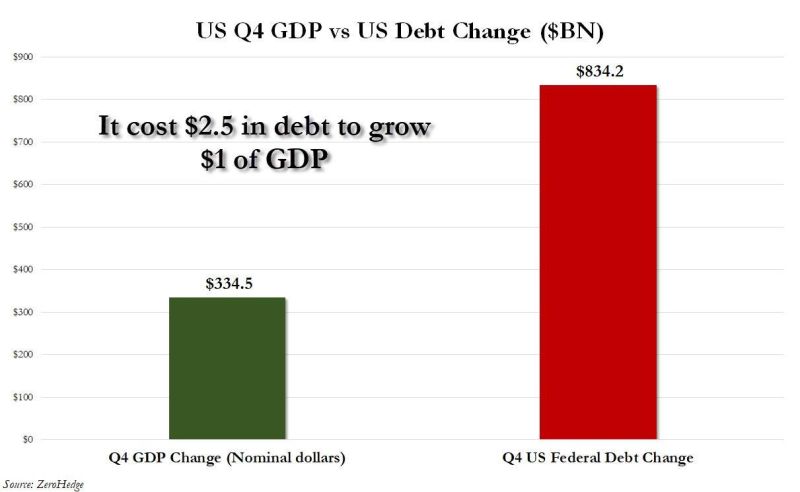

When you invest in US debt, think twice...

In Q4 2023, nominal GDP grew by 3.2% according to data on Wednesday. This would mean a $334.5 billion increase in nominal GDP. Meanwhile, over the same time period the US added $834.2 billion of debt. In other words, it cost us $2.50 of debt for every $1.00 of GDP last quarter, according to Zerohedge. As Fed Chair Powell recently said, "we are on an unsustainable fiscal path." What's the long term plan here? Source: The Kobeissi Letter, www.zerohedge.com

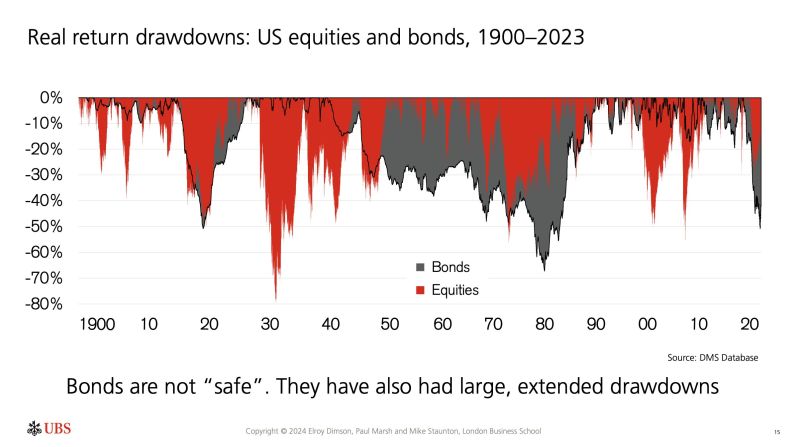

Bonds are “safe”?

Think again, they have also had large, extended drawdowns, UBS Yearbook shows.

Buffett's longest held stocks:

$KO - 34 years $AXP - 29 years $MCO - 22 years $GLBE - 22 years $PG - 18 years He has returned 20% CAGR since 1965. Source: The Investing for Beginners Podcast

Coinbase suffered a glitch on Wednesday that left many users seeing a zero balance in their account.

The Coinbase crash just erased $100 BILLION of market cap in Bitcoin in 15 minutes. Between 12:15 PM ET and 12:30 PM ET, Bitcoin fell from $64,000 to $59,000. This was a near 9% swing in 15 minutes right as many Coinbase users began showing a $0 balance in their account. It also happened to occur just as Bitcoin was less than 10% away from a new all time high. Coinbase is reportedly still working on fixing the issue. Source: The Kobeissi Letter

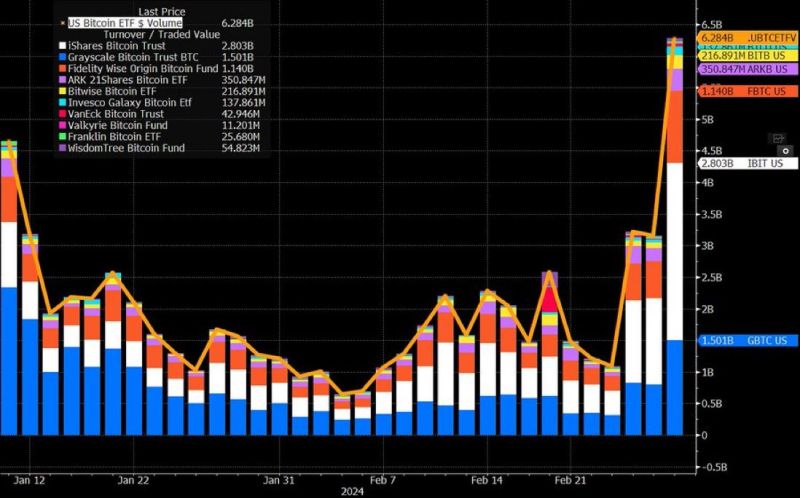

Bitcoin ETFs have smashed their daily trading volume record with $6.28 billion so far.

More than double the previous record of $3b. Source: JSeyff, Bitcoin archive

Mag 7 market cap is higher than India & Japan listed equities combined

Source: r/IndianStreetBets on Reddit

BREAKING: Bitcoin prices rise above the key $60,000 resistance level for the first time since November 2021

amid surging optimism that demand for the token is widening beyond committed digital-asset enthusiasts. iShares Bitcoin ETF manages >$8bn in assets after one and a half months. Over the past 24 hours, Bitcoin has surged by an impressive 7%, with a weekly gain of almost 20% and a staggering 160% increase over the last 12 months. So what's driving this remarkable rally? 1/ The recent spike in Bitcoin's price can be attributed to a significant increase in institutional interest, following the approval of 11 Bitcoin exchange-traded funds (ETFs) in the US earlier this year. This development has opened the floodgates for institutional investors, who are now entering into the crypto space. Bitcoin is obviously their choice number 1 2/ Adding fuel to the fire is the highly anticipated Bitcoin halving event, scheduled for April this year. Historically, halvings have triggered massive bull runs, as the mining rewards are cut in half, effectively reducing the inflation rate of new Bitcoin supply by 50%. 3/ Hedge funds are anticipating a massive demand-supply squeeze due to the combination of ETF-led demand and the halving. Some numbers to keep in mind (as of the end of last week): - 272,000 Bitcoin were bought in the last 28 days by ETFs. Meanwhile only 25,200 $BTC were mined! Yes, GBTC (Grayscale Bitcoin Trust) outflows are still a concern, but at some point that will have to end. - Assuming this number stays consistent (or possibly even increases) with roughly ~2 million BTC on exchanges (based on today's liquidity), that would mean that in about 8 months time there would literally be ZERO BTC available for sale!!! - And not mention the halving in 3 months will cut this amount to just 12,600 BTC mined in the same amount of time. 4/ Retail investors are now joining the party. They have been initially shy to follow the positive momentum but as the BTC keeps moving up they are starting to speculate on all-time-highs to be soon be revisited. From a technical analysis point of view, the all-time high of $67,757 is the next resistance. As a final note: Bitcoin is testing all-time highs before the halving. This has NEVER happened before in history Source chart: Rizzo

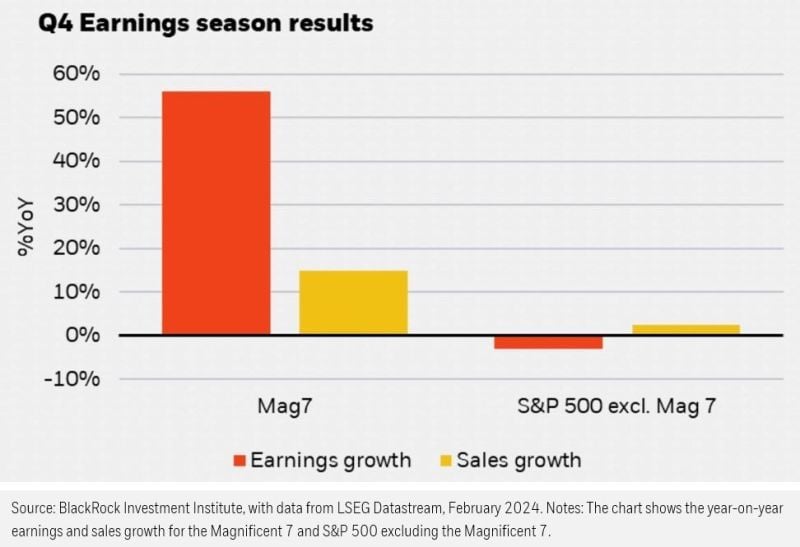

Market concentration mirroring earnings concentration

Source: Blackrock