Volatility in US Investment Grade Corporate Bond Market Hits All-Time Low!

📉 Trend Alert: The 1-month volatility of the CDX North America Investment Grade index, a basket of 125 equally weighted credit default swaps on investment-grade issuers, has dropped to its lowest level since the index was launched in 2012. 📊 What’s Driving This Trend? Resilient Economy: The US economy is demonstrating strong resilience, which supports narrower credit spreads. Stable Equities: Low volatility in the US equity markets indicates investor confidence, further stabilizing the bond market. Strong Corporate Health: Robust fundamentals of US companies are contributing to lower credit risk perceptions. 📈 Interest Rates & Credit Spreads: Negative Correlation: There's a current negative correlation between US interest rates and credit spreads. This means that as interest rates rise, credit spreads tend to narrow, and vice versa. Positive Impact: This trend has led to US corporate bonds significantly outperforming US Treasuries, marking the biggest relative outperformance since the pandemic crisis in March 2020. ❓ Future Considerations: How long can we expect this low volatility and narrow spreads to continue? Watch the credit market closely for any signs of weakness. Source: Bloomberg

🚀 Chart of the Week: Japan's Yield Curve is Steepening Again! 📈

Big moves in the Japanese bond market! The Japanese yield curve, which tracks the difference between 2-year and 10-year yields, has dramatically steepened since late March and surged even more in May. It's now at 63 bps, a level we haven't seen since January! 📊 10-year and 30-year Japanese yields are hitting decade highs, approaching 1% and surpassing 2%, respectively. As the Yen weakens, the Bank of Japan stepped in to support the JPY and recently cut its bond-buying program for the first time this year. What’s next? The BOJ might sell off its US Treasuries holdings, potentially driving US Treasury yields up in the coming months. Higher Japanese yields also mean US Treasuries are less attractive to Japanese investors, who are key players in the US market. Last summer, a sharp steepening of the Japanese yield curve coincided with a major sell-off in US Treasuries...🤔 #Finance #Investing #Bonds #JapaneseEconomy #GlobalMarkets #Economics #Investors #FinancialMarkets #BankofJapan #USTreasuries Source: Bloomberg

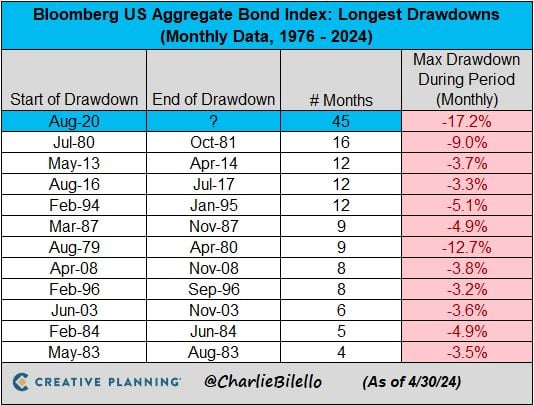

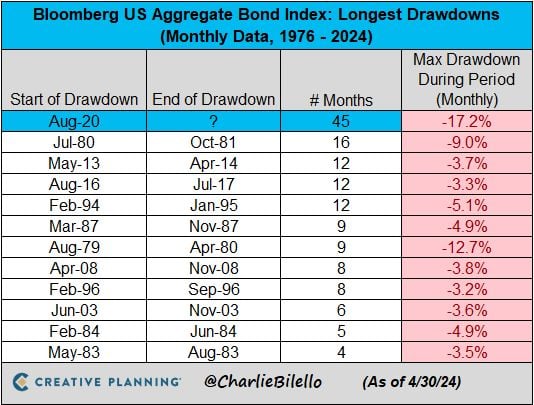

The US Bond Market has now been in a drawdown for 45 months, by far the longest bond bear market in history

Source: Charlie Bilello

The US Bond Market has now been in a drawdown for 45 months, by far the longest bond bear market in history.

Source: Charlie Bilello

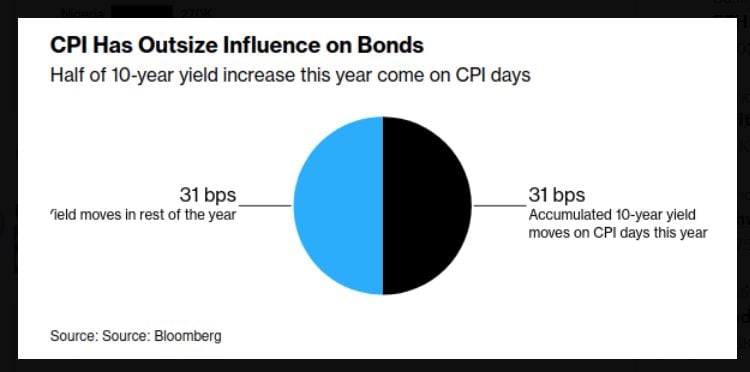

Ahead of US CPI, it's important to note that the data point tends to weigh heavily on bond yields -- up or down.

Source: Bloomberg, Markets & Mayhem

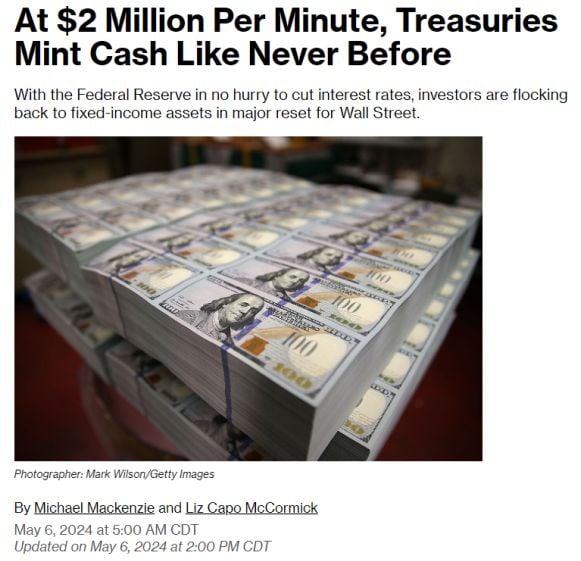

BREAKING 🚨: U.S. Treasury

U.S. Treasuries are now paying out $2 million per minute! Source: Barchart

Great observation by Dr. Michael Stamos, CFA - Head of Global Research & Development of Global Multi Asset Department at Allianz Global Investors

-> "On days when bonds were up, stocks tended to go up as well. When bonds fell, stocks managed to stay at least flat. Overall it was a pretty nice environment for equity investors. Lets hope this doesn't turn into a high-correlation-when-markets-are-down type of environment".

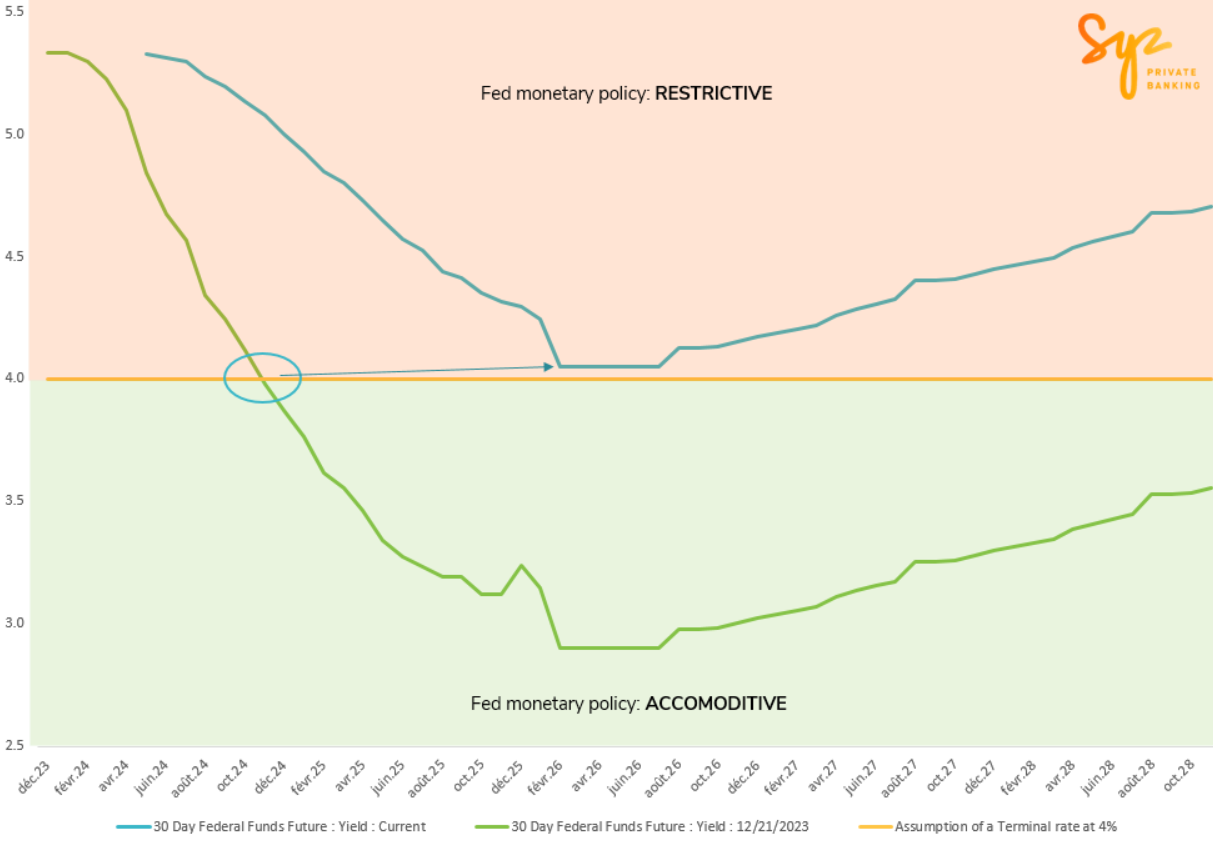

'Higher for Longer' — The Fed Fund Future Market Takes Heed!

The market has notably adjusted its expectations for the Federal Reserve's monetary policy over the coming years. Initially, an aggressive trajectory toward a terminal rate of around 3% was projected at the start of the year, indicating a return to a Neutral rate adjusted for inflation. However, current forecasts now suggest a more cautious normalization, with a significantly higher terminal rate of 4%. Intriguingly, the market anticipates further tightening by mid-2026, which some analysts believe could echo the inflation resurgence patterns of the 1970s. The Neutral rate (R*), long considered to be around 0.5%, is now hotly debated and estimated to be between 1.5% and 2.0% in the United States. The Fed Funds Futures market appears to have already factored in the impacts of enduring fiscal deficits, improved productivity, and deglobalization trends. How will these elements continue to influence Fed policy amid shifting global economic dynamics? Source: Bloomberg