Stocks, bonds and cryptos rally following soft US jobs data.

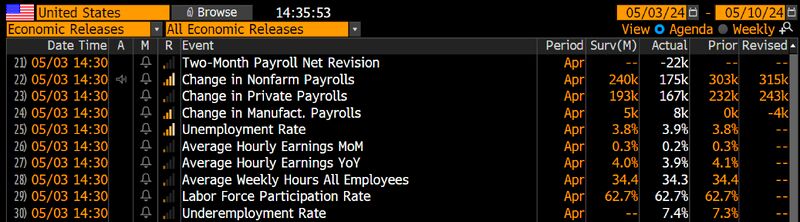

Hiring slows to 175,000 jobs in April way below the forecasted 240k. This is the lowest figure since Oct 2023’s +165k. Household survey came in below forecasts as well with unemployment rate rising to 3.9% from March's 3.8%. Wage growth slows to 0.2% MoM vs 0.3% expected. Note that 0.2% is consistent with 2% inflation. Source: Bloomberg, HolgerZ

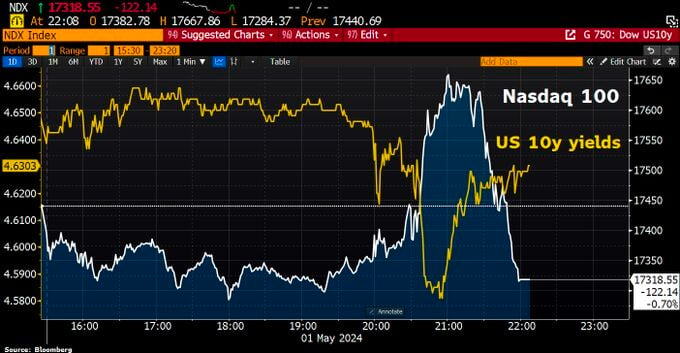

The gains in equities & bonds during the Fed meeting were completely wiped out by the market by the end.

Nasdaq 100 closed 0.7% lower, and US 10y yields pared most of their drop. Source: HolgerZ, Bloomberg

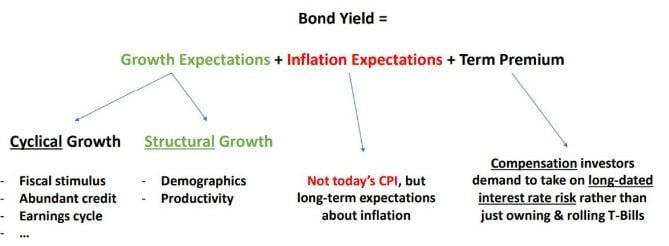

Bond Market 101: a useful way to think about bond yields by Alfonso Peccatiello.

Nominal bond yields can be thought of as the interaction between: 1️⃣ Growth expectations 2️⃣ Inflation expectations 3️⃣ Term premium

In case you missed it: 2-Year Treasury Yield jumps above 5% to its highest level since November 10

Source: Barchart

What's going on here?

Source: Bloomberg, Lawrence McDonald

One of the most important chart in the asset allocation decision process:

Stocks vs. long duration US Treasuries. The trend is your friend Source: J-C Parets

To the moon!!! US Treasury boosts April-June borrowing estimates to $243b from $202b.

US reiterates a cash-balance estimate of $750bn for the end of June. US Treasury cites lower cash receipts for bigger borrowing estimates. No Mrs Yellen, this is not virtual reality... (picture stollen to Jim Bianco)

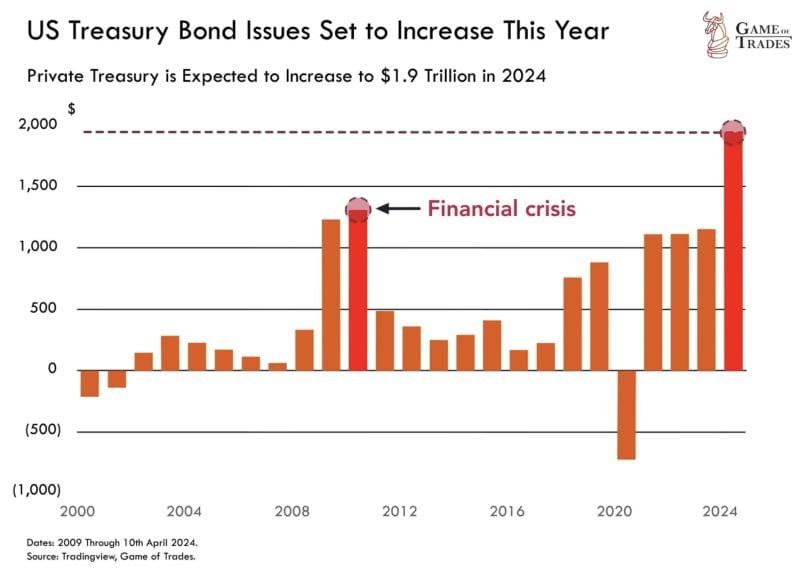

Treasury bond issuance in 2024 is expected to hit $1.9 TRILLION.

Surpassing levels seen even during the 2008 financial crisis and 2x 2023 levels. Source: Game of Trades