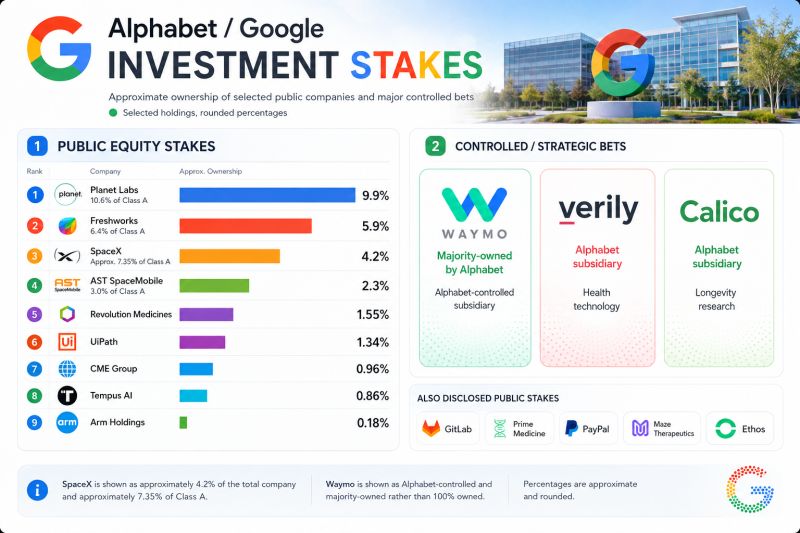

Google's investment portfolio:

Source: Patient Investor

Alphabet $GOOGL closed below its 200-day moving average for the first time in over a year

Source: Barchart

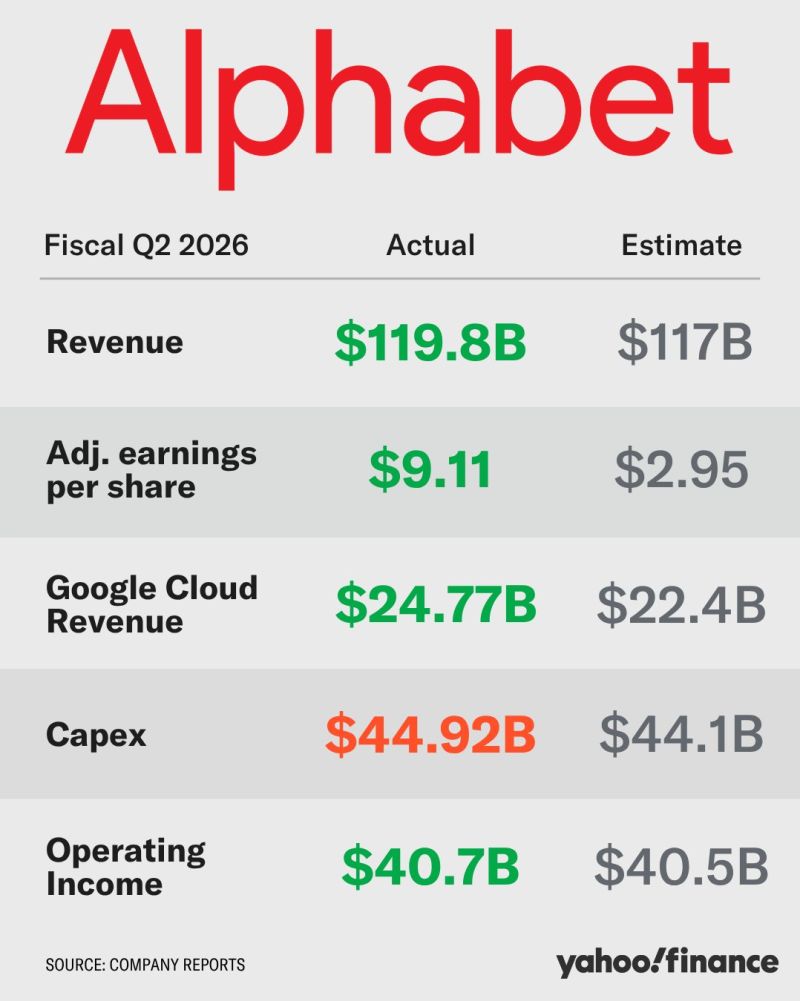

Alphabet beat Q2 revenue expectations, but missed on underlying earnings.

Revenue rose 24% to $119.8 billion, led by an 82% increase in Google Cloud revenue to $24.8 billion. Cloud operating margin reached 36%. Reported net income was boosted by roughly $99 billion in unrealised gains on investments including Anthropic and SpaceX. Excluding these gains, adjusted EPS was $2.85 versus $2.90 expected. The stock fell 3% after hours. Source: App Economy Insights @EconomyApp Bull Theory Yahoo Finance

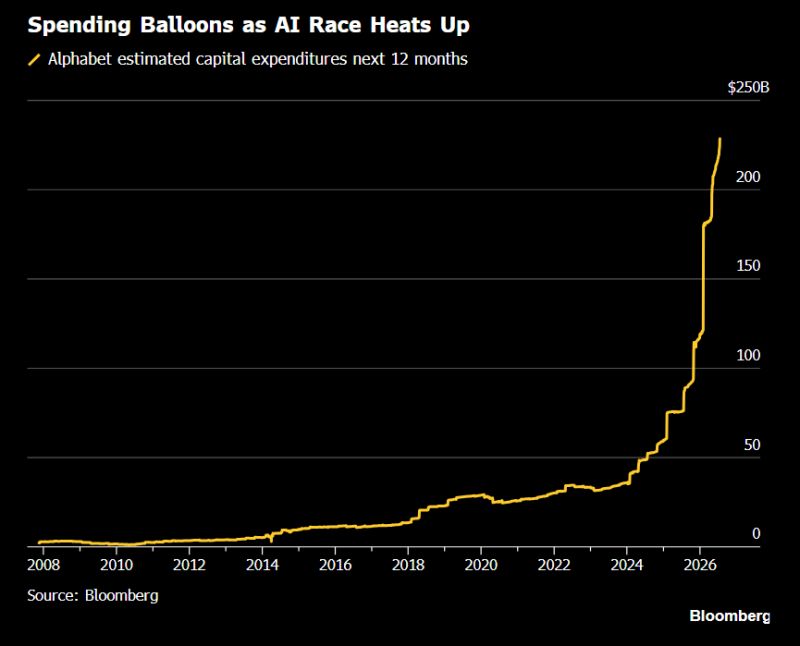

Google's capex is on track to nearly triple in two years

Source: Hedgeye @Hedgeye Bloomberg

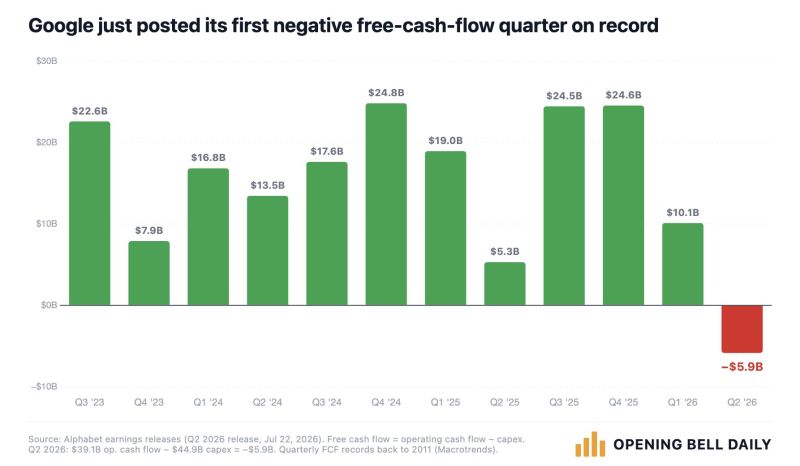

Alphabet $GOOG just reported NEGATIVE free cash flow for the first time in history.

And the story is not over; Alphabet projected full-year capital expenditures will be $195 billion to $205 billion in 2026, increasing its already sky-high spending estimate for the year as it works to secure an edge in the AI race. Source: Phil Rosen @philrosenn

Andy Bechtolsheim wrote Google a $100,000 check before it even had a bank account.

That $100,000 check is worth $15 billion today. Andy Bechtolsheim is a billionaire German-American electrical engineer, investor, and tech entrepreneur. He co-founded Sun Microsystems in 1982 and Arista Networks in 2004. Source: Bull Theory

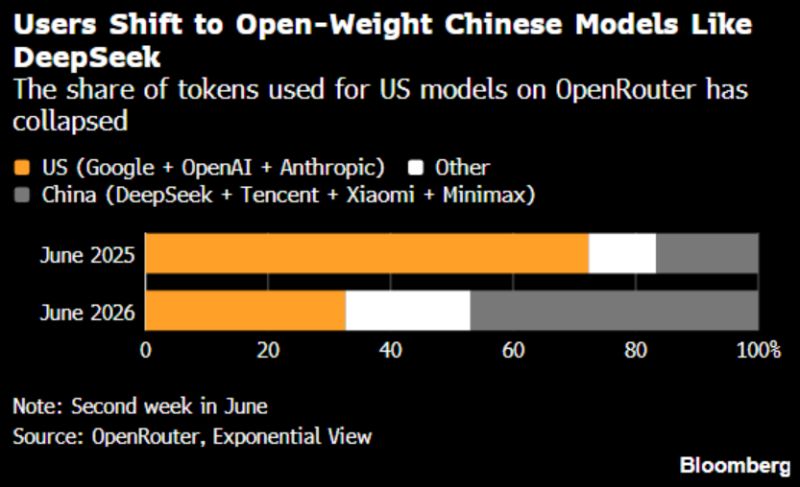

Tokens requested from Google, OpenAI and Anthropic relative to total fell to 33% in June 2026 from 72% a year earlier.

Tokenomics matters, or at least it will soon enough. Chinese AI’s gains in the market are remarkable. Source: Bloomberg, Negligible Capital

ALPHABET $GOOGL MANDATORY CONVERTIBLE STOCK SALE IS SAID TO BE OVERSUBSCRIBED

ALPHABET $GOOGL MANDATORY CONVERTIBLE STOCK SALE IS SAID TO BE OVERSUBSCRIBED Source: Wall St Engine