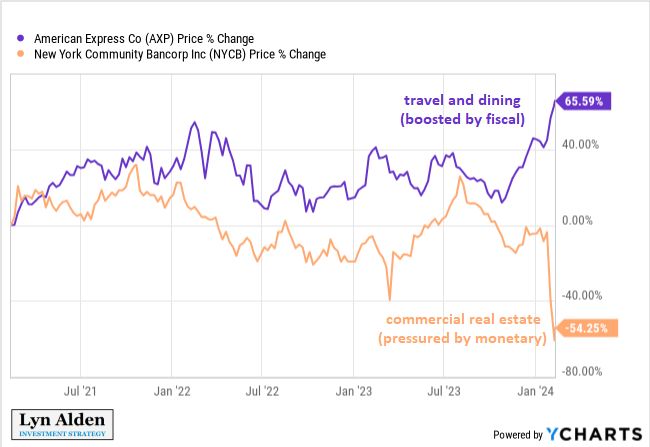

Great comment by Lyn Alden about the impact "FISCAL DOMINANCE" on sector performance divergence...

Bottom-line: go LONG Fiscal deficits receivers and go SHORT Fiscal deficit payers (i.e interest-rate sensitive sectors) "The wider-than-normal divergence between loose fiscal policy (which is stimulating) and tight monetary policy (which slows things down) contributes to wider-than-normal divergence between the performance of different economic sectors. It results in a wider-than-normal gap between sectors that are directly or indirectly on the receiving side of the deficits (eg business that rely on spending from upper and upper-middle class spenders) vs those that are the most sensitive to interest rates and thus are the most hurt by tight monetary policy (eg commercial real estate). And because some sectors of the economy are doing great partially due to the fiscal stimulus, it makes it unlikely that monetary policy or other assistance will arrive to the weaker areas any time soon. And ironically, because public debt levels are high, tight monetary policy *contributes* to looser fiscal policy by increasing the overall interest expense of the government, which goes to various entities in the economy and strengthens some of the sectors that are not sensitive to interest rates. This is a condition known as fiscal dominance". Lyn Alden

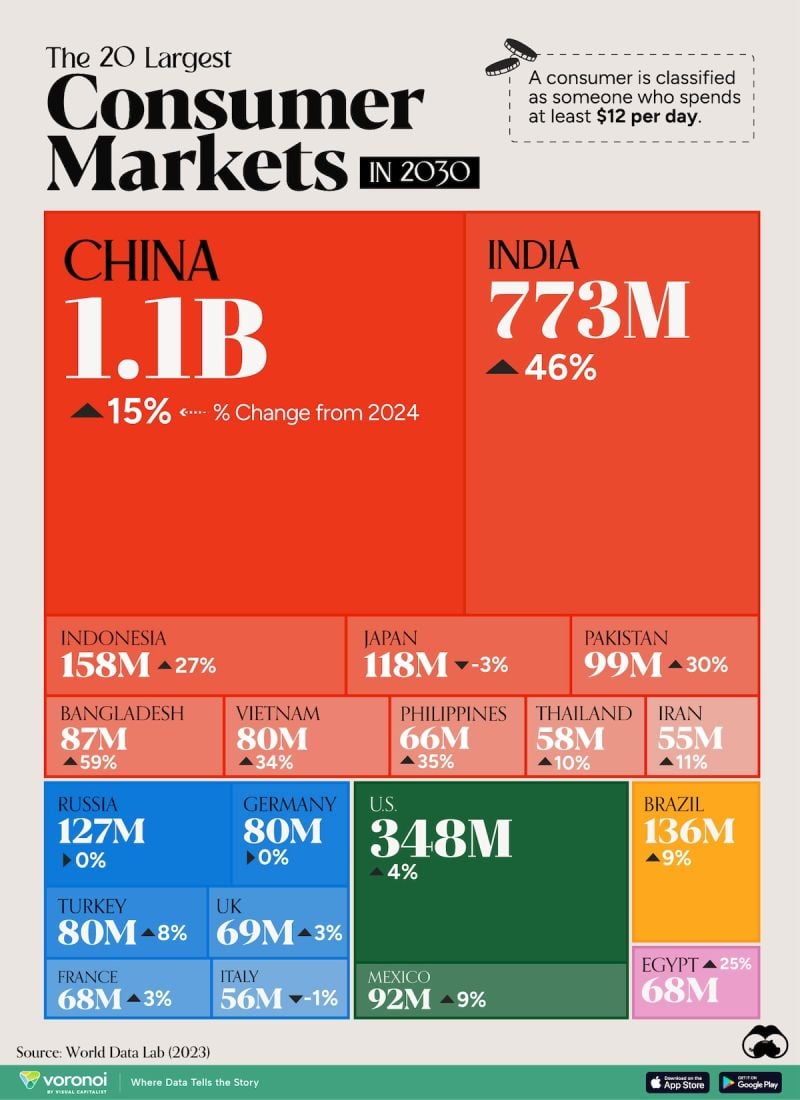

The World’s Largest Consumer Markets in 2030 🌏

Source: Visual Capitalist

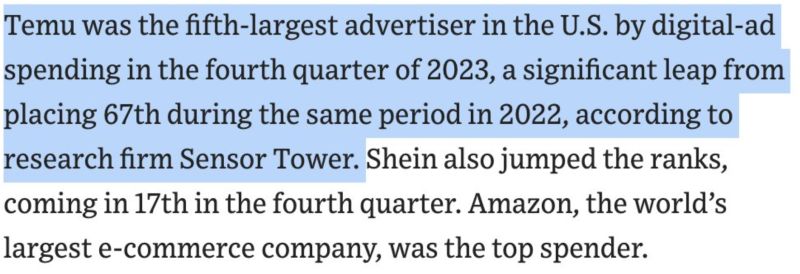

The Spend, Spend, Spend Strategy..

Temu is going all in on Marketing (including in this Sunday’s Super Bowl) Marketing spend: • 2023 - $1.7 billion • 2024 - $3 billion (est.) source : wsj

Has the fed won the party?

US Medium-Term Inflation Expectations Lowest in 11 Years of Data – Source: Bloomberg

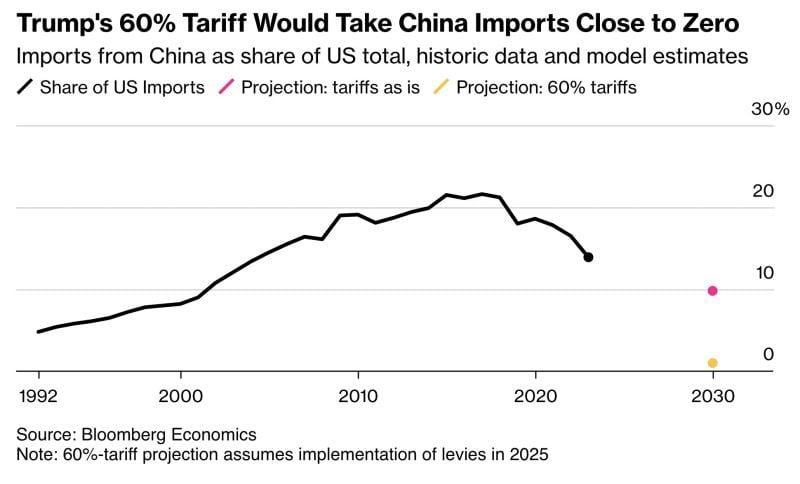

Donald Trump is pitching a 60% tariff on all Chinese imports.

That would shrink a $575bn trade pipeline to practically nothing, Bloomberg analysis shows. For China ’s economy and its slumping stockmarket — down >40% from its 2021 high — that’s bad news. Worse, Trump’s rhetoric may add pressure on Biden to take harsher measures in the run-up to election day Source: HolgerZ, Bloomberg

Jamie Dimon believes U.S. debt is the ‘most predictable crisis’ in history

And experts say it could cost Americans their homes, spending power and national security - Fortune Source: Markets & Mayhem

“Super Sick Monday"

16.1 million U.S. employees will be completely absent from work today following Super Bowl Sunday, according to this year’s research from UKG. In 2023, nearly 18.8 million employees said they planned on missing work on Super Bowl Monday. However, 6.4 million further employees plan to come to work late, another 11.2 million are unsure of whether they will come to work, and around 6.4 million will decide what to do on the day. The number jumps up for U.S. employees who plan to miss at least some work on Monday, reaching around 22.5 million employees – 14% of the U.S. workforce. The research also finds six million employees have not yet notified their employers and will call in sick on the day or simply ‘ghost’ their employer on Monday. source : The Harris Pol, UKG Workforce Institute

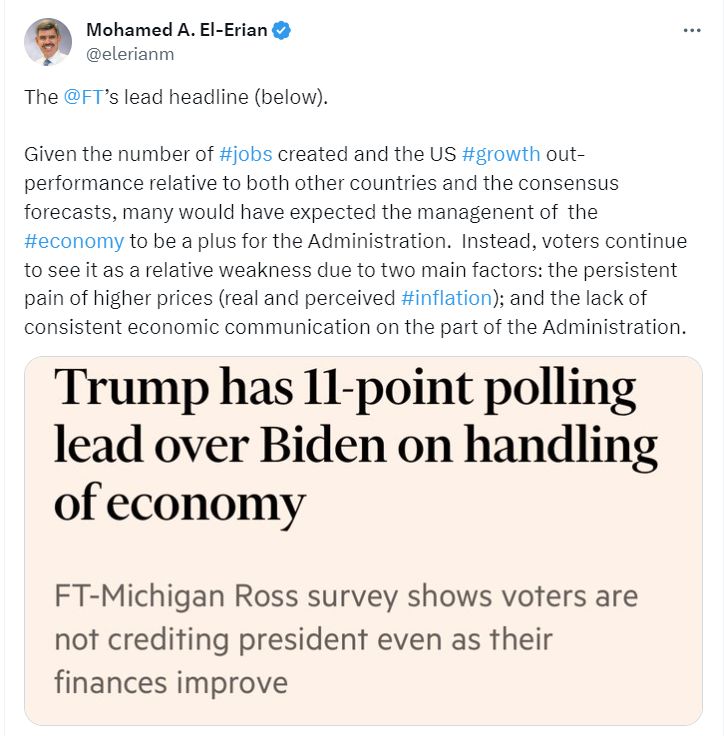

In an US election year, the spread between “Job Creation” and job “approval rating on the economy” has NEVER been wider...

Source: Mohamed A. El-Erian