The US is facing a "death spiral" as a result of its mounting debt and the inability of politicians to confront the issue, according to "The Black Swan" author Nassim Taleb.

Per Bloomberg, the Universa Investments advisor who correctly called the 2008 financial crash cast a dire warning about the US debt situation, which has seen the federal debt balance notch $34 trillion for the first time ever to start the year. As long as Congress keeps up its rapid pace of spending, those debts are going to continue to pile up, which could have disastrous consequences for the US economy, Taleb said this week at an event held by Universa Investments. In fact, rising debt in the US is a "white swan," Taleb said, and is an event that poses an obvious risk to markets versus a "black swan" event, which can occur without much warning. That death spiral would necessitate "something to come in from the outside, or maybe some kind of miracle," Taleb said, when asked how the shock would play out, adding that the situation has made him more pessimistic about the political system in the West. Source: Business Insider

FED: DON'T SEE CUTS UNTIL MORE CONFIDENT INFLATION NEARING 2%

In a nutshell · The FOMC voted unanimously to leave benchmark rate unchanged - as expected - in target range of 5.25%-5.5% for fourth straight meeting while making significant changes to statement · However, the statement was very much more hawkish than expected, as The Fed pushed back aggressively against the dovish market stance. Market reaction: -> The 10-year Treasury yield fell more than 7 basis points to 3.98%. The yield on the 2-year Treasury was last down about 8 basis points at 4.27% -> US equity indices are retreating. Gold is paring gains, dollar is recovering. -> Odds of a March Fed rate cut plummet from 47% to 31% after the Fed interest rate decision. Our take: The U.S. economy enters 2024 from a position of strength. For instance, the S&P PMI came in higher than expected last week. Q4 GDP growth in the U.S. came in at 3.3% annualized, well above expectations of 2.0% growth. And while disinflation is firmly in place, the inflation rate remains above the central bank target. There is thus no reason for the Fed to rush. Nevertheless, we still believe they will have to cut rates at some point for the following reasons: 1/ Keeping rates too high for too long can have long-lasting effects on US economic growth 2/ Keeping rates steady while inflation is coming down imply rising real rates. Keeping positive real rates for too long at a time when Uncle Sam is facing $33T debt and surging interest rates payments is unsustainable

German inflation slows to 2.9% in January from 3.7% in December, lowest level since June 2021

Core CPI slows to 3.4% in January from 3.5% in December, lowest level June 2022. Energy in deflation, hashtag#energy prices dropped -2.8% YoY, while Food CPI slowed to 3.8% from 4.5% in December. Source: HolgerZ, Bloomberg

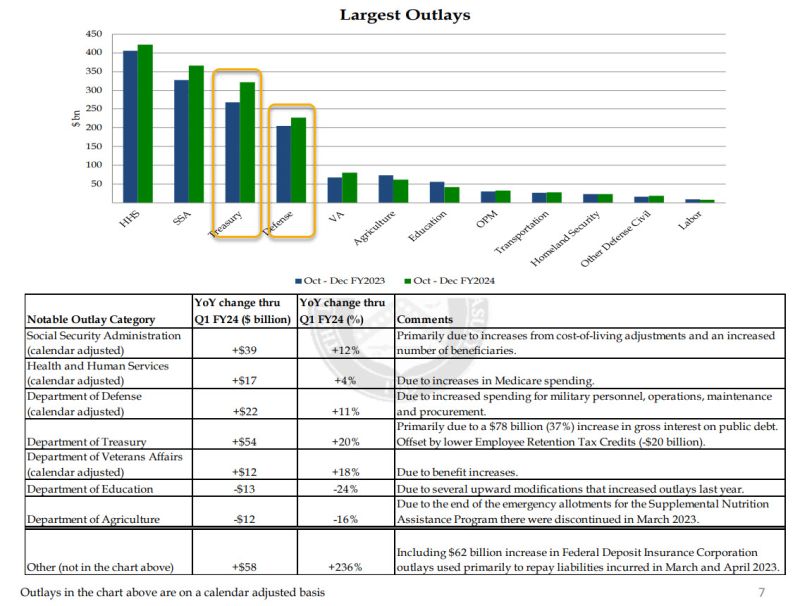

US Treasury confirms spending on debt interest now larger than entire Defense Budget.... and will soon surpass entire Social Security budget.

Source: www.zerohedge.com

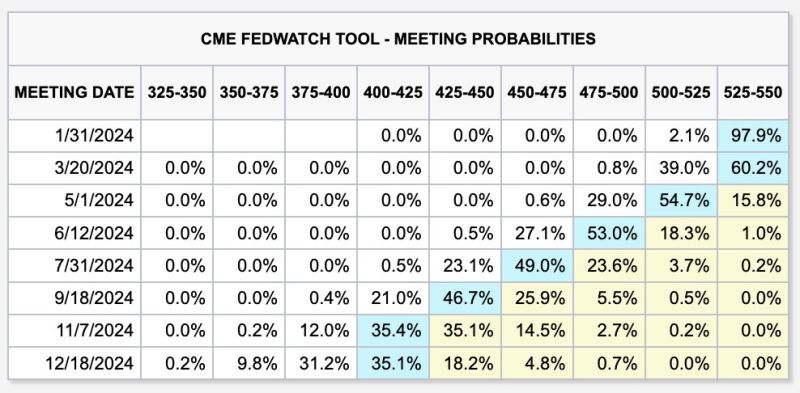

As we are less than 24 hours away from the first Fed meeting of 2024, odds of rate cuts are pulling back

Odds of a rate cut this week are down to 2% and odds of a rate cut in March are down to ~40%. This is the lowest probability of a March rate cut since November 2023. Still, futures are pricing-in a base case of 6 rate cuts for a total of 150 bps in 2024. - All eyes will be on Fed guidance on June 30zh Source: The Kobeissi Letter

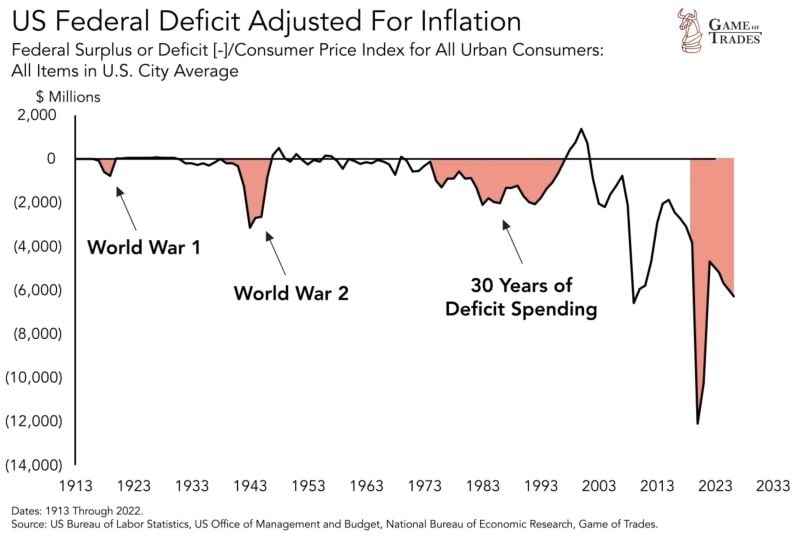

US government spending (inflation-adjusted) since 2020 has exceeded the combined spending of:

- World War I - World War II - 1970 to 1990 Is this sustainable?

All the headline numbers have showed that the labor market is incredibly strong

But is it really? Currently, the US has a record ~8.6 MILLION people that are holding 2 or more jobs. Since 2020, nearly 2.6 million people have taken on an additional job. Source: Bloomberg, The Kobeissi Letter

Interesting FT article highlighting the improvement of global liquidity (contributor -> Cross Border Capital as contributor)

Flows of global liquidity accelerated higher into early 2024, expanding by 9 per cent at an annual rate from September, led by strong increases in Japan and China In 2024, we expect greater liquidity support from central banks as more policymakers turn towards monetary policy easing. Aside from the Fed, the People’s Bank of China is the obvious central bank to watch as it already contributed almost one-fifth of the total increase in global liquidity last year.