15 Jan 2024

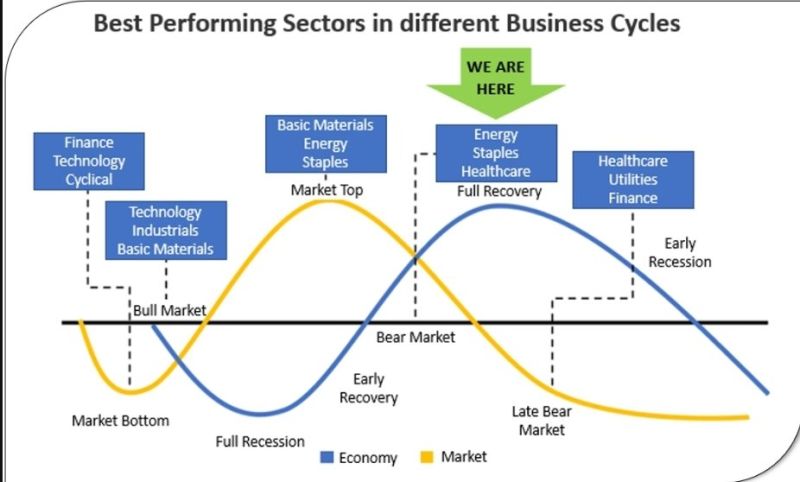

The Economy is not The Market

Source: Win Smart

15 Jan 2024

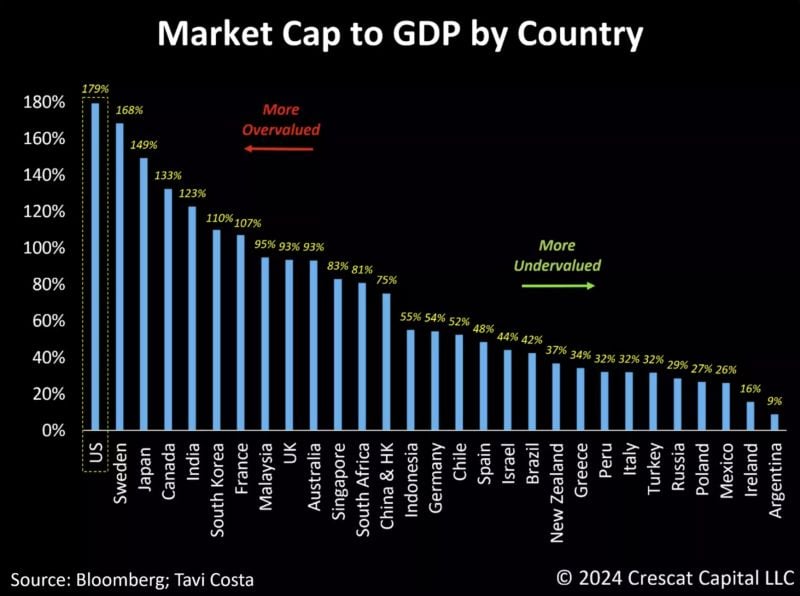

The current macro environment across global equity markets presents a sharply divided investment setup for 2024 and the remainder of the decade.

Source: Tavi Costa

15 Jan 2024

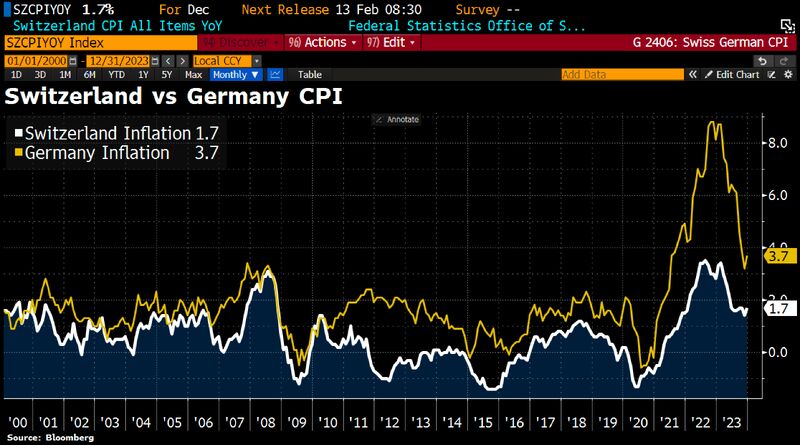

Swiss inflation vs. German inflation.

The inflation rate in Switzerland is already well below the target of 2%. At 1.7%, it is a full 2ppts lower than the German rate. Source: Bloomberg, HolgerZ

15 Jan 2024

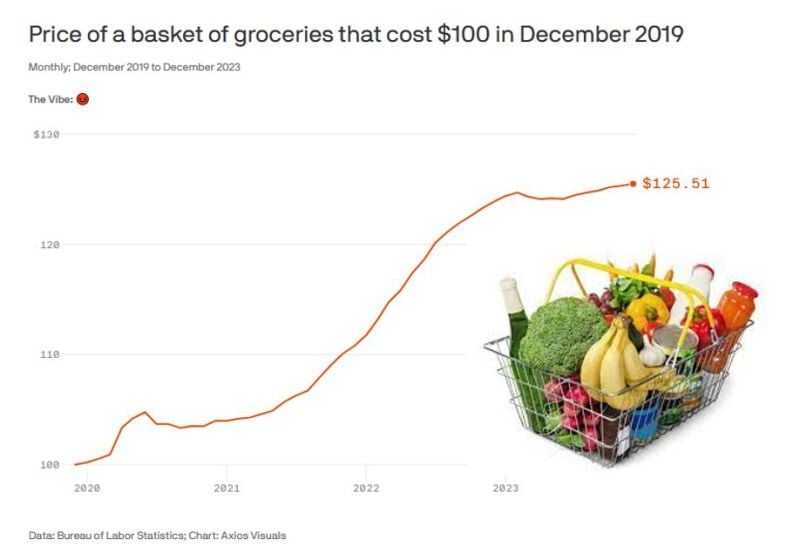

Your grocery bill has increased more than 25% over the last 4 years!

Source: barchart

15 Jan 2024

The Red Sea's inflation threat:

The disruptions in the Red Sea have roiled global supply chains and pushed up freight costs. The Houthis have pledged a “big” response to airstrikes. Iran wins either way w/US airstrikes on Houthis in Yemen. Source: HolgerZ, Bloomberg

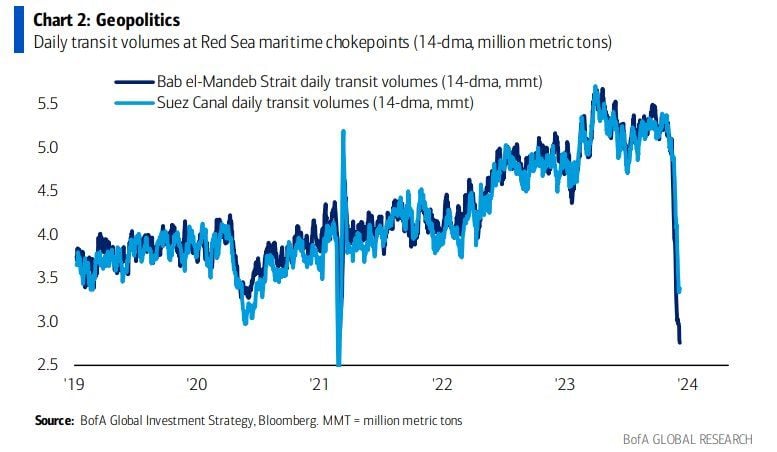

15 Jan 2024

Red Sea Transit Volume

Source: BofA, Win Smart

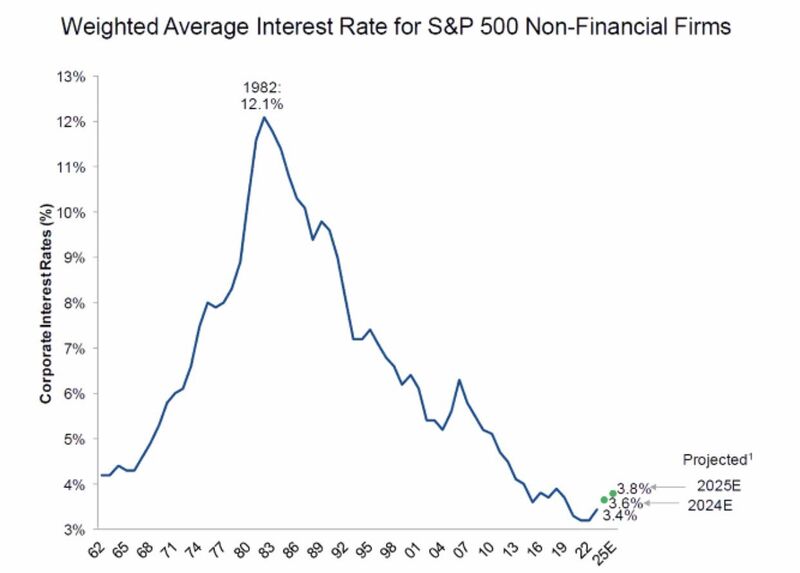

15 Jan 2024

Weighted Average interestrate for sp500 non-financial firms is expected to pick-up in 2024e and 2025e but remains quite low by historical standard.

Source: Michel A.Arouet

15 Jan 2024

Is this the reason why the Fed might be forced to cut rates in March?

We could have: 1. Reverse repo ends (see chart below) 2. BTFP expires 3. Fed cuts (allegedly) 4. QT ends (allegedly) I.e 3 and 4 could counter-balance 1 and 2