15 Jan 2024

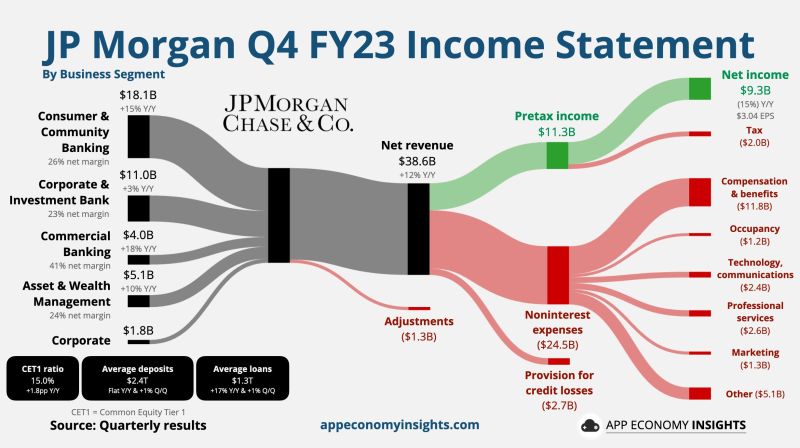

$JPM JP Morgan Chase Q4 FY23.

CEO Jamie Dimon: Deficit spending and supply chain adjustments “may lead inflation to be stickier and rates to be higher than markets expect." • Net revenue +12% Y/Y to $38.6B ($1.2B miss). • Net Income $9.3B. • Non-GAAP EPS: $3.97 ($0.37 beat). • CET1 ratio of 15.0%. • Expect FY24 NII of $90B (+1% Y/Y).

12 Jan 2024

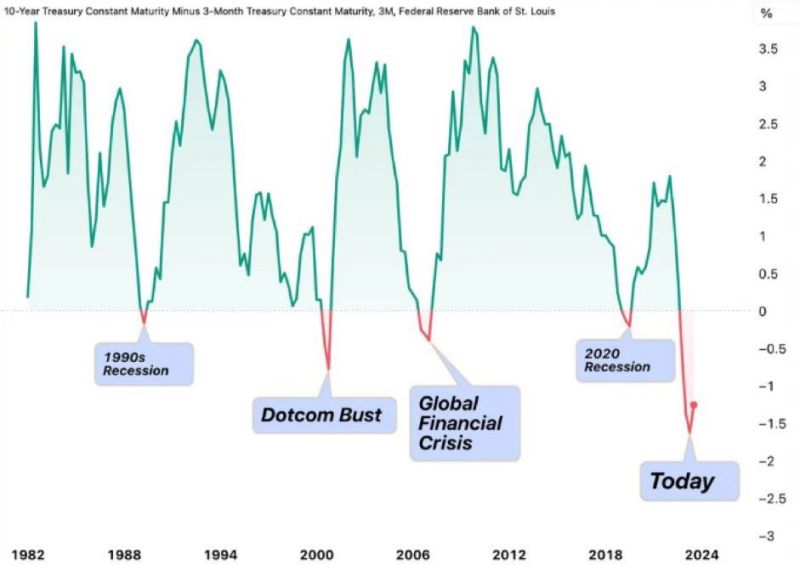

The last 4 times the 10Y Minus 3M Treasury Yield Curve inverted, it led to the 1990s recession, the Dotcom Bust, the Global Financial Crisis, and the 2020 Recession.

Will this time be different? 🤔 Source: Barchart

12 Jan 2024

Uranium 16-Year High: Uranium going parabolic as it hits its highest price since November 2007

Source: barchart

12 Jan 2024

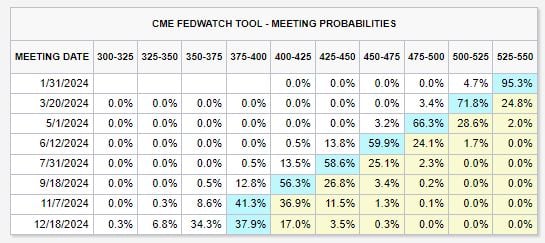

Surprise, surprise... Even with a hot jobs report and inflation rising to 3.4%, market expectations regarding timing and number of rate cuts have shifted more dovish.

Markets are now pricing-in a rate cut at EVERY Fed meeting this year beginning in March 2024 until December 2024. Effectively, markets are saying that us interestrates will move in a straight-line lower. Source: The Kobeissi Letter

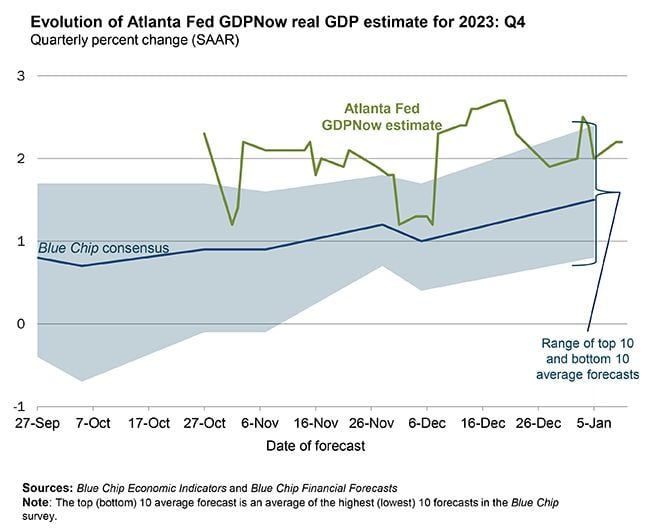

11 Jan 2024

On January 10, the GDPNow model nowcast of us real GDP growth in Q4 2023 is 2.2%

Source: Atlanta Fed

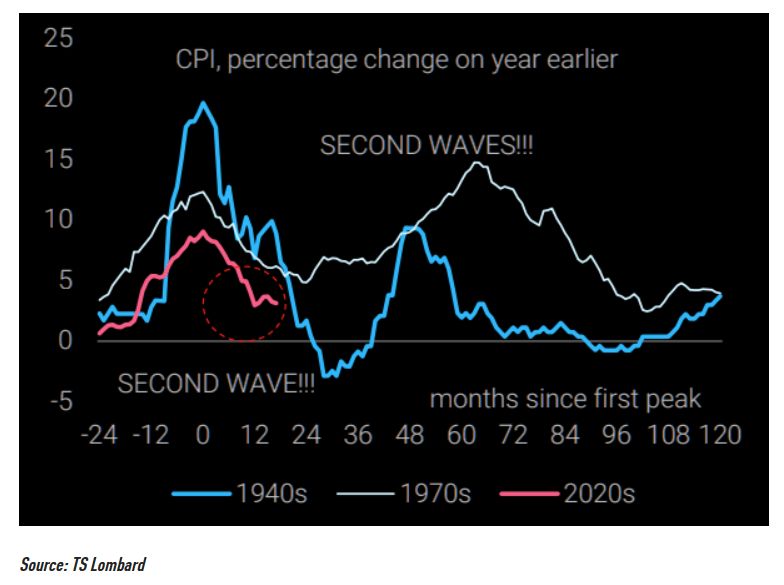

11 Jan 2024

Beware the second wave...inflation moves in mysterious ways and sometimes you get that "unplanned" second wave.

Source: TS Lombard, TME

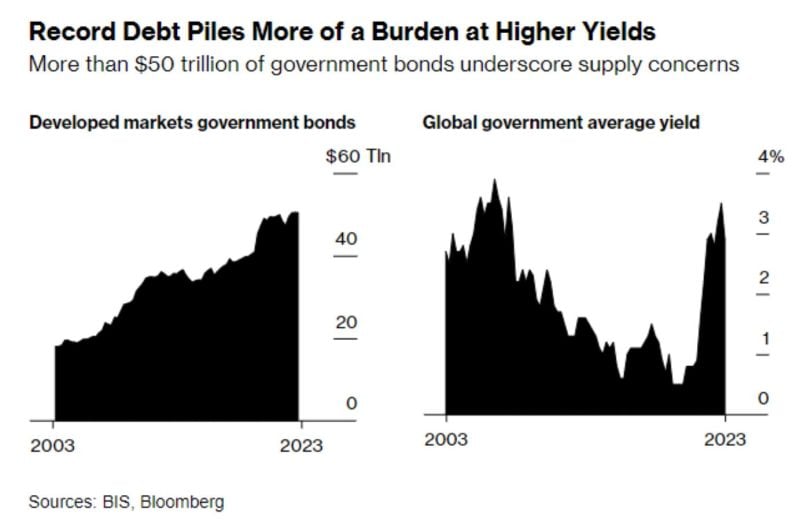

11 Jan 2024

While G7 claims can offer short-term tactical opportunities, soaring G7 debt levels at the the of high yields mean that the long-term risk-reward remains unattractive.

Source chart: Bloomberg

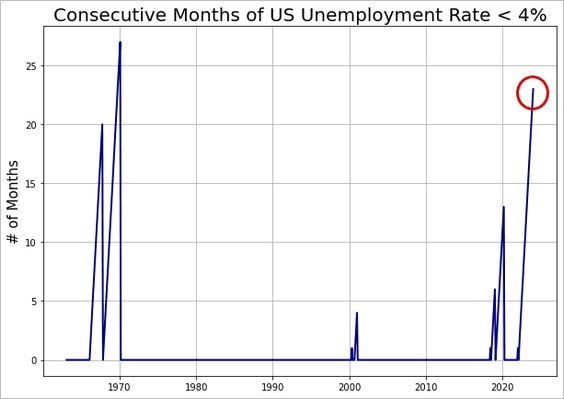

10 Jan 2024

Remember the 70s?

Source: Win Smart