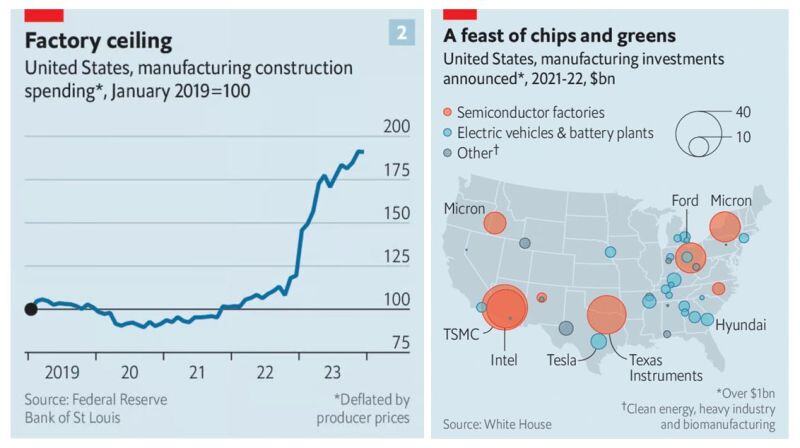

US manufacturing mega-boom in 2 images

Source: Science is Strategic, The Economist

🚨 🚨 🚨 HUGE SECTOR ROTATION OUT OF TECH AND INTO SMALL CAPS HAPPENING NOW 🚨 🚨 🚨

⬇ Nasdaq 100 $QQQ -1.0% ⬆ Russell 2000 $IWM +3.3% Source: Stocktwits

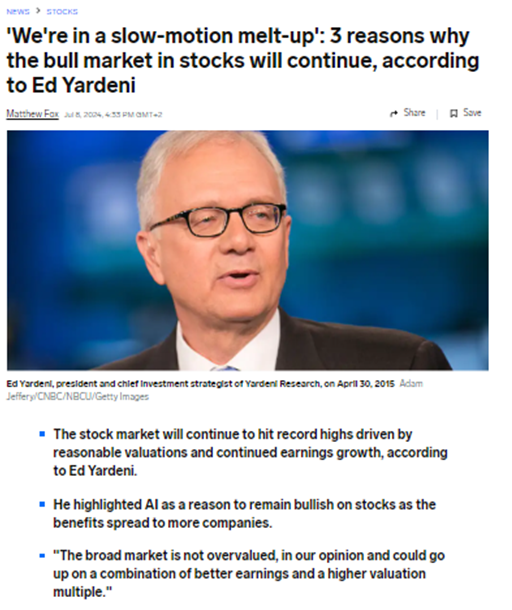

We're in a slow-motion melt-up according to Ed Yardeni

Source: Business Insider

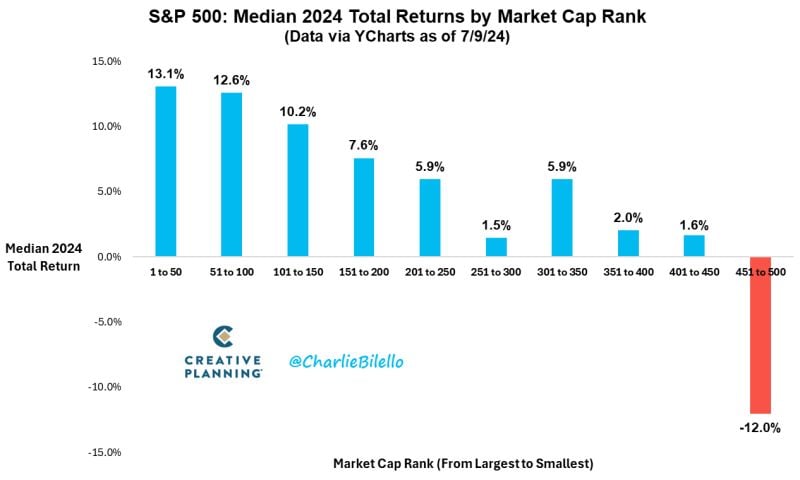

The 50 largest stocks in the S&P500 have a median return of +13% this year while the 50 smallest stocks in the index are down 12%.

$SPX Source: Charlie Bilello

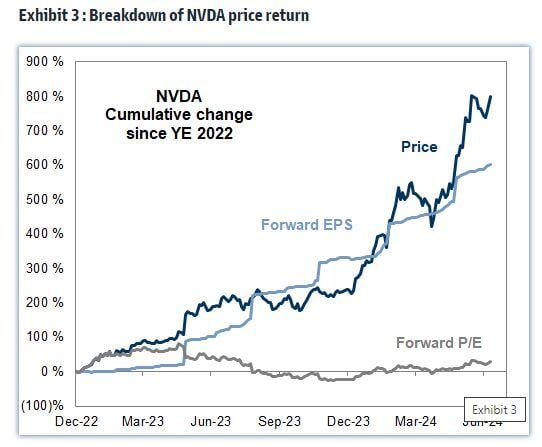

Nvidia $NVDA P/E hardly changed last 18 months

Source: Mike Zaccardi, Goldman Sachs

The S&P 500 climbed Wednesday to a fresh record, breaking above 5,600 for the first time, as a sharp rise in semiconductor stocks led the market higher.

The broad market index jumped 1.02%, closing at 5,633.91, and notching a seventh straight day of gains.

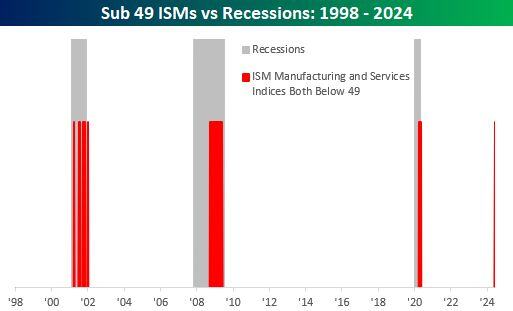

In June, both ISM Manufacturing and ISM Services fell below 49.

Here are all months where both PMI readings were below 49 Source: Bespoke

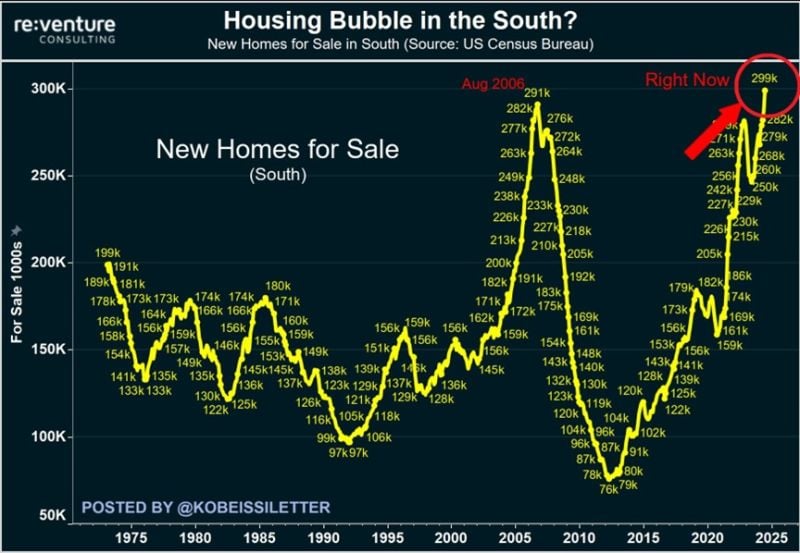

BREAKING: There are now a record 299,000 new homes for sale in the Southern US states, according to Reventure.

This is even higher than in 2006, a year before the housing market crash began. The number of new houses for sale in the South has nearly DOUBLED in just 4 years. Meanwhile, new home sales have officially dropped below pre-pandemic levels for the first time. It would take ~9 months current new inventory to sell if it sold at the current pace without new inventory coming to the market, 2nd longest duration since 2009. Source: The Kobeissi Letter, Reventure