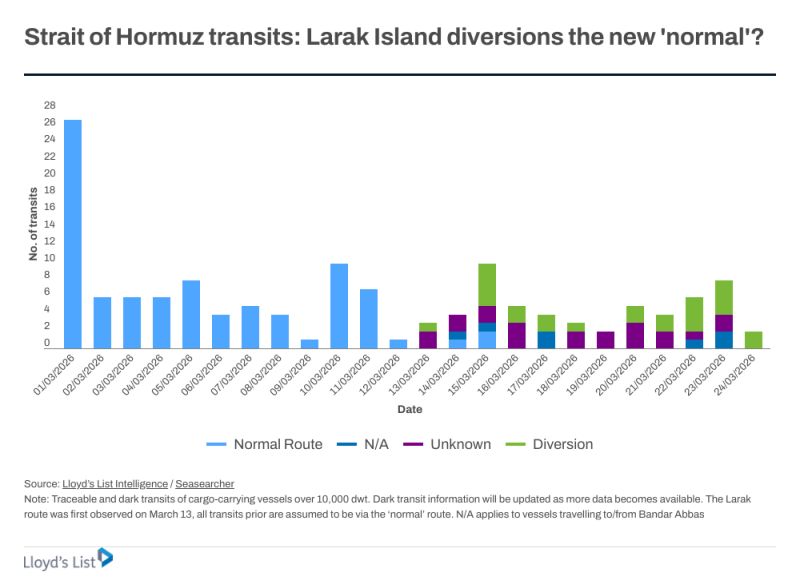

The limited flow of traffic moving through the Strait of Hormuz is now sailing exclusively through an IRGC-controlled corridor requiring specific clearance codes and an Iranian escort service.

Source: LLoyd's List

Iran Controls Passage Through the Strait of Hormuz

Iran has announced it will allow “non-hostile vessels” to transit the Strait of Hormuz, but only under Iranian control and coordination. This strait normally carries ~20% of global oil, yet thousands of ships are delayed, attacked, or paying high fees. Iran may block vessels linked to the US or Israel and is drafting laws to formalize control. Beyond shipping, this move signals a financial shift, including potential moves away from the US dollar, turning the Strait into a strategic leverage point in global energy and trade. Source: Financial Times

SHIPS PASSING THROUGH THE STRAIT OF HORMUZ

🟢 Feb 26 → 🚢 132 🟢 Feb 27 → 🚢 128 🟠 Feb 28 → 🚢 98 🟠 Mar 01 → 🚢 18 🟠 Mar 02 → 🚢 7 🔴 Mar 03 → 🚢 2 🔴 Mar 04 → 🚢 2 🔴 Mar 05 → 🚢 1 🔴 Mar 06 → 🚢 0 🔴 Mar 07 → 🚢 1 🔴 Mar 08 → 🚢 2 🔴 Mar 09 → 🚢 1 🔴 Mar 10 → 🚢 2 🔴 Mar 11 → 🚢 1 🔴 Mar 12 → 🚢 0 🔴 Mar 13 → 🚢 3 🔴 Mar 14 → 🚢 1 🔴 Mar 15 → 🚢 0 🔴 Mar 16 → 🚢 1 🔴 Mar 17 → 🚢 2 🔴 Mar 18 → 🚢 1 🔴 Mar 19 → 🚢 0 🔴 Mar 20 → 🚢 1 🔴 Mar 21 → 🚢 2 🔴 Mar 22 → 🚢 3 🔴 Mar 23 → 🚢 5 🔴 Mar 24 → 🚢 6 Source: Windward Maritime Intelligence, Lloyds List, PIB India, and regional briefings.

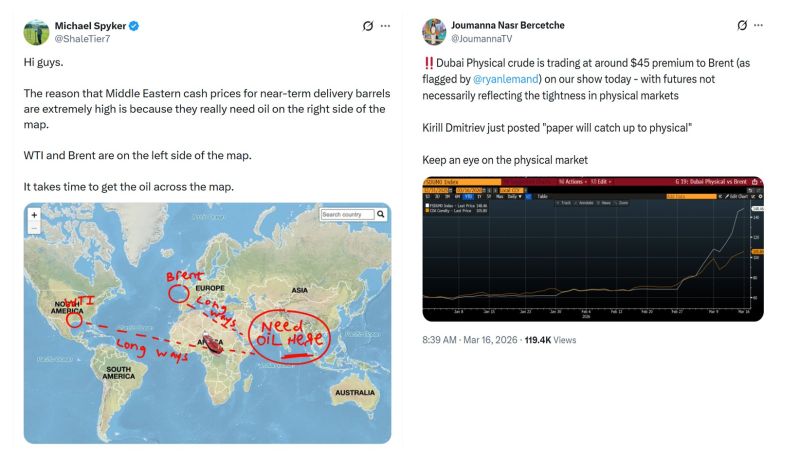

Dubai Physical Prices vs. Brent Futures

As highlighted by Anton Likhodedov @ALikhodedov on X: Many people are questioning why Brent futures aren’t higher and pointing out the massive premium of Dubai oil physical versus Brent futures (see post by Joumanna Bercetche on X his morning following her interview with Brent futures probably don’t fully reflect the severity of the current situation, but a few additional points—building on Michael’s chart on the right —are worth considering: 1) Brent reflects forward delivery and location differences. Brent is currently trading the May contract, and in about two weeks the market will roll to June. These contracts represent crude loading in the North Sea, while much of the incremental demand is in Asia. 2) Shipping times significantly affect the landed price. Looking at the Sparta dashboard, voyage times from the North Sea (for example Hound Point for Forties) to key Asian destinations are roughly: India / Singapore / South Korea: ~37–48 days By comparison: Fujairah → India (Sikka): under 3 days Fujairah → Singapore: about 11 days When you factor in these logistics, the difference in arrival times is substantial, which explains a large portion of the price discrepancy. 3) Crude quality also matters. As June Goh from Sparta explains in the article below, Asian refiners are also dealing with crude slate optimization and diversification, which affects pricing dynamics. That said, the gap between landed prices of Atlantic Basin cargoes and Fujairah cargoes has widened significantly. As a result, some Asian refiners are beginning to consider Brent despite the longer shipping time. A notable example: Trafigura sold a cargo of about 700,000 barrels for late-March loading to a Thai refiner. It’s reportedly the first time a Thai company has bought North Sea crude since at least 2019, when Bloomberg began tracking the data.

Reports are circulating that Saudi Arabia, the UAE, Kuwait, and Qatar are discussing withdrawing from US contracts and cancelling future investment commitments

According to the Financial Times, the Gulf states are facing growing budget pressure due to the US-Israeli war with Iran, which is disrupting their economies. The conflict has reduced energy revenues, slowed shipping through the Strait of Hormuz, damaged oil and gas infrastructure, hurt tourism and aviation, and increased defence spending. As a precaution, some Gulf governments are reviewing overseas investments and financial commitments, including investment pledges, business contracts, sports sponsorships, and asset holdings. They may also consider invoking force majeure clauses in contracts. The review could affect major global investments, including hundreds of billions of dollars pledged to the US, attracting attention from the White House. According to the FT, Gulf leaders had urged diplomacy before the war and are now frustrated about being drawn into the conflict, questioning whether their financial support for regional initiatives is being used for peace or war. Saudi Arabia held 254 billion riyals in U.S. equity exposure as of Q4 2025. Across the Gulf Cooperation Council (GCC), total financial commitments linked to the United States are estimated at $3–4 trillion, spanning sovereign wealth fund investments, defense procurement, infrastructure partnerships, and bilateral investment agreements. The United Arab Emirates alone has pledged $1.4 trillion in U.S. investments over the next decade, under an economic framework announced during Donald Trump’s first 100 days in office. These figures are not merely financial statistics—they form the economic backbone of the U.S.–Gulf security partnership. In effect, they underpin the strategic relationship that allows the Pentagon to maintain its military presence in the region, including deploying carrier strike groups in the Arabian Gulf. Bottom line: If the war continues, Gulf states may scale back global investments and financial commitments, which could have significant economic and geopolitical consequences, including pressure on the US to pursue diplomacy.

Dubai and Abu Dhabi: a reminder of property prices (as of the end of January)

Source: Hasnain Malik

Saudi Arabia has removed all restrictions for foreigners to buy local stocks.

The decision allows non-residents to invest directly in the main market effective Feb. 1.

A $100B "Santa Rally" might have arrived via the UAE sovereign wealth funds

Here is the breakdown of what is going on: 1. The $100 Billion Life Raft 💰 OpenAI is reportedly looking to raise a staggering $100B (Source: WSJ). With a target valuation of $830B, this isn't just a fundraising round—it’s a geopolitical event. Sam Altman isn't just looking for "growth capital"; he’s securing a bridge to 2030 profitability. 2. From Debt to Equity 📉 Private credit markets (like Blue Owl) have been tightening the taps on AI infrastructure. OpenAI is pivoting from cheaper debt to massive equity dilution. Why? Because when you’re "incinerating" cash to build the future, you need a sovereign-sized safety net. 3. The Oracle "Survival" Surge 🚀 This isn't just about OpenAI. This cash flows directly into compute. Oracle and CoreWeave are the primary beneficiaries. This funding ensures OpenAI can pay its hyperscaler partners for years to come. The market is breathing a sigh of relief: Bankruptcy risks for AI infrastructure plays are evaporating. 4. The Credit Default Swap (CDS) Collapse 📉 Before tonight, Oracle’s CDS was at a 16-year high (~156bps). Investors were pricing in serious risk. Now? We expect a short-covering frenzy. The "AI winter" just got hit by a heatwave of Emirati capital. The Bottom Line: The world was waiting for the US to backstop the AI revolution. Instead, Abu Dhabi stepped up. This $100B injection doesn't just fund a chatbot; it stabilizes the entire AI ecosystem for the next 24 months. Is this the start of the 2025 bull run, or just a very expensive bridge to the unknown?