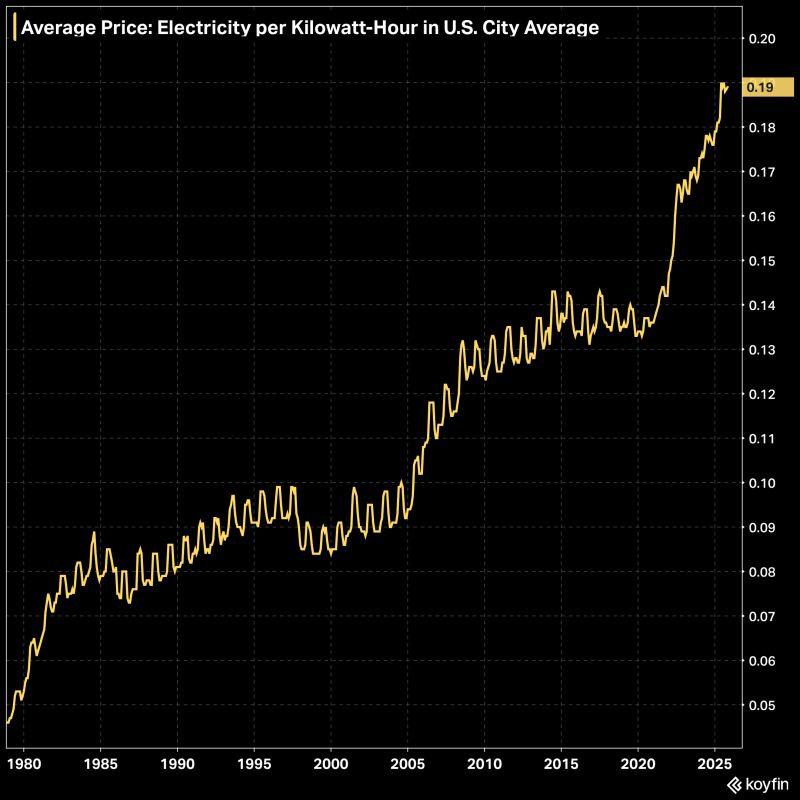

The average price of electricity per Kilowatt-hour in the United States.

Source: Koyfin @KoyfinCharts

The Federal Reserve's 420 Billion Dollars Wall Street Bailout

The Fed has quietly delivered nearly HALF A TRILLION DOLLARS of no-strings-attached bank bailouts in the last few months, according to documents & data reviewed by @LeverNews . In all, the new bailouts are already 60% of the amount of the financial crisis TARP bailout. Source: David Sirota @davidsirota

BREAKING: U.S. stock market has wiped out $650 billion in market value this week.

Nasdaq -1.40% Dow -1.21% S&P 500 -1% While Bitcoin is up 7%. BTC has added $130 billion, and the total crypto market has added $190 billion this week. Remember the stocks are at all time high, while Bitcoin is still down -23% from its ATH of $126k. Source: Bull Theory

According to technical models, hashtag#silver $SLV should’ve stopped about 47 trendlines ago...

Source: Trend Spider

Hear that sound? Over $20 trillion in market cap quietly breaking down to new 4-month lows relative to the S&P500.

Source: J-C Parets

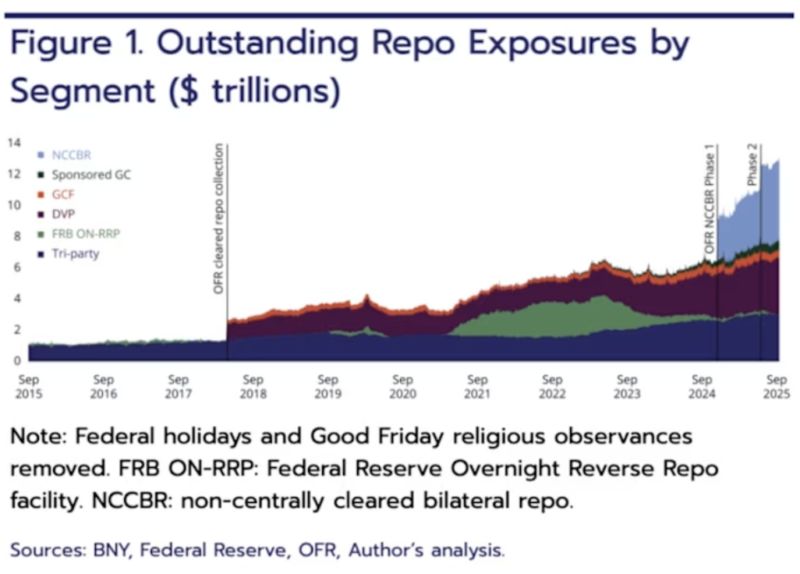

Total Repo Exposure has reached an all-time high of $12.6 Trillion

Source: barchart

Treasury Secretary Scott Bessent goes full fire on Powell

Sec. Bessent says the probe into Fed Chair Jerome Powell is 100% justified, “NOBODY is above the law!” “There NEEDS to be some accountability!” “The Fed is now LOSING $100B a year! $100B! With NO accountability!” Jerome should RESIGN, NOW. The Fed’s bleeding billions under Powell’s watch, time for real oversight and America First monetary sanity. No more excuses! Source: @GuntherEagleman

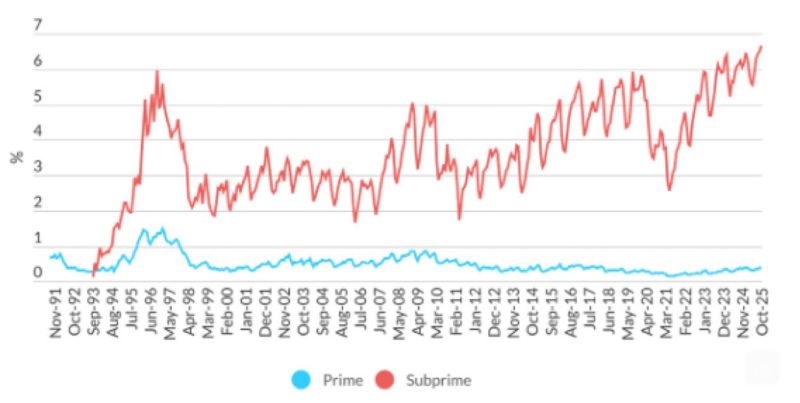

% of subprime auto loans that are 60 days or more overdue on their payments hit an all-time high of 6.65%

Source: Barchart