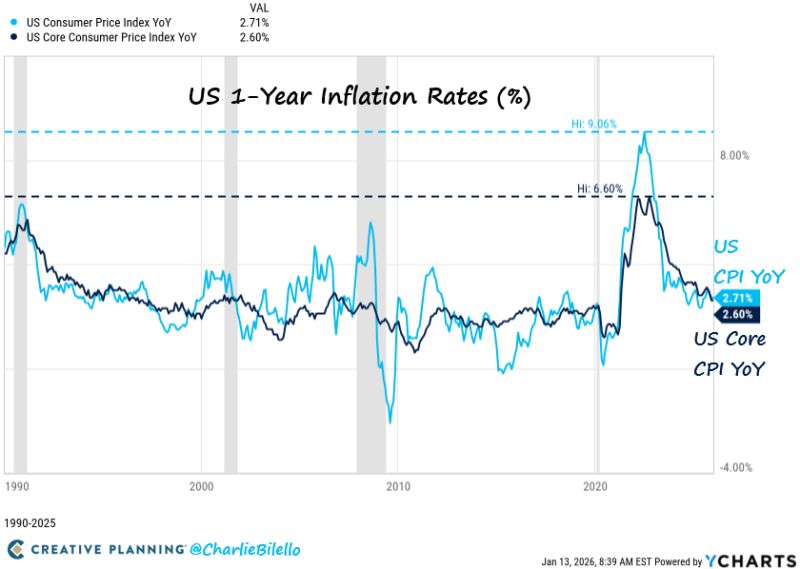

CPI Holds at 2.7% YoY as December Rebound Falls Short of Fears

The headline CPI print rose 0.3% MoM (vs +0.3% MoM exp) driving prices up 2.7% on a YoY basis (vs +2.7% YoY exp). Many expected a December pickup due to the unwinding of distortions from data-collection disruptions during the government shutdown, which amplified seasonal discounting in November. So the headline number is basically below most of “Whisper” numbers. Source: Charlie Bilello

U.S. Companies issued $95 Billion worth of bonds during the first week of the year, the highest weekly volume since Covid

Source: Barchart

Global Central Bankers in "Full solidarity" with Fed's Powell

Claims that the Fed is “losing independence” are being reframed by James E. Thorne as misleading. According to this view, Chair Powell publicly suggested the DOJ was threatening a criminal indictment over his testimony on costly Fed building renovations—despite the DOJ never using that term. The U.S. Attorney’s Office had repeatedly sought clarification on cost overruns and testimony accuracy, but those requests were ignored until grand jury subpoenas were issued, after which Powell framed the situation as retaliation. Monetary policy independence remains intact, but it does not imply immunity from fiscal or legal oversight. Invoking “central bank independence” in this context is seen as an attempt to shield the Fed from accountability rather than a genuine threat to rate-setting autonomy. Source: Bloomberg, James E. Thorne @DrJStrategy

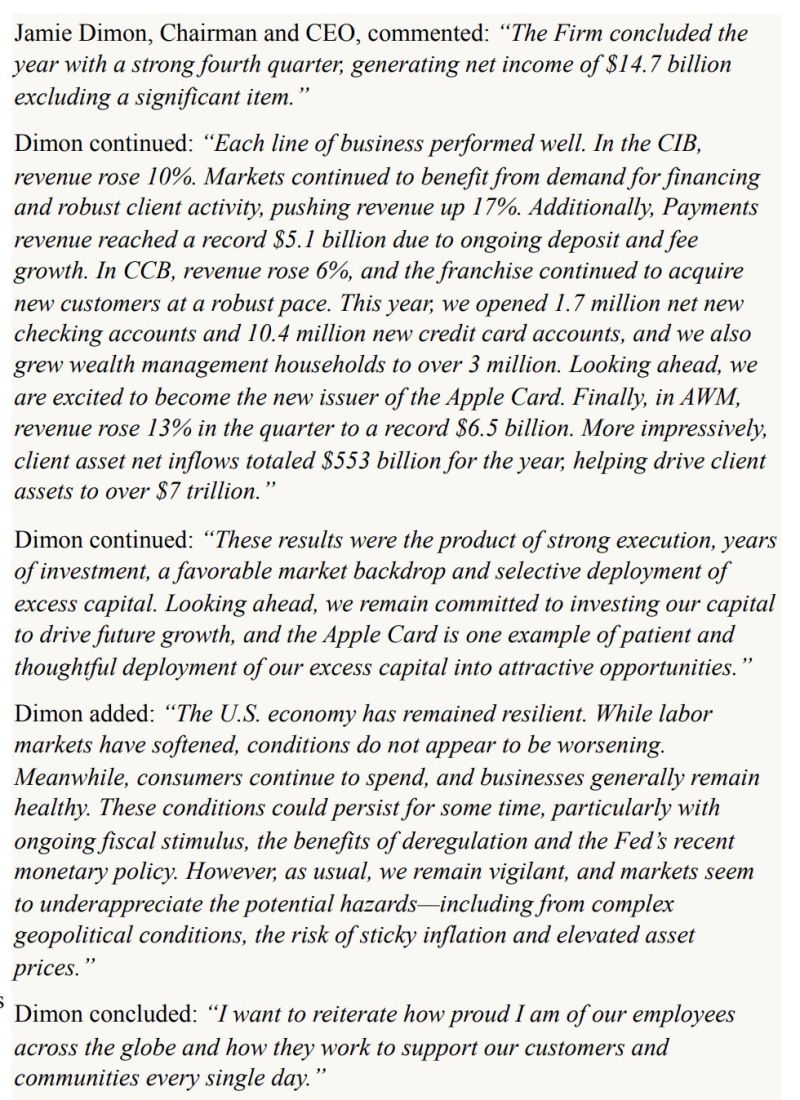

Jamie Dimon: U.S. Economy Remains Resilient Despite Softer Labor Markets

$JPM JP Morgan CEO Jamie Dimon: "The U.S. economy has remained resilient. While labor markets have softened, conditions do not appear to be worsening. Meanwhile, consumers continue to spend, and businesses generally remain healthy. These conditions could persist for some time..." Source: The Transcript

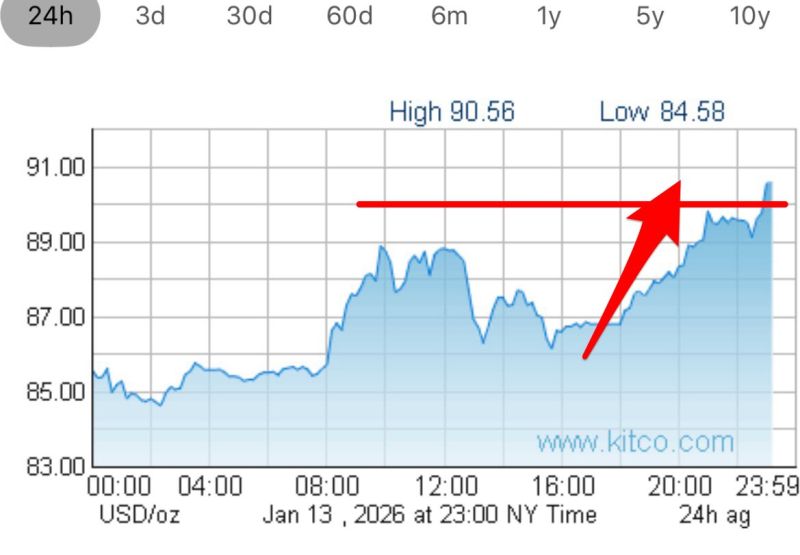

Silver storms through the $90 level. This is unprecedented! Both exciting & concerning at the same time.

Source: Silver Gold News

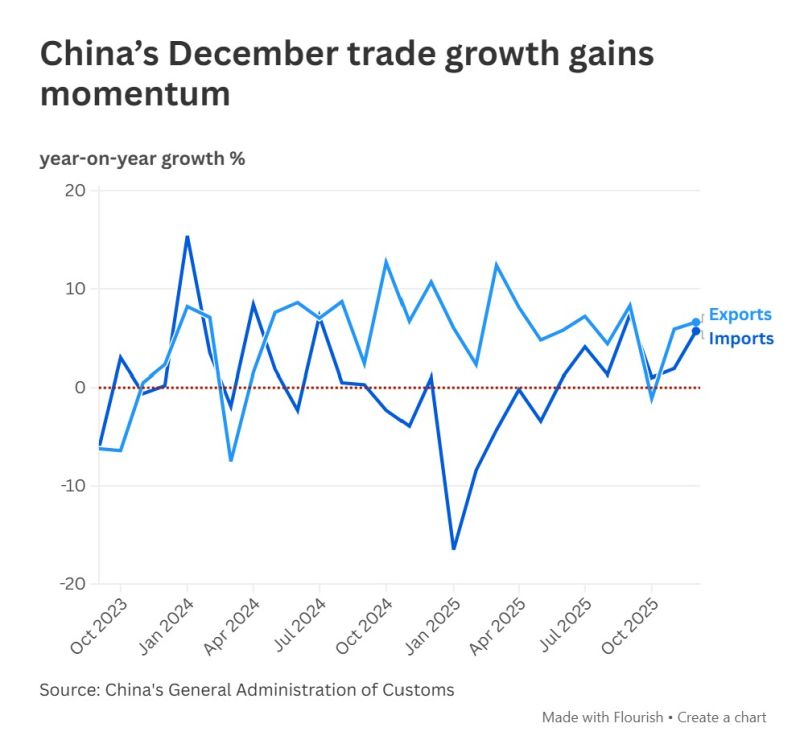

The $1.19 Trillion Elephant in the Room

China’s December trade data just leaked, and it’s a masterclass in contradiction: ✅ The Good News: Exports beat expectations by 2x. Imports are at a 3-month high. The annual trade surplus hit a record high (up 20%). ❌ The Bad News: Trade with the U.S. is in freefall. Exports to the U.S. are down 30%. Imports from the U.S. are down 29%. What does this mean for 2026? - Diversification is king. China is filling the "U.S. gap" elsewhere. - Tariffs are working (but maybe not as intended). They are reducing bilateral trade, but China’s total global footprint is still growing. - Supply chains are shifting. Expect "China + 1" to move from a buzzword to a survival requirement. Source: CNBC

The Gold/Silver pair down to 52x - the lowest since Dec 2012

Since: zerohedge

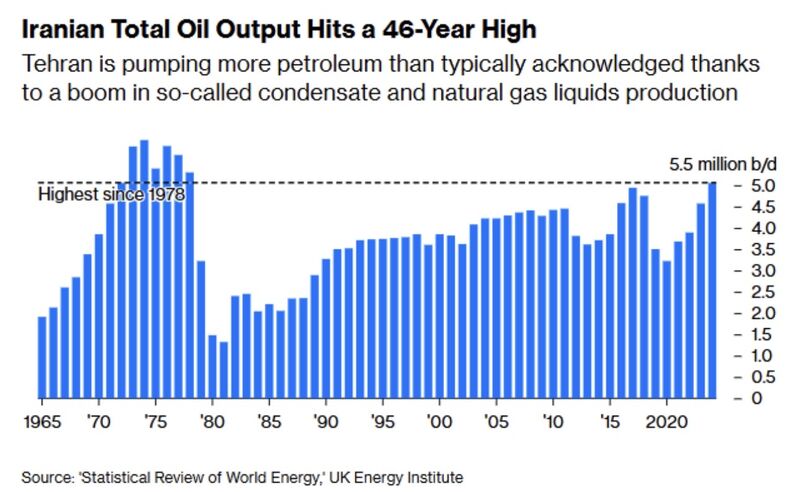

Iran’s Oil Output: A 46-Year Milestone You Might Have Missed

For the first time since 1978, Iran’s oil output has reached about 5.5 million barrels per day, marking a structural shift rather than a simple recovery. After years of volatility, production has surged since 2020, driven largely by growth in condensates and natural gas liquids (NGLs), which are less constrained by sanctions than conventional crude. Much of this supply is moving discreetly to China via shadow fleets, adding hidden liquidity to global markets and helping restrain oil prices despite geopolitical risks. Bottom line: Iran is re-emerging as a major energy player in a form that is harder to sanction, raising questions about how effective traditional oil sanctions remain in today’s market. Source: Jack Prandelli on X